ansonsaw

Nobody said investing was easy, and it’s simply hard to find a high-growth stock that yields 5%. Yet, it’s possible to find such a deal with an eye on the market, especially in light of no Santa Claus rally and amidst year-end tax loss harvesting.

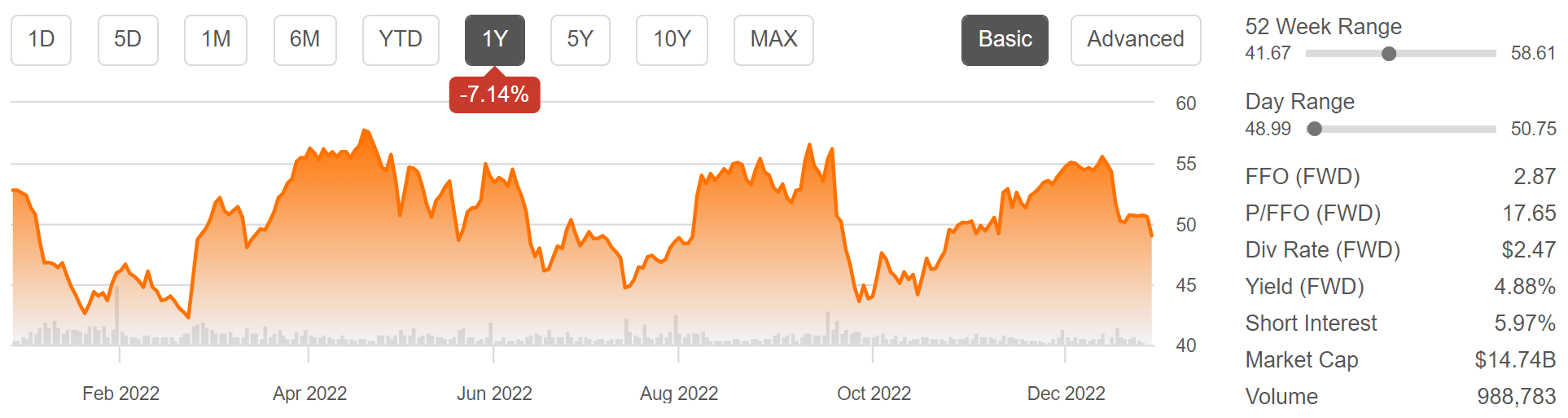

Such I find the case to be with Iron Mountain (NYSE:IRM), which, as seen below, is now again back below $50 after the sell-off this month. At the current price of $49, IRM now yields 5.0%. This article highlights why now marks an opportune time to pick up this growth while it’s down.

(Note: Dividend yield below is as of 12/27 close)

IRM Stock (Seeking Alpha)

Why IRM?

Iron Mountain Inc. is a global leader in storage and information management services, helping organizations to store, protect, and manage their physical and digital data. The company was founded in 1951 and has since grown to become a Fortune 1000 company with a market capitalization of $15 billion.

At present, it operates a network of over 2,000 storage facilities in 58 countries and serves 225K customers including 95% of the Fortune 1000 companies. The company also has a strong presence in the digital segment, offering cloud-based data storage and protection services.

One of the key drivers of Iron Mountain’s growth in recent years has been its focus on innovation and the development of new services. In recent years, the company has invested heavily in the development of its digital offerings, including the acquisition of several technology companies to enhance its capabilities.

IRM’s core business and transformation appear to be going rather well. This is reflected by 18% YoY revenue growth on a constant currency basis (14% growth including FX headwinds) to $1.3 billion in the third quarter. This was driven by pricing benefits, positive volume trends, and data center growth. Notably, IRM leased seven MW of data center capacity last quarter, and management expects to exceed its 130 MW projection this year.

Speaking of pricing benefits, I view IRM as being a net beneficiary of inflation, especially on the records storage side, which comes with low labor costs. In fact, IRM’s CEO said years ago, when inflation was low, that he prayed for inflation. As such, it appears that he has gotten his wish, with inflation running hot for much of this year.

Dividend growth investors also have good reasons to be optimistic, as IRM’s dividend to AFFO payout ratio is now 63% (based on Q3 AFFO per share of $0.98). This is now within IRM’s long-term target AFFO payout ratio range in the low to mid-60s. Management has stated that they expect to grow the dividend in line with AFFO growth should this level be sustained.

Looking forward, IRM targets 5-year AFFO per share CAGR of 7%, which translates to potential 12% total returns, when including the 5% dividend yield. In addition to IRM’s core RIM business, it’s also finding good traction in the adjacent fine arts storage business. These trends along with the capital-light nature of the business were highlighted by management during a recent Wells Fargo (WFC) industry conference:

So things such as our fine arts business has been growing quite quickly, albeit one of our smaller lines of business. Our consumer business has been growing quite quickly as well as our other business services storage that both of which the consumer and the other lines of business storage is all in our global RIM business.

And we see a significant amount of incremental runway there. Importantly, with the exception of fine arts, everything else we’re storing is generally going into the same record centers that we already have. So the team is doing a great job utilizing our existing physical space. And that’s one of the reasons why we say that our core business is quite capital light. We can continue to grow nicely with relatively little incremental investment.

Meanwhile, IRM carries a solid balance sheet with a net lease adjusted leverage of 5.2x, sitting below the 5.8x average among REITs. It also maintains $1.5 billion in liquidity and 79% of the balance sheet debt is carried at fixed rate. The weighted average interest rate is also at a modest and manageable 5.0%.

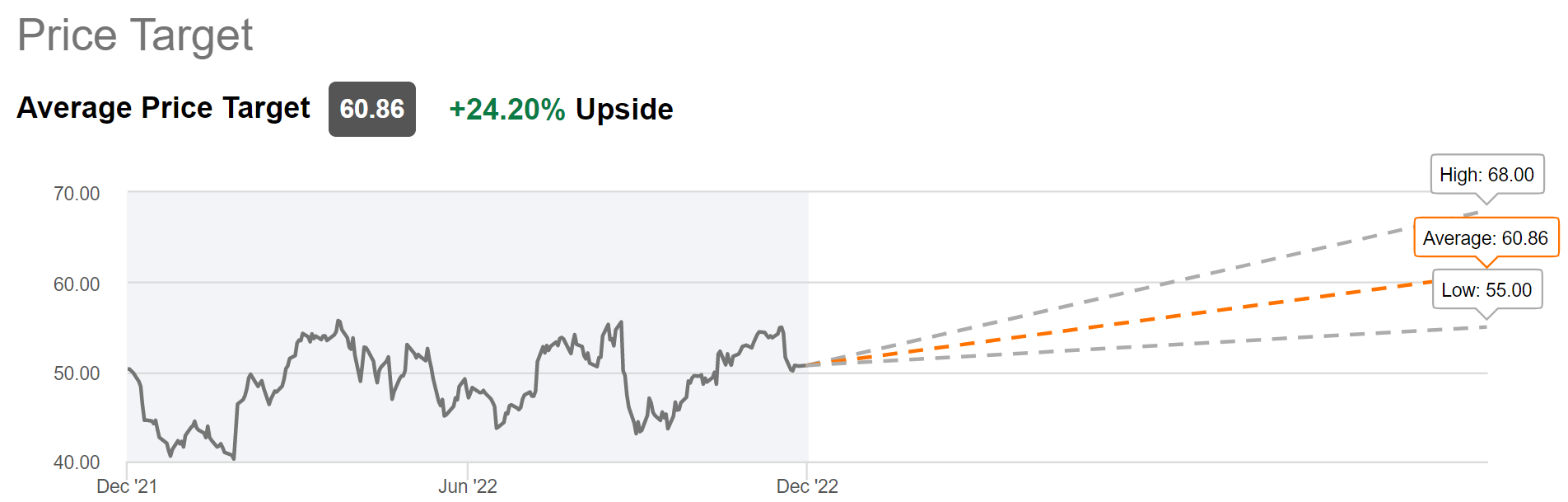

Turning to valuation, IRM isn’t necessarily cheap at $49 with a forward P/FFO of 17.1, but I believe it’s attractively priced considering the stability and growth of its business model. Plus, analysts project a 6.4% FFO per share growth rate next year before ramping up to the low teens thereafter. Analysts have a consensus Buy rating on the stock with an average price target of $61, translating to potentially very strong total returns in the near term.

IRM Price Target (Seeking Alpha)

Investor Takeaway

IRM’s transformation appears to be going well, and its core RIM business is seeing positive volume trends. The core capital-light model, in combination with growth in the company’s adjacent fine arts business and digital expansion strategy, bodes well for future growth.

Investors could see meaningful capital appreciation in the near term, and a potential 12% long-term annual returns. As such, I find IRM to be a solid buy at these levels for dividend growth investors.

Be the first to comment