SimonSkafar

A Quick Take On SONDORS

SONDORS Inc. (SODR) has filed to raise $22.5 million in gross proceeds from the sale of its common stock in an IPO, according to an amended registration statement.

The company manufactures premium electric bicycles and motorcycles for sale to consumers.

While Sondors Inc. has grown revenue, I’m cautious about its profit outlook in the near term as it faces a macroeconomic slowdown with high inventory in a competitive industry.

I’m on Hold for the SODR IPO.

SONDORS Overview

Malibu, California-based Sondors was founded to develop and sell high quality electric bikes and motorcycles for sale worldwide.

Management is headed by founder and CEO Storm Sonders, who has been with the firm since inception since 2015 and was previously an entrepreneur in the toy business, designing models for Mattel, McDonald’s and Fisher-Price.

The company’s primary offerings include:

-

Electric bicycles

-

Electric motorcycle

-

SONDORS mobile app

-

Community

As of September 30, 2022, Sondors has booked fair market value investment of $5.2 million from investors.

SONDORS – Customer Acquisition

The firm sells its products through retail outlets such as Costco Wholesale and direct-to-consumer [DTC] via the company’s website.

To-date, the company has delivered more than 51,000 e-cycles to 72 countries.

Selling and Marketing expenses as a percentage of total revenue have dropped to 9.9% as revenues have increased, as the figures below indicate:

|

Selling and Marketing |

Expenses vs. Revenue |

|

Period |

Percentage |

|

Nine Mos. Ended September 30, 2022 |

9.9% |

|

2021 |

19.2% |

|

2020 |

17.8% |

(Source – SEC)

The Selling and Marketing efficiency multiple, defined as how many dollars of additional new revenue are generated by each dollar of Selling and Marketing spend, rose to 3.3x in the most recent reporting period, as shown in the table below:

|

Selling and Marketing |

Efficiency Rate |

|

Period |

Multiple |

|

Nine Mos. Ended September 30, 2022 |

3.3 |

|

2021 |

1.4 |

(Source – SEC)

SONDORS’ Market & Competition

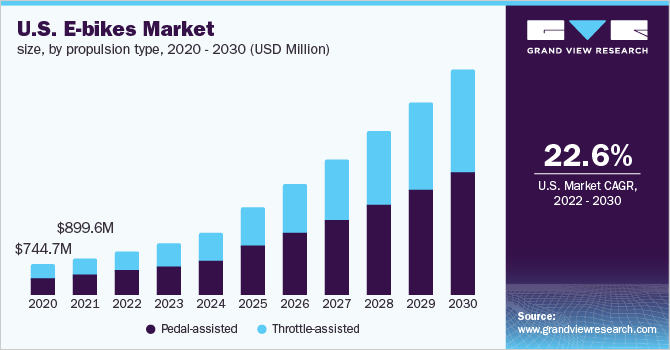

According to a 2022 market research report by Grand View Research, the global e-bicycle market was an estimated $17.8 billion in 2021 and is forecast to reach $55.7 billion by 2030.

This represents a forecast CAGR of 13.5% from 2022 to 2030.

The main drivers for this expected growth are an increasing awareness by consumers about cleaner alternatives to existing modes of transportation and a growing number of regions that are installing or modifying streets that are bicycle friendly.

The rise in the number of cyclists commuting due to the pandemic has also been a major driver of growth.

Furthermore, technological advancements in the e-bicycle market, increasing development of innovative e-bicycles, and growing demand for electric mountain bikes are expected to generate more opportunities in the e-bicycle market.

In addition, the growth of the e-bicycle market is driven by rising concerns about air pollution and climate change and government initiatives and subsidies.

Also, the chart below shows the historical and projected future growth trajectory of the U.S. e-bicycle market:

U.S. E-Bicycle Market (Grand View Research)

Major competitive or other industry participants include:

-

Specialized Bicycle Components

-

Trek Bicycle

-

Canyon Bicycles GmbH

-

Rad Power Bikes

-

Zero Motorcycles

-

Energica

-

LiveWire

-

Super 73

-

Pedego Electric Bikes

-

Yamaha Motor Company

-

Aima Technology Group Co. Ltd.

-

Merida Industry Co. Ltd

-

Pon Bike

-

Harley Davidson.

SONDORS Financial Performance

The company’s recent financial results can be summarized as follows:

-

Growing topline revenue

-

Increasing gross profit

-

Uneven gross margin

-

Growing operating losses

-

A swing to cash used in operations.

Below are relevant financial results derived from the firm’s registration statement:

|

Total Revenue |

||

|

Period |

Total Revenue |

% Variance vs. Prior |

|

Nine Mos. Ended September 30, 2022 |

$ 16,787,000 |

49.4% |

|

2021 |

$ 16,463,000 |

37.2% |

|

2020 |

$ 11,999,000 |

|

|

Gross Profit (Loss) |

||

|

Period |

Gross Profit (Loss) |

% Variance vs. Prior |

|

Nine Mos. Ended September 30, 2022 |

$ 3,823,000 |

30.9% |

|

2021 |

$ 3,510,000 |

-20.8% |

|

2020 |

$ 4,434,000 |

|

|

Gross Margin |

||

|

Period |

Gross Margin |

|

|

Nine Mos. Ended September 30, 2022 |

22.77% |

|

|

2021 |

21.32% |

|

|

2020 |

36.95% |

|

|

Operating Profit (Loss) |

||

|

Period |

Operating Profit (Loss) |

Operating Margin |

|

Nine Mos. Ended September 30, 2022 |

$ (3,767,000) |

-22.4% |

|

2021 |

$ (4,883,000) |

-29.7% |

|

2020 |

$ (753,000) |

-6.3% |

|

Net Income (Loss) |

||

|

Period |

Net Income (Loss) |

Net Margin |

|

Nine Mos. Ended September 30, 2022 |

$ (4,225,000) |

-25.2% |

|

2021 |

$ (4,892,000) |

-29.1% |

|

2020 |

$ (745,000) |

-4.4% |

|

Cash Flow From Operations |

||

|

Period |

Cash Flow From Operations |

|

|

Nine Mos. Ended September 30, 2022 |

$ (9,454,000) |

|

|

2021 |

$ 5,195,000 |

|

|

2020 |

$ 1,706,000 |

|

(Source – SEC.)

As of September 30, 2022, Sondors had $1.0 million in cash and $29.3 million in total liabilities.

Free cash flow during the twelve months ended September 30, 2022, was negative ($9.4 million).

SONDORS’ IPO Details

Sondors intends to sell 2.5 million shares of common stock at a proposed midpoint price of $9.00 per share for gross proceeds of approximately $22.5 million, not including the sale of customary underwriter options.

No existing or potentially new shareholders have indicated an interest in purchasing shares at the IPO price. The company founder owned 99.2% of company stock pre-IPO.

Assuming a successful IPO at the midpoint of the proposed price range, the company’s enterprise value at IPO (excluding underwriter options) would approximate $118 million.

The float to outstanding shares ratio (excluding underwriter options) will be approximately 16.1%. A figure under 10% is generally considered a “low float” stock which can be subject to significant price volatility.

Per the firm’s most recent regulatory filing, it plans to use the net proceeds as follows:

We currently intend to use up to $3.6 million of the net proceeds of this offering for the repayment of the portion of our Senior Secured Notes (including interest thereon) that are not converted into shares of common stock at the closing of this offering and the remaining $16.3 million of the net proceeds from this offering for new product research and development, existing product development and commercialization, the development of international markets and to fund our growth and to fund other general corporate purposes.

(Source – SEC.)

Management’s presentation of the company roadshow is available here until the IPO is completed.

Regarding outstanding legal proceedings, management said the firm is not presently involved in any legal proceedings that would have a material adverse effect on its financial condition or operations.

The listed bookrunners of the IPO are Lake Street and Joseph Gunnar & Co.

Valuation Metrics For SONDORS

Below is a table of the firm’s relevant capitalization and valuation metrics at IPO, excluding the effects of underwriter options:

|

Measure [TTM] |

Amount |

|

Market Capitalization at IPO |

$140,007,420 |

|

Enterprise Value |

$118,168,420 |

|

Price / Sales |

6.36 |

|

EV / Revenue |

5.37 |

|

EV / EBITDA |

-17.21 |

|

Earnings Per Share |

-$0.46 |

|

Operating Margin |

-31.20% |

|

Net Margin |

-33.31% |

|

Float To Outstanding Shares Ratio |

16.07% |

|

Proposed IPO Midpoint Price per Share |

$9.00 |

|

Net Free Cash Flow |

-$9,377,000 |

|

Free Cash Flow Yield Per Share |

-6.70% |

|

Debt / EBITDA Multiple |

-0.02 |

|

CapEx Ratio |

-8.64 |

|

Revenue Growth Rate |

49.38% |

|

(Glossary Of Terms) |

(Source – SEC.)

Commentary About SONDORS

Sondors is seeking U.S. public capital market investment to pay down debt and fund product development and sales efforts.

The firm’s financials have produced increasing topline revenue, growing gross profit, variable gross margin but increasing operating losses and a swing to cash used in operations.

Free cash flow for the twelve months ended September 30, 2022, was negative ($9.4 million).

Selling and Marketing expenses as a percentage of total revenue have dropped to 9.9% and its Sales and Marketing efficiency multiple was 3.3x in the most recent reporting period.

The firm currently plans to pay no dividends on its capital stock and intends to retain any future earnings to reinvest back into the company’s growth initiatives.

Sondors’ trailing twelve-month CapEx Ratio was negative 8.64, which indicates it has spent on capital expenditures even while generating negative operating flow.

The market opportunity for two wheeled e-transportation is large and expected to grow at a high rate of growth in the coming years, so the firm enjoys a very strong industry growth dynamic in its favor, although it also faces significant competition.

Lake Street is the lead book-running manager, and there is no data on the firm’s IPO involvement over the last 12-month period.

Risks to the company’s outlook as a public company include the potential for a U.S. recession ahead as well as continued high costs for raw materials, transportation and labor.

As for valuation, management is asking IPO investors to pay an EV/Revenue multiple of approximately 5.4x on growing revenue, but an EV/EBITDA of negative (17.2x).

The company’s recent cash flow results have been negatively impacted by a strong growth in inventories.

Going into a likely recession with high inventory is a difficult spot to be in, as it may force the company to discount its products to move the inventory.

E-bikes have become a popular item in recent years, but the industry has no shortage of competitors and some of the more well-capitalized have moved to acquire their own distribution retail stores.

While Sondors has grown revenue, I’m cautious about its profit outlook in the near term as it faces a macroeconomic slowdown with high inventory in a competitive industry.

I’m on Hold for the SODR IPO.

Expected IPO Pricing Date: To be announced

Be the first to comment