Andy

A Quick Take On Intchains

Intchains (ICG) has filed to raise $30 million in gross proceeds from the sale of ADSs representing its Class A common stock in an IPO, according to an amended registration statement.

The company provides ASICs for cryptocurrency mining computers.

Given my negative short-term outlook for crypto pricing, the company’s location in China, quickly slowing growth rate and generally poor performance of Chinese companies post-IPO, my outlook on the ICG IPO is on Hold.

Intchains Overview

Shanghai, China-based Intchains was founded to develop advanced application-specific integrated circuits [ASIC] and related mining algorithms to assist cryptocurrency blockchains and miners.

Management is headed by founder, Chairman and CEO Qiang Ding, who has been with the firm since its inception and was previously director of research at Shanghai InfoTM Microelectronics Co.

The company’s primary offerings are a family of ASIC chips optimized for a variety of blockchain mining algorithms.

Intchains has booked fair market value investment of $26.4 million as of September 30, 2022, from investors including a variety of private capital entities.

Intchains – Customer Acquisition

The firm sells its chips to crypto machine assemblers and seeks to avoid the highly competitive Bitcoin chip market by focusing on other mining algorithms.

The company is also aiming its products at home/small mining rigs and end-user markets, with fewer energy requirements resulting in lower cooling noise generation.

Sales & Marketing expenses as a percentage of total revenue have risen as revenues have increased, as the figures below indicate:

|

Sales and Marketing |

Expenses vs. Revenue |

|

Period |

Percentage |

|

Nine Mos. Ended September 30, 2022 |

0.7% |

|

2021 |

0.5% |

|

2020 |

0.2% |

(Source – SEC)

The Sales & Marketing efficiency multiple, defined as how many dollars of additional new revenue are generated by each dollar of Sales & Marketing spend, was 34.9x in the most recent reporting period.

|

Sales and Marketing |

Efficiency Rate |

|

Period |

Multiple |

|

Nine Mos. Ended September 30, 2022 |

34.9 |

|

2021 |

191.5 |

(Source – SEC)

Intchains’ Market & Competition

According to a 2022 market research report by Brand Essence Research, the global cryptocurrency mining hardware market was an estimated $2.3 billion in 2021 and is forecast to reach nearly $5.3 billion by 2028.

This represents a forecast CAGR of 28.5% from 2022 to 2028

The main drivers for this expected growth are a growth in the use of cryptocurrencies by consumers and an increase in the number of applications used by blockchain technologies.

Also, the market share for ASICs has historically been a majority of the market for several years now while the pace of chip technology advancement has generally slowed in recent years as many early gains have already been commoditized.

The overall ASIC chip market is fairly fragmented, with some sectors more concentrated than others.

Management says the firm’s ASICs have ‘dominated the computing power of several algorithms commonly used for alternative cryptocurrencies in terms of the accumulative computing power sold for the years of 2019, 2020 and 2021,’ although I could not independently confirm that.

Intchains Group Limited Financial Performance

The company’s recent financial results can be summarized as follows:

-

Rising topline revenue at a decelerating rate of growth

-

Growing gross profit and gross margin

-

Stable operating profit

-

Growing cash flow from operations

Below are relevant financial results derived from the firm’s registration statement:

|

Total Revenue |

||

|

Period |

Total Revenue |

% Variance vs. Prior |

|

Nine Mos. Ended September 30, 2022 |

$ 61,865,000 |

31.1% |

|

2021 |

$ 88,822,000 |

1038.7% |

|

2020 |

$ 7,800,429 |

|

|

Gross Profit (Loss) |

||

|

Period |

Gross Profit (Loss) |

% Variance vs. Prior |

|

Nine Mos. Ended September 30, 2022 |

$ 52,442,000 |

29.8% |

|

2021 |

$ 72,802,000 |

1529.6% |

|

2020 |

$ 4,467,429 |

|

|

Gross Margin |

||

|

Period |

Gross Margin |

|

|

Nine Mos. Ended September 30, 2022 |

84.77% |

|

|

2021 |

81.96% |

|

|

2020 |

57.27% |

|

|

Operating Profit (Loss) |

||

|

Period |

Operating Profit (Loss) |

Operating Margin |

|

Nine Mos. Ended September 30, 2022 |

$ 45,232,000 |

73.1% |

|

2021 |

$ 62,882,000 |

70.8% |

|

2020 |

$ 790,714 |

10.1% |

|

Comprehensive Income (Loss) |

||

|

Period |

Comprehensive Income (Loss) |

Net Margin |

|

Nine Mos. Ended September 30, 2022 |

$ 48,155,000 |

77.8% |

|

2021 |

$ 63,278,000 |

102.3% |

|

2020 |

$ 1,178,143 |

1.9% |

|

Cash Flow From Operations |

||

|

Period |

Cash Flow From Operations |

|

|

Nine Mos. Ended September 30, 2022 |

$ 44,452,000 |

|

|

2021 |

$ 55,587,000 |

|

|

2020 |

$ 2,226,571 |

|

(Source – SEC)

As of September 30, 2022, Intchains had $98.8 million in cash and $2.9 million in total liabilities.

Free cash flow during the twelve months ended September 30, 2022, was $68.1 million.

Intchains’ IPO Details

ICG intends to sell 3.75 million ADSs representing 2x shares of underlying Class A common stock at a proposed midpoint price of $8.00 per ADS for gross proceeds of approximately $30.0 million, not including the sale of customary underwriter options.

No existing or potentially new shareholders have indicated an interest in purchasing shares at the IPO price.

Class A stockholders will be entitled to one vote per share and Class B shareholders (the two founders) will receive ten votes per share and will have voting control of the company immediately post-IPO.

The S&P 500 Index no longer admits firms with multiple classes of stock into its index.

Assuming a successful IPO at the midpoint of the proposed price range, the company’s enterprise value at IPO (excluding underwriter options) would approximate $377 million.

The float to outstanding shares ratio (excluding underwriter options) will be approximately 6%. A figure under 10% is generally considered a ‘low float’ stock which can be subject to significant price volatility.

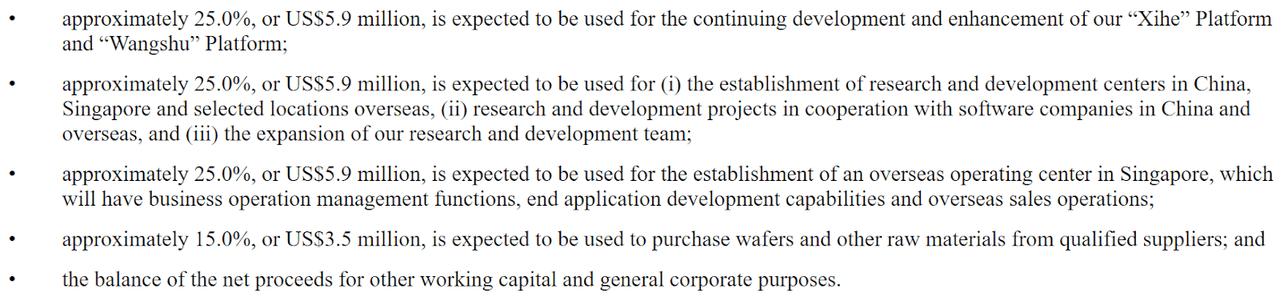

Per the firm’s most recent regulatory filing, it plans to use the net proceeds as follows:

Proposed Use Of IPO Proceeds (SEC)

(Source – SEC)

Management’s presentation of the company roadshow is not available.

Regarding outstanding legal proceedings, management says the firm is not currently a party to any legal or administrative proceedings that would have a material adverse effect on its financial condition or operations.

The sole listed bookrunner of the IPO is Maxim Group.

Valuation Metrics For Intchains

Below is a table of the firm’s relevant capitalization and valuation metrics at IPO, excluding the effects of underwriter options:

|

Measure [TTM] |

Amount |

|

Market Capitalization at IPO |

$499,188,000 |

|

Enterprise Value |

$376,797,000 |

|

Price / Sales |

4.82 |

|

EV / Revenue |

3.64 |

|

EV / EBITDA |

5.21 |

|

Earnings Per Share |

$1.20 |

|

Operating Margin |

69.94% |

|

Net Margin |

72.94% |

|

Float To Outstanding Shares Ratio |

6.01% |

|

Proposed IPO Midpoint Price per Share |

$8.00 |

|

Net Free Cash Flow |

$68,091,857 |

|

Free Cash Flow Yield Per Share |

13.64% |

|

CapEx Ratio |

145.52 |

|

Revenue Growth Rate |

31.10% |

(Source – SEC)

Commentary About Intchains

ICG wants to tap U.S. capital markets for its continued platform development, R&D efforts and growth initiatives.

The firm’s financials have produced increasing topline revenue at a decelerating rate of growth, rising gross profit and gross margin, flat operating profit and increasing cash flow from operations.

Free cash flow for the twelve months ended September 30, 2022, was $68.1 million.

Sales and Marketing expenses as a percentage of total revenue rose as revenue has increased and its Sales and Marketing efficiency multiple was 34.9x in the most recent reporting period.

The firm currently plans to pay no dividends on its capital stock and anticipates that it will retain any future earnings to reinvest back into the business.

The firm‘s trailing twelve-month CapEx Ratio was 146x, which indicates it has spent lightly on capital expenditures as a percentage of its operating cash flow.

However, based on the proposed use of proceeds, it is likely the company will spend much more heavily on CapEx in the near future.

The market opportunity for crypto ASICs is large and expected to grow substantially in the coming years, although recent volatility in the price of major crypto assets has filtered through to reduced demand for ASICs.

Like other firms with Chinese operations seeking to tap U.S. markets, the firm operates within a WFOE structure or Wholly Foreign Owned Entity. U.S. investors would only have an interest in an offshore firm with interests in operating subsidiaries, some of which may be located in the PRC. Additionally, restrictions on the transfer of funds between subsidiaries within China may exist.

The recent Chinese government crackdown on IPO company candidates combined with added reporting and disclosure requirements from the U.S. has put a serious damper on Chinese or related IPOs resulting in generally poor post-IPO performance.

Also, a potentially significant risk to the company’s outlook is the uncertain future status of Chinese company stocks in relation to the U.S. HFCA act, which requires delisting if the firm’s auditors do not make their working papers available for audit by the PCAOB.

Prospective investors would be well advised to consider the potential implications of specific laws regarding earnings repatriation and changing or unpredictable Chinese regulatory rulings that may affect such companies and U.S. stock listings.

Additionally, post-IPO communications from the management of smaller Chinese companies that have become public in the U.S. has been spotty and perfunctory, indicating a lack of interest in shareholder communication, only providing the bare minimum required by the SEC and a generally inadequate approach to keeping shareholders up-to-date about management’s priorities.

Maxim Group is the sole underwriter, and IPOs led by the firm over the last 12-month period have generated an average return of negative (67%) since their IPO. This is a bottom-tier performance for all significant underwriters during the period.

Risks to the company’s outlook as a public company include the ongoing volatility in crypto prices as well as a shift by some blockchains toward less mining-intensive protocols that use Proof of Stake consensus systems.

As for valuation, management is asking investors to pay an Enterprise Value / Revenue multiple of around 3.6x on revenue growth that is decelerating quickly.

Given my negative short-term outlook for crypto pricing, the company’s location in China, quickly slowing growth rate and generally poor performance of Chinese companies post-IPO, my outlook on the ICG IPO is on Hold.

Expected IPO Pricing Date: December 27, 2022.

Be the first to comment