Introduction

The current market environment has been unsettling, to say the least. U.S. equity markets have fallen around 30% from their February peak (as of March 16, 2020), and in a very short time period of time. Global markets have followed suit, dramatically impacting return-seeking investments and the asset values of all investors.

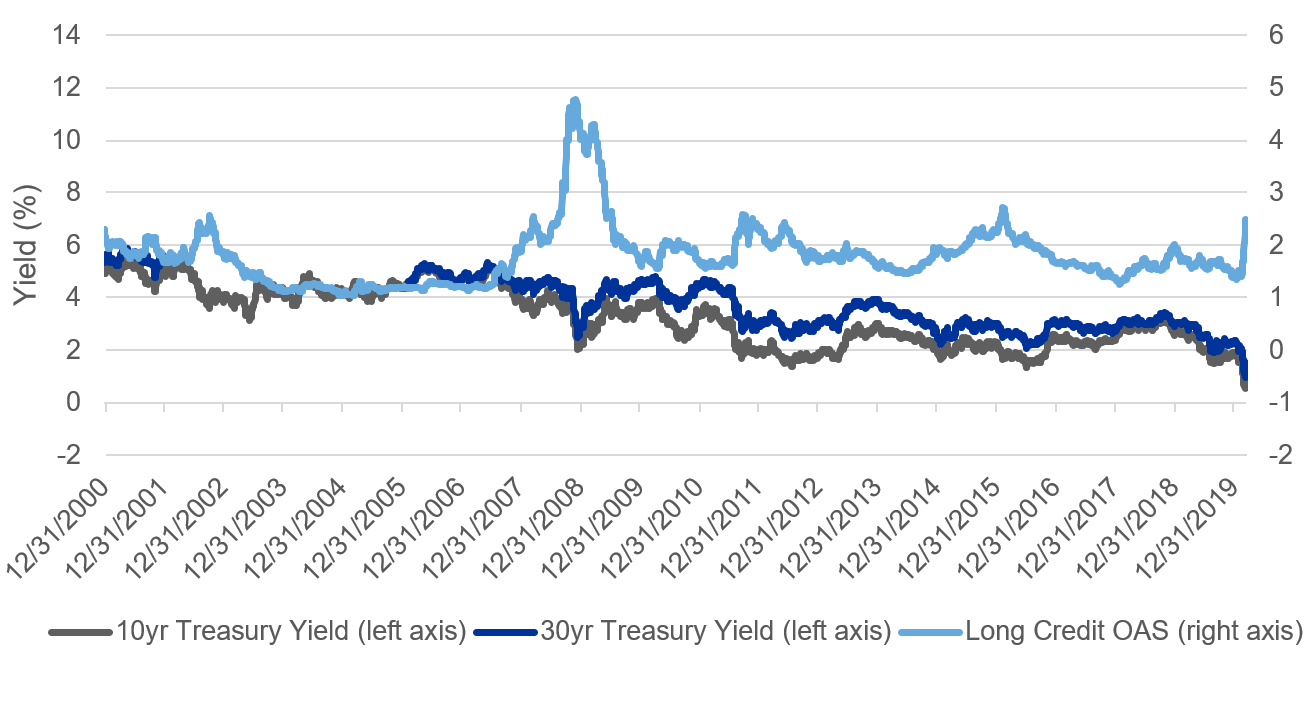

At the same time, U.S. Treasury yields have fallen dramatically to historic lows. This has resulted in significant returns to holders of these bonds. However, as is typical in risk-off events, credit spreads widened at the same time as these Treasury yields fell. As a result, credit-based fixed income investments haven’t fared as well.

Historical Treasury Yields & Investment Grade Credit Spreads

{kind=link}

Source: U.S. Department of TreasuryChart data current as of March 13, 2020

The impact of these market moves differs by investor type. For example, the fixed income exposures of non-profit investors tend to be more focused on credit-oriented exposures. While these assets may not have performed particularly well recently, return impacts have still been dwarfed by equity losses, such that investors will still find themselves overweight fixed income assets. In contrast, many defined benefit (DB) plans – particularly those with liability-hedging programs incorporating long-duration Treasuries and STRIPS – will find themselves considerably more overweight fixed income relative to equity. Given the magnitude of these market moves and the extremely uncertain investment environment, many clients are asking if their portfolios should be rebalanced, or even if they should be targeting a different allocation during these turbulent times.

The importance of an appropriate long-term investment strategy

Asset owners conceptually understand that the overwhelming majority of desired investment outcomes will be determined by the asset allocation strategy documented in their Investment Policy Statement. While it is easier to rely on these implementation parameters in periods of normal volatility, we believe it is critical to minimize second guessing them when markets become volatile and risk becomes truly palpable. In these environments, concept must become reality. Investors need to lean on their established asset allocation policies as an anchor for decision making. We have a lot more confidence in such strategic investment policies, which have typically been developed based on an analysis of risk and reward trade-offs, consideration of unique client goals and circumstances, and informed by fairly stable asset class behaviors over the long term. Such strategic decisions have served clients well – including the management of liability-relative interest rate risks by pension plans, which has mitigated impacts to funded status over time. This is particularly so in the recent weeks for those plans using long Treasuries/STRIPS to achieve even greater liability hedging and significant tail-risk protection. However, on the equity side, only well-funded plans that followed a de-risking glide path to a much lower risk posture would have avoided the brunt of the recent equity decline.

Nevertheless, the current market environment is unique in that we are in uncharted territory – at least for the U.S., with 10-year Treasuries yielding under 1%. The speed and magnitude of the equity market decline from the recent peak have also been extraordinary. This is clearly an evolving situation and one in which clients naturally ask whether they should be doing something different. To the extent clients do want to consider adjustments to their strategic investment allocations, potentially tactically, we should all accept that we have less confidence and conviction with respect to how asset classes behave when rates are at extremely low levels and in such a volatile environment.

- Equity markets could rally significantly if economic risks and COVID-19 concerns fade – especially with recent accommodative policy responses. However, equity markets could easily fall further from here in another leg down, based on uncertainty over the length and magnitude of economic impacts.

- Similarly, with respect to fixed income, while the recent decline in yields appears overly precipitous with a potential to revert higher, we have certainly seen rates go significantly lower or negative in some markets outside the U.S. This suggests there is still potential future benefit to Treasury exposures, even from here – particularly from a short or medium-term risk management perspective.

These comments are directionally bifurcated to test conviction in any views – if any adjustments are desired – and to ensure that any such decisions are made deliberately, relative to an established strategic policy. The size of any deviations should be subject to an appropriate risk budget, determined by conviction levels. Of course, as with any shift away from strategic policy, clients will also need to consider a plan to migrate back, as appropriate.

Rebalancing

As to the question of rebalancing – and absent any deliberate change in investment policy (see special considerations for DB plans next) – we believe intended policy exposures should be maintained via rebalancing.

Indeed, given that virtually all investors will be underweight equity, we would note that current U.S. equity valuations are now much closer to longer-term norms than was the case earlier this year, while non-U.S. stocks are relatively cheaper again. This influences the potential return outlook over medium-to-long-term horizons and, on balance, provides further support for rebalancing into equity. Of course, as noted earlier, there is concern and uncertainty surrounding the underlying equity earnings and cash-flow outlook, and ongoing/elevated draw-down risk. So going beyond target to an overweight equity position is a different proposition which should be sized appropriately, should investors so decide.

Similarly, given the remarkable decline in Treasury yields, DB plans that have been hedging primarily with long Treasuries/STRIPS will have accrued significant value, particularly relative to a corporate discount rate. With 10-year Treasuries yielding below 1%, the market is embedding a view that the U.S. Federal Reserve (the Fed) will keep rates low for an extended period of time. It is yet to be seen whether such Treasury exposures will continue to have as much efficacy as a tail-risk hedge against equity risk-off events at such low levels, though they will continue to play a role in hedging interest rate risk. To be clear, in further risk-off scenarios (if this current environment worsens), fixed income investments could still meaningfully outperform equity, but there is likely less cushion to be used as an offset, given the potential magnitude of any downward rate moves is more limited. This will be mitigated somewhat by the increase in duration of fixed income assets as interest rates fall, a phenomenon known as convexity. It is unclear how low U.S. rates could go relative to the Fed’s desire, or lack thereof, for negative rates.

Of course, for both pensions and non-profits, credit-oriented fixed income exposures are now offering higher yields than earlier in the year, but they have certainly not reached anywhere near the outsized opportunities offered in 2008-2009. Nevertheless, in the pension case – if there is a mix of credit and Treasuries/STRIPS exposures – the extent of recent Treasury moves would suggest STRIPS exposure as the funding choice for rebalancing requirements.

All else being equal, we would advocate that clients rebalance to policies where appropriate. However, one additional consideration that we are watching closely is liquidity levels and associated trading costs, particularly with respect to fixed income investments. Liquidity has been constrained as market volatility has increased, with bid/ask spreads increasing materially across fixed income markets. As such, the cost of rebalancing should be carefully considered prior to implementation.

Special Considerations for DB Plans

Given a solid long-term plan for the return-seeking allocation vs. liability hedging, DB plans have a unique follow-on question: Should the nature and underlying structure of the liability-driven investing program evolve, as we navigate through this volatile market environment? How that question is answered depends largely on the current circumstances of the defined benefit plan and the health of the sponsoring organization.

For well-funded plans that have most of their assets allocated to liability-hedging fixed income and that have hedged a large percentage of their interest rate volatility1, the likely response is to stay the course. There is little benefit in trying to time interest rate reversals, and the potential for trapped capital – in the event of a plan termination – means there is little to no utility in having a large amount of excess assets. That said, another consideration is raising cash from the fixed income portfolio in order to fund future benefit payment obligations. Any plan with exposure to (particularly long-dated) Treasury STRIPS likely finds itself overweight that asset class. Selling these assets to provide several months’ worth of benefit payments results in very little give-up in portfolio yield, given the current flat yield curve.

Poorly funded plans in the midst of extending the duration of the composite fixed income portfolio may want to pause in the face of current market volatility. Extending asset duration beyond that of the liability often involves buying long-dated Treasury STRIPS. Treasury yields at or near historic lows means that the portfolio would be rotating into a relatively expensive asset class that has just hugely increased in value. This may, though, be an opportunity to examine the relative weights of credit and Treasury duration in the portfolio. With credit spreads having widened meaningfully in the past several days – though still well below the highs of the Global Financial Crisis – there may be an opportunity to capture incremental return if spreads start to tighten.

Those plans in an in-between state have the most difficult path to navigate. Their response to the current market environment depends on several factors. If the corporation cannot withstand further large downside shocks to funded status, it may still make sense to increase the plan’s hedge ratio.2 The relative focus of the plan sponsor on cash contributions vs. mark-to-market balance sheet impacts will also influence allocation decisions. Current market dislocations will have very little-if-any impact on near-term contribution requirements for plans with a calendar-year valuation cycle. Funding relief means that discount rates are essentially already fixed for the coming year, the availability of asset smoothing will blunt the impact of market declines, and any contribution requirements may not be due for up to 20 months following the beginning of the next plan year.

Finally, as was the case with rebalancing, any potential tactical changes in portfolio positioning should consider the expense of buying and selling the underlying securities, to ensure any perceived benefits of repositioning are not precluded by trading costs.

Disclosures

¹ Also commonly referred to as the plan’s hedge ratio

² This comment also applies to poorly funded plans described in the previous paragraph

Nothing contained in this material is intended to constitute legal, tax, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. The general information contained in this publication should not be acted upon without obtaining specific legal, tax, and investment advice from a licensed professional.

These views are subject to change at any time without notice based upon market or other conditions and are current as of the date at the top of the page. It is made available on an “as is” basis. Russell Investments does not make any warranty or representation regarding the information. While all material is deemed to be reliable, accuracy and completeness cannot be guaranteed. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This is not an offer, solicitation, or recommendation to purchase any security or the services of any organization.

AI-28121

Be the first to comment