Tomas Ragina/iStock via Getty Images

Transcript

What is the outlook for traditional energy?

William Su, Senior Analyst, U.S. Income & Value team

The Ukraine crisis has amplified an already under-supplied situation in the oil and gas markets. In our view, the big winner will be U.S. natural gas producers and exporters, who will send rapidly growing volumes of LNG (Liquified Natural Gas) to Europe as the continent weans off of Russian gas, hoping to close an 80% pricing discount and drive very high cash flows for years to come.

What is the outlook for defense stocks?

Rolf Heitmeyer, Equity Research Analyst, U.S. Income & Value team

Due to Ukraine, the U.S. defense budget is likely to see mid-single-digit growth versus a prior base case of low-single-digit growth. As a result, defense stocks have sharply rallied and now, for the most part, adequately reflect the higher outlook. However, we continue to find individual opportunities in this space.

What are the effects of increased cyber aggression?

Reid Menge, Portfolio Manager, Global Technology team

Cyber aggression is a growing and serious threat to governments, companies and individuals around the world. We see potential for 40% upside in some IT security providers and favor best-of-breed vendors in each subcategory, including network security, identity security and “zero-trust” security architecture.

Where can impact investing be applied?

Flora Cameron Watt, Impact Analyst, Global Impact team

The human suffering brought on by the war has increased the need to find solutions to provide access to food, shelter, and critical skills. In addition to investing in companies that are providing affordable food, homes, job placements, language skills, and financial literacy, we are also supporting companies through engagement, leading strategic introductions in the hope of finding new solutions to meet some of these unique challenges being felt across the globe.

_________________

The war in Ukraine is raising questions across disciplines, even as hearts and minds are first focused on the human tragedy of the crisis. Investors from BlackRock Fundamental Equities offer insight on the implications for key sectors and investment themes.

- Selectivity is critical in defense stocks after recent appreciation

- We see a favorable longer-term outlook for oil and gas prices

- Cyber threats support the outlook for IT security providers

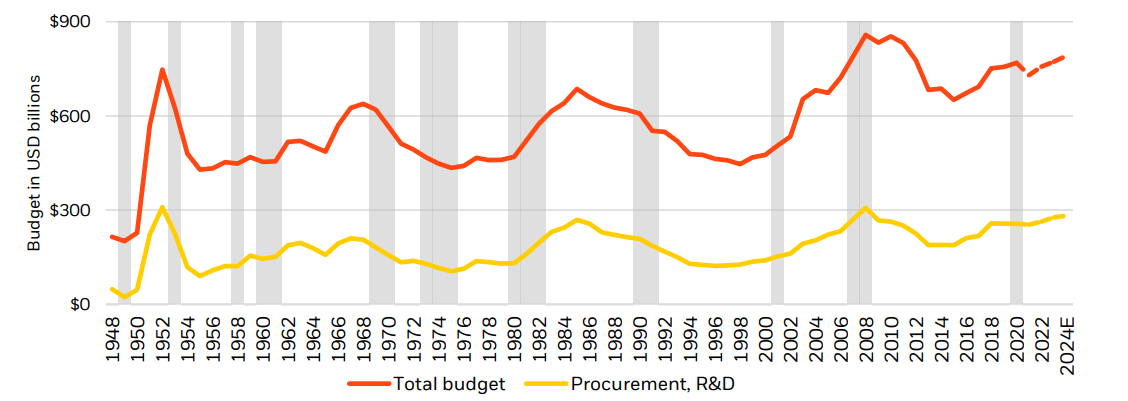

Defense spending and investment

A number of crosscurrents are affecting the investment thesis in the defense industry today. Across time, peaks in U.S. defense spending have correlated to active U.S. conflicts as well as the Cold War and have not been directly related to the broader economic picture, as shown in the chart below.

Prior to Russia’s invasion of Ukraine, U.S. defense spending was already elevated for an environment without active conflict. Given the higher base, we believe the outlook for growth in both total defense budgets and investment spending in the space is lower than might typically be the case in wartime.

Defense spending across time

U.S. defense budget, 1948-2024E

Figures shown are in USD billions and inflation-adjusted. Shaded areas represent recessions. (BlackRock Fundamental Equities, with data from the U.S. Department of Defense, as of April 2022)

The situation differs somewhat in Europe. Many NATO members had spent less than the agreed upon 2% of their GDP on defense. If the laggards move to the 2%, we could see $80 billion in additional defense spending, a 25% increase.

More important to investors is the growth in spending on equipment and procurement within the defense budget. This element, which drives orders and revenues for companies, is expected to outgrow the headline budget increases. The magnitude would vary significantly by market. For example, Germany could see the biggest uptick while France should see a continuation of the solid budget growth witnessed in recent years.

Capacity constraints are an issue, limiting growth potential. For one, defense companies can’t hire engineers fast enough. Then there are environmental, social and governance (ESG) concerns, which have long been an issue for the industry. We saw the tide beginning to turn before the invasion, and the war has reinforced the realization that defense is necessary for the maintenance of stable democracies and, thereby, ESG security. This sentiment change could give defense some positive rerating.

Key takeaway: The war does not necessarily affirm the investment case for defense stocks, particularly after a recent sharp multiple expansion. Given the many considerations and crosscurrents at play, selectivity is especially important today.

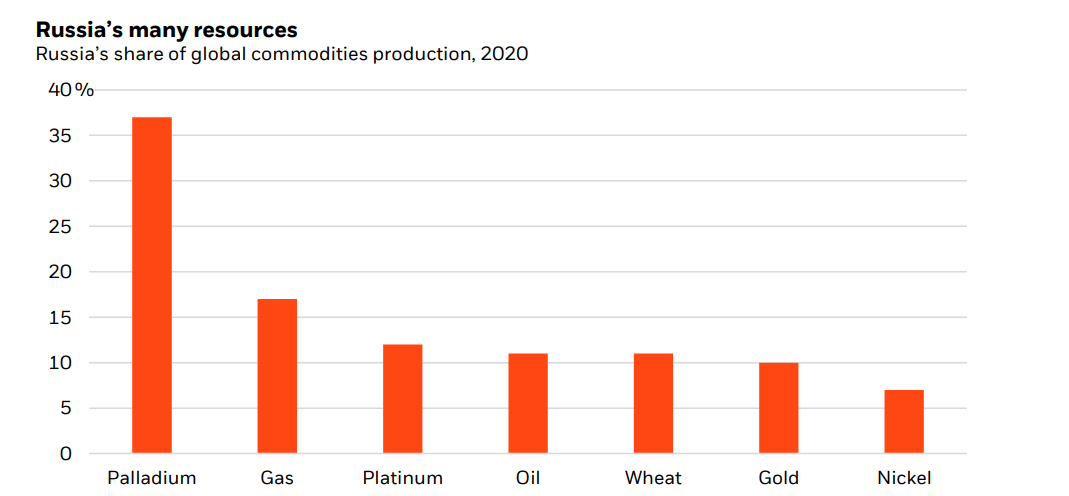

Energy independence and transition

Russia is a major global commodity producer ― everything from oil and natural gas to palladium, platinum, gold, and nickel, as shown in the chart below. In the near term, a key consequence of the war is the need for Europe to establish energy independence. Europe gets roughly 40% of its natural gas from Russia. The aim is to reduce that reliance by two-thirds in one year and to be fully energy independent by 2030. The one-year goal is a tall order.

Europe will look to achieve its ambitions through various means: improved energy efficiency; new gas imports, which will take time to get online; thermal coal consumption, which will be challenging due to underinvestment; and increased renewable spend, fast-tracking the plans already in place.

Green or sustainable metals, such as copper, are poised to benefit as the backbone of the decarbonization story. We are seeing increased copper demand in green spending areas such as electric vehicles, solar and wind. Estimates suggest demand from these areas is set to more than double by the end of the decade* ― and new copper supply will be challenged to keep up.

Key takeaway: The crisis contributes to a growing recognition of the strategic significance of metals and commodities, as well as the importance of having a domestic resources base and stockpiles. We believe the sector should benefit in the near term from inflation, tight commodity markets and strong earnings from mining companies. We also see exciting longer-term implications playing out over the next decade.

Russia’s many resources

Russia’s share of global commodities production, 2020

Morgan Stanley, Goldman Sachs, JPMorgan Chase, Haver Analytics, and Wood Mackenzie, February 2022

*Based on data and analysis from Wood Mackenzie, CRU Group, and Goldman Sachs Global Investment Research, as of Oct. 31, 2021.

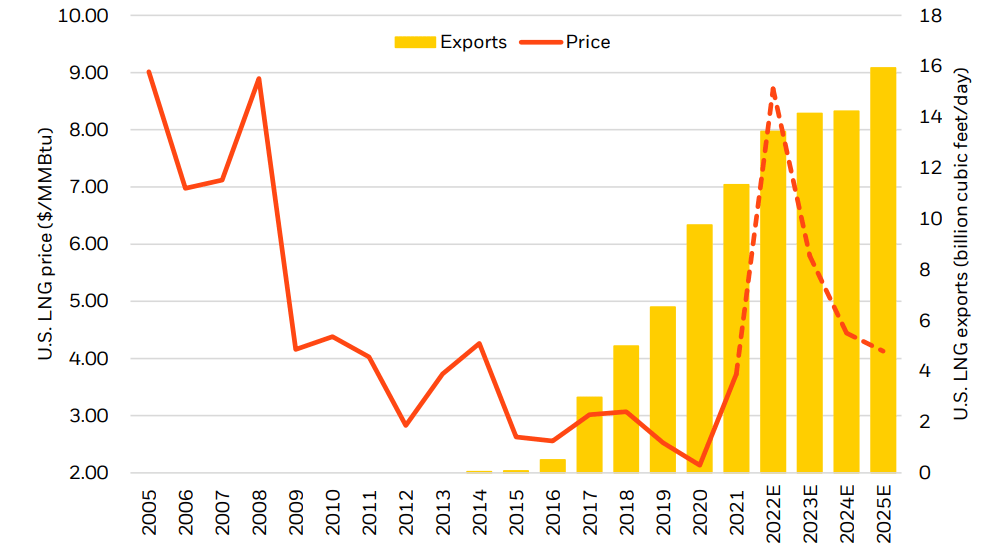

The path out of a 15-year bear market?

Liquefied Natural Gas (LNG) prices and exports, 2005-2025E

LNG prices are U.S. Henry Hub natural gas prices (Bloomberg, EIA, and BlackRock Fundamental Equities estimates, as of May 2022)

The outlook for traditional energy

The near-term direction of the oil price is difficult to forecast amid significant volatility. Russian oil flows are so far down one million barrels/day, but we see the potential for another one million barrel daily loss in the coming months as supply contracts wind down.

Longer term, we are confident in the sustained strength in energy prices due to the growing recognition that oil and gas will be needed for longer than the consensus believes as the energy transition advances.

Gas is the more interesting story, as U.S. exports stand to benefit from Europe’s move away from Russian gas. Currently, U.S. liquefied natural gas (LNG) exports account for roughly 15% of gas produced, up from essentially zero in 2015. (See chart above.)

U.S. natural gas has rallied since the start of the war but is still expected to trade at only 20% of European gas prices in 2023. A strategic partnership with Europe would increase LNG exports and, we believe, drive further upside in U.S. gas prices after a 15-year bear market. We estimate that a structural rise in natural gas prices to $5/MMBtu could propel roughly 100% upside for some major gas producers.

One unique and attractive characteristic of natural gas is its historically recession-resistant nature: More than 70% of gas is used for infrastructure needs, heating, and power generation in the U.S., according to the Energy Information Administration (EIA). The remainder is used in the industrial production of essential chemicals, fertilizers, and steel.

Data from the International Energy Agency (IEA) shows that in 2020 when the world shut down amid the COVID-19 pandemic, oil demand fell 12% whereas natural gas demand was down only 1% and LNG demand rose 2%.

Gas production also has an inverse relationship with oil production: 40% of U.S. supply is known as “associated gas” and comes “free” from oily basins like the Permian in the southwest U.S. This means natural gas supply will fall if oil prices drop in a recession, adding to the attractive risk/reward in what is arguably the most recession-proof commodity.

Key takeaway: We see a favorable longer-term outlook for oil and gas prices, even as the netzero transition unfolds. Companies exhibiting both organic growth and production volume offer resilience ― they should do relatively well in an environment where demand remains strong as well as a scenario in which prices begin to drift lower over time.

The cloud of cyber aggression

Russia under Vladimir Putin has adopted a hybrid form of fighting that combines conventional military force with unconventional means such as cyberattacks. Cyber aggression was seen in the invasions of Georgia in 2008 and Crimea in 2014. In 2015 and 2016, Russian hackers shut down Ukraine’s electricity grid. The 2020 U.S. Colonial Pipeline hack was also Russian sponsored and led to gas shortages on the East Coast of the U.S.

With the imposition of crippling sanctions by the U.S. and other nations, Russia has no means to attack under conventional methods. This has stirred concern about cyberattacks. Our research shows the average time it takes from initial infection to virus discovery is 90 days. The idea that attacks have been implanted and are yet to be revealed is worrisome. We could see alarming headlines by summer.

In the past, every major hack or threat has prompted a reflexive surge in spending by companies in the form of purchase orders for security software. Given the looming threat, we expect this war will be a demand driver. Vendors know that cyber is an existential threat to business: We’ve seen company stock prices fall significantly on the news of a hack. This makes a strong case for exposure to stocks in the IT security space, including network security and identity security.

Key takeaway: Cyber aggression is a growing and serious threat to governments, companies, and individuals around the world. We see the potential for a 40% upside in some IT security providers and favor best-of-breed vendors in each subcategory, including network security, identity security, and “zero-trust” security architecture.

Investments with impact

The human suffering brought on by the war has increased the need for solutions to humanitarian challenges felt across the globe. The crisis has significantly disrupted the global food chain, contributing to the sharp rise in food prices. This amplifies the need to provide solutions, such as affordable groceries, to support both communities and those finding innovative ways to tackle food availability and reduce reliance on imports.

We also see rising demand for affordable housing, particularly among companies providing homes to lower-income populations in Europe as the refugee crisis grows alongside a rising cost of living. Amid a significant increase in the number of displaced people, we see growing demand for companies offering services in language skills, job placements, and financial literacy to ensure decent work and financial well-being are attainable for uprooted and underserved populations.

Key takeaway: The war highlights the crucial needs in areas such as food, shelter, and critical skills. In addition to investing in companies that can help to solve these needs, we are also lending support through engagement. This includes leading strategic introductions to find new solutions that address some of the unique challenges brought on by the crisis.

A time for resilience

Uncertainty is high and the questions facing investors are complex. An unprovoked and horrific war has applied new pressures to a global system that was looking to emerge from pandemic malaise, normalize interest rates and process the effects of the highest inflation seen in decades.

As we discuss in our latest market outlook, the prevailing backdrop highlights the importance of building resilience into portfolios. We believe this is best achieved through diversification and a focus on quality – particularly stocks of companies with strong balance sheets and healthy free cash flow characteristics.

Be the first to comment