Thesis

Intuitive Surgical (ISRG) is a Strong Buy after the recent market plunge. In late February, ISRG was trading above $600 at a valuation that was arguably higher but understandable given the company’s strong revenue growth profile. Less than four weeks later, we’ve hit a new 52-week low of $370 due to the Covid-19 market selloff.

In addition to travel restrictions that could dampen sales efforts, I believe one of the core reasons ISRG is selling off is due to its reliance on elective surgeries (non-emergencies). More than half of the surgeries performed on ISRG’s da Vinci system are elective surgeries. And many hospitals are postponing elective surgeries to deal with the potential dramatic rise in Covid-19 cases.

Intuitive Surgical doesn’t just sell surgical robots. More than 70% of the company’s revenue comes from selling instruments and accessories that must be purchased from Intuitive by hospitals for future robot surgeries. So, if surgery volume declines, the company’s recurring revenue stream takes a hit as well.

While we may see a surge in Covid-19 hospital cases, and further delays of an elective surgery as a result, I view this temporary blip as a strong reason to buy shares of ISRG. Elective surgery volumes, typically the lowest in Q1 regardless, will likely return to normal inside of a year. General market fears will lift as Covid-19 hits the rearview mirror. In the meantime, ISRG has an excellent balance sheet and nearly $6 billion in cash to ride the Covid-19 roller coaster.

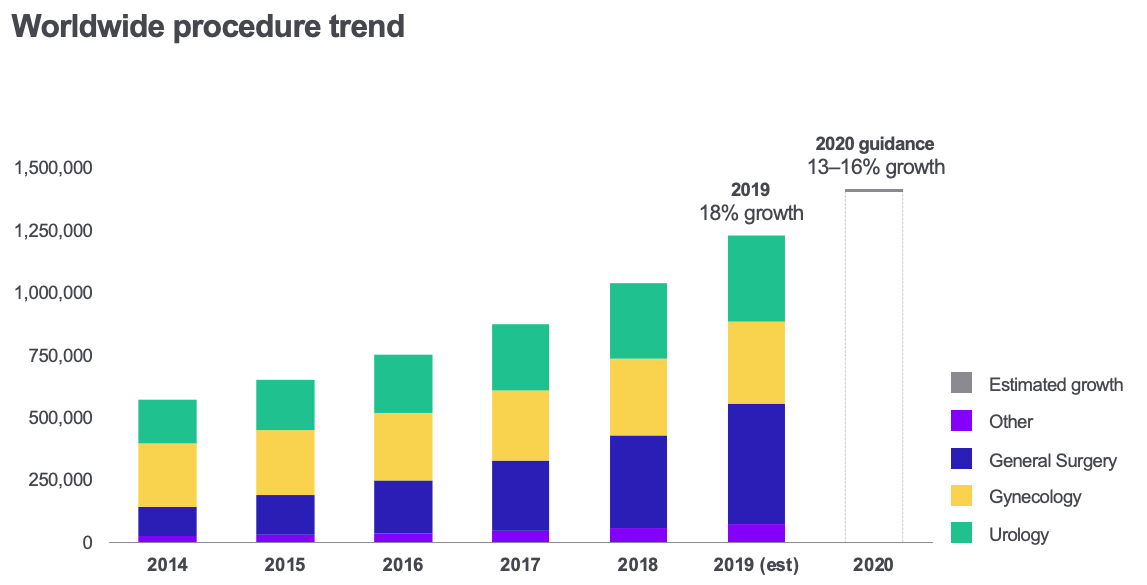

Elective Surgery Is Big Business For ISRG

Intuitive Surgical has 5,582 da Vinci surgical robots installed globally. Of these, 3,531, or 63%, are in U.S. healthcare facilities.

Most of the procedures performed using the da Vinci surgical robot are to treat benign conditions, like hernia repairs, hysterectomies, and cholecystectomies. These are elective surgeries that are not life-critical. In the U.S., the bulk of these procedures are actually done end of year, when more patients have met annual health plan deductibles, and fewer are done in the first quarter of the year, when deductibles are reset.

As Covid-19 spreads, more hospitals are delaying elective surgeries to make room for a potential surge in virus patients. In some cases, patients themselves are canceling elective surgeries because they don’t want to face exposure to Covid-19 by entering a hospital. A reduction in elective surgery volume will likely impact Intuitive in the short term. Fewer elective surgical procedures will result in lower demand from hospitals for the Intuitive Surgical consumables needed to support procedures. More than 70% of company revenue comes from the recurring sales of these consumables.

Of course, the silver lining here for the company is timing. The bulk of U.S. elective surgeries tend to come later in the year. This virus outbreak will likely peak before we enter the second half of 2020. While it remains to be seen how long Covid-19 will be a problem, the impact on Intuitive could be limited due to both timing in the year (Q1-Q2) and the likelihood that Covid-19 could be greatly minimized before year end.

Why Intuitive Is A Strong Buy

Intuitive Surgical is the undisputed leader in robotic-assisted surgery. The company has nearly 6,000 robots deployed worldwide and has a 20-year head start on competing technologies, of which several are being developed by major medical device manufacturers. Intuitive has a strong competitive advantage due to its early-mover advantage, which includes the distinction that doctors around the world are trained to use Intuitive robots. The company has a rock-solid balance sheet and nearly $6 billion in cash to weather the Covid-19 storm, should things get worse before they get better.

Last year, the company grew revenue by 20%, and it is on pace to eclipse $5 billion in sales this year. I believe we are still in the early innings of robot-assisted surgery and Intuitive will remain a leading player for decades to come.

{kind=link}

(Source)

At $600+, Intuitive Surgical was arguably overvalued. The company has always traded at a steep valuation premium, thanks to its strong revenue growth, strong recurring revenue stream, lack of a key competitor, and a massive runway for growth. Its average forward P/E over the last five years has been 45. Today, we’re at 35. I would argue this is a great buying opportunity that may not repeat itself for a while once the Covid-19 scare passes.

My initial cost basis was in the low $500s in 2019. As shares began to crater below $500, I started buying more and topped out my stake below $400 this morning, March 17, which is hopefully the bottom.

If shares continue to dip below $400, I may add more.

Conclusion

Extreme selloffs are the best time to buy great companies like Intuitive Surgical. The long-term investment thesis for ISRG remains solid, and the recent selloff is a gift to anybody looking for a market-crushing long-term investment option.

Disclosure: I am/we are long ISRG. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment