gorodenkoff/iStock via Getty Images

After a brief jump to its 52-week high of $39.98 on February 9, 2022, The Interpublic Group of Companies, Inc. (NYSE:IPG), after pulling back some, had three triple tops of approximately $37.00 per share, before correcting to its 52-week low of $25.14 per share.

Since reaching its 52-week low on September 27, 2022, the company has enjoyed a strong run to a little under $36.00 per share and is poised to test its triple top of $37.00 per share in the near term.

TradingView

Coming off a quarter where it beat on the top and bottom lines, there have been signs of concerns from some of its customers over how to go forward in the challenging economic environment, which looks like it’s likely to get worse before getting better.

In this article, we’ll look at its last earnings report, and the challenges the company faces in 2023 from expectations the economy is going to pressure companies to make spending decisions based upon weaker revenue and earnings results.

Some of the numbers

Total revenue in the third quarter of 2022 was $2.64 billion, compared to total revenue of $2.54 billion in the third quarter of 2021.

Adjusted EBITDA in the quarter was $356.2 million, producing a revenue margin of 15.5 percent.

Net income in the reporting period was $258.1 million, or $0.64 per share per diluted share, compared to $239.9 million, or $0.60 per diluted share in the third quarter of 2021.

Cash and cash equivalents at the end of the third quarter of 2022 was $1.77 billion, compared to $3.27 billion and the end of calendar 2021.

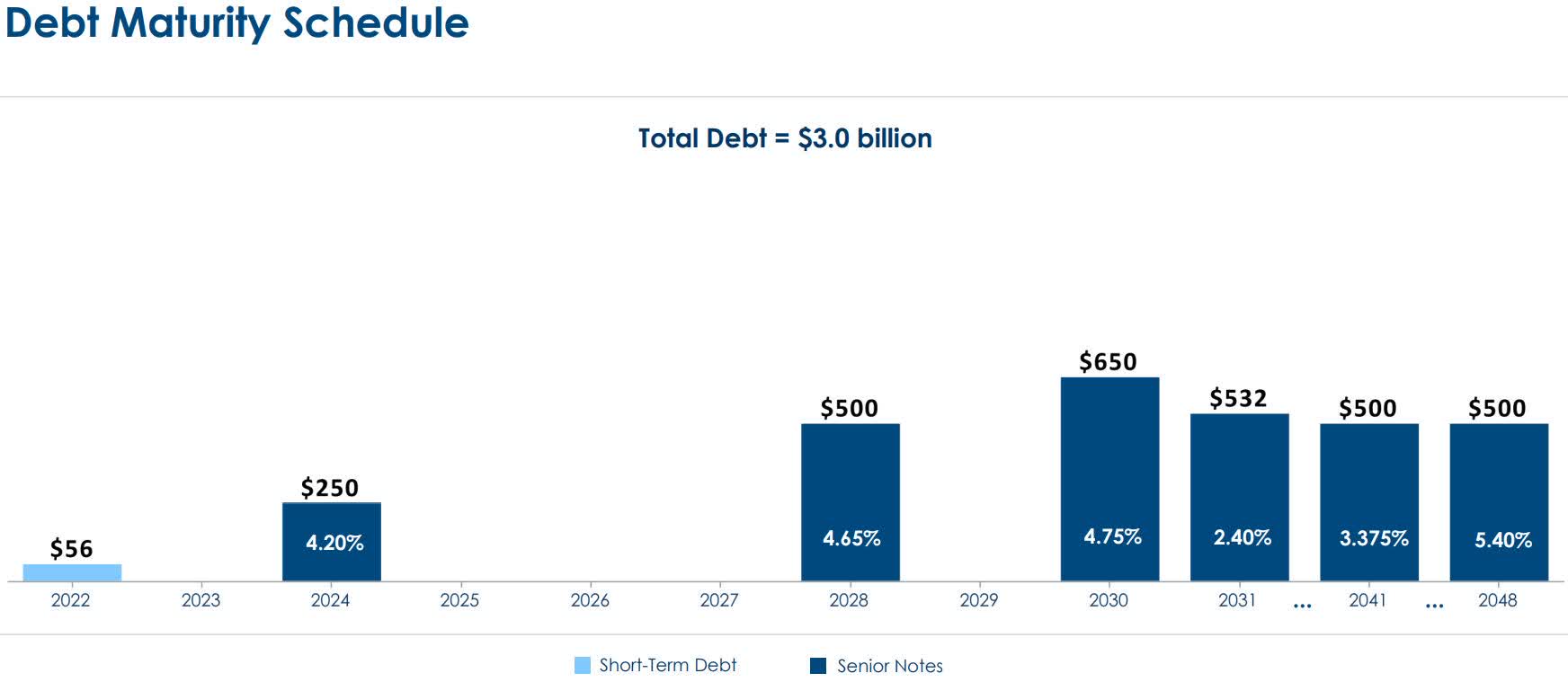

Total debt at the end of the reporting period was $3 billion. It has $56 million in short-term debt, with another $250 million due in 2024. After that, another $500 million is due in 2028. From there the remainder due is spread out from 2030 to 2048.

Investor Presentation

Performance by segment

In the first nine months of calendar 2022 all the segments of IPG grew organically, although all three segments showed signs of slowing down in the third quarter.

Investor Presentation

Media, Data Engagement Solutions

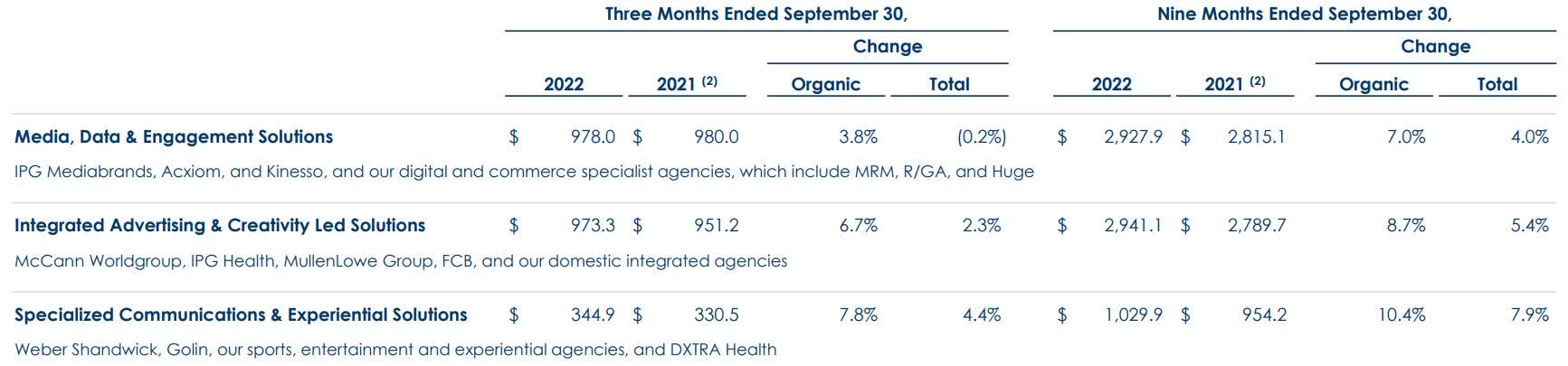

In its Media, Data Engagement Solutions generated revenue of $2.9 billion in the first nine months of 2022, compared to $2.8 billion in the first nine months of 2021. That was up 7 percent organically, and 4 percent overall.

In the third quarter of 2022 Media, Data Engagement Solutions generated revenue of $978 million, compared to $980 million in the third quarter of 2021, down (0.2) percent overall, and up organically 3.8 percent.

Integrated Advertising & Creativity Led Solutions

Revenue from its Integrated Advertising & Creativity Led Solutions segment was $973.3 million in the third quarter of 2022, up 6.3 percent organically, and up 2.3 percent total, compared to $951.2 million in the third quarter of 2021.

For the first nine months of calendar 2022 the segment generated revenue of $2.941 billion, up 8.7 percent organically and up 5.4 percent total, compared to $2.789 billion in the first nine months of 2021.

Specialized Communications & Experiential Solutions

Revenue in the third quarter of 2022 from its Specialized Communications & Experiential Solutions segment was $344.9 million, up 7.8 percent organically and 4.4 percent total.

In the first nine months of 2022 revenue generated from the segment was $954.2 million, up 10.4 percent organically and 7.9 percent total.

The most important takeaway here is third quarter results revealed that growth momentum was slowing down heading into the fourth quarter, and based upon macro-economic conditions, lack of visibility, and tightening up of spend by upper management, it’s highly probable that the numbers are going to get worse over the next couple of quarters, and possibly longer if the global economy continues to get worse in the second half of 2023.

Spending decisions

Almost every company I’ve been researching lately has alluded to the fact companies are starting to reconsider spending decisions in light of the uncertainty associated with the slowing global economy and high interest rates that are having an impact on the top and bottom lines of companies. That is the same with IPG, which is facing more concern from its customer base.

Its clients, over the last several months or so have pointed to their concerns over how to best deploy capital under different scenarios if the recession gets worse for longer.

While most of its clients, at the time of the last earnings call were asking for the input on making contingency plans and how to prioritize spending under difficult economic conditions, a smaller number were already deferring some of their spending. I think there’s probably going to be a lot more companies delaying spend on some projects until things get clearer concerning the economy.

I generally agree with management’s assertion that those companies that continue to invest during down cycles can, under normal downturns, come out ahead by gaining market share and growing at a faster pace than their peers.

But this doesn’t appear to be normal circumstances, which is why so many companies are tightening up spend and pushing spending decisions farther up the corporate hierarchy.

I think this is why investors can’t rely on historical patterns connected to downturns to base their decisions on concerning IPG. We really have no idea how 2023 is going to turn out economically, and the general consensus the first half will be tough and the second half will rebound, while probable, can’t be guaranteed.

There’s strong possibility the recession will extend toward the end of 2023 and possibly into 2024. The is, many business leaders that make spending decisions are seeing this as a period of very low visibility that is less clear than recent economic slowdowns, and are making decisions in accordance with that.

Conclusion

I think the key metric for IPG will be the economic sentiment surround spending decisions by top management teams. The fact that a lot of spending decisions have already been booted up the management hierarchy means there is a lot of concern over the economic conditions in the quarters ahead because there is no clarity as to the depth of the recession, or its duration.

My thought is too many companies are treating this like just another economic downturn, when interest rates are soaring, the U.S. debt stands at over $31 trillion, and consumers are prioritizing their own spending because of a job market that is now showing a lot of people being let go because of slowdowns across a number of sector.

Under normal economic slowdowns, sales and marketing spend tends to rebound fairly quickly, again, it remains to be seen if this is a normal economic slowdown, or something worse. That’s the issue facing many decision makers in regard how much to spend under these conditions. With that in mind, I think spending is going to cut more than IPG may be thinking at this time, and that should put downward pressure on its share price if that’s how it plays out. If conditions worsen, it’s going to drop further.

On the other hand, if this ends up being an economic similar to most in the past, the company will still take a hit on lower revenue, but would probably rebound quickly once signs of a turnaround are confirmed.

Either way, in the short term, the stock is going to probably correct, but further out it’s positioned for further growth once economic conditions improve.

My final thought is the company has gotten ahead of itself and is due for a correction. Once that happens, I think it’ll trade level until there is more visibility on how its customers respond to the global economy.

Be the first to comment