dmitriymoroz/iStock via Getty Images

Since our Double Down report, International Paper (NYSE:IP) is up by more than 13% (including the dividend payment). Here at the Lab, during 2022, we were pretty cautious about the company’s development, and we initiated with a neutral target supported by a full analysis of IP’s Russian Exposure. Over the year, despite some disappointing results, we decided to increase the company to overweight with a thesis backed by: 1) a strong demand based on Fastmarkets RISI estimates, 2) higher price increases, 3) a solid balance sheet, and 4) a compelling valuation with a tasty dividend yield as a margin of safety (one of Mare Evidence Lab’s key supporting metric). Today, we are happy to report that IP is up by almost 10% thanks to a good quarter as well as positive indications reported below in Fig 2.

Mare Evidence Lab’s previous publication Resiliency of IP

Fig 2

Q4 Analysis

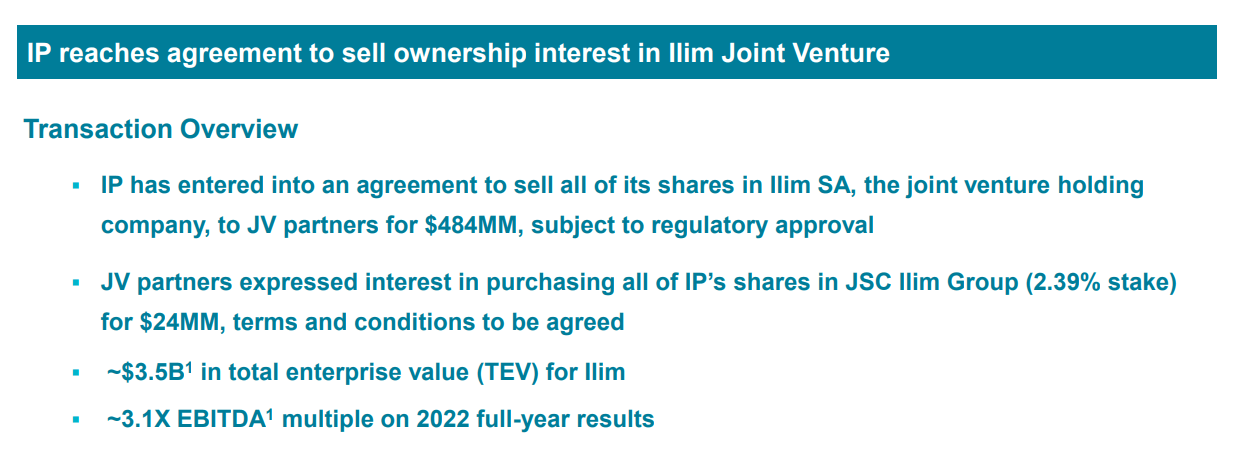

Before commenting on the company’s quarterly results, it is important to report that IP sold its Russian activities for $484m equity value. ILIM transaction was concluded for a total EV of approximately $3.5 billion based on a multiple on a 2022 EBITDA multiple of 3x. As a reminder, International Paper had a 50% equity stake, and all in all, IP disinvestment is still subject to regulatory considerations. Looking at the numbers, the company recorded a negative one-off charge of $533 million which was fully booked in Q4. Here at the Lab, from Q4 and FY onwards, ILIM IP will be accounted as discontinued operations and we restated IP’s historical accounts.

IP – ILIM transaction

Looking at the specific division, IP delivered the following:

-

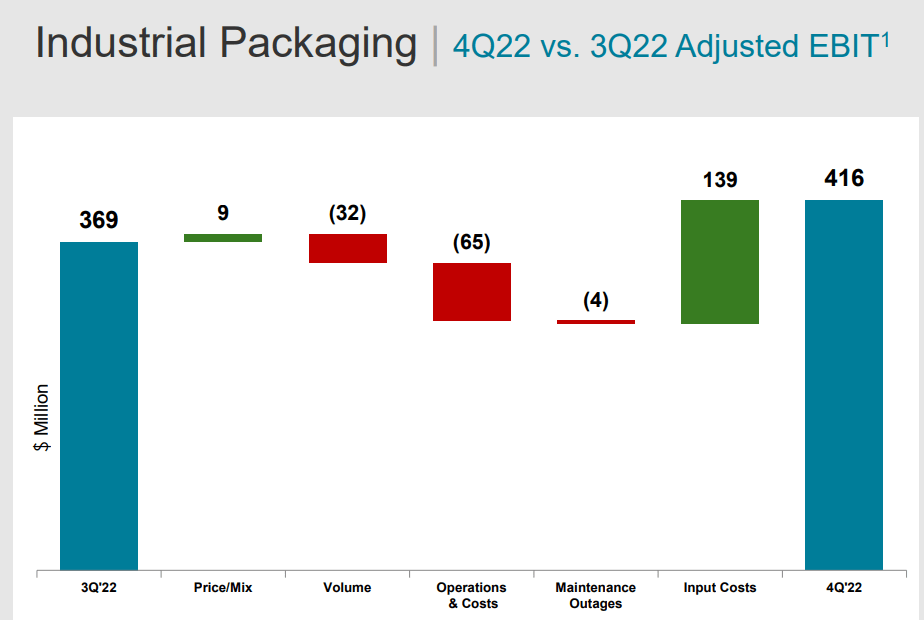

Industrial Packaging’s Q4 operating profit was flat compared to Q4 2021 and was considerably above Wall Street consensus estimates of $323 million. International Paper’s outlook was guiding a quarter erosion but the company delivered an operating profit increase of $47 million. This was driven by cost improvement that partially offset lower volumes (-$32 million) and maintenance costs (-$4 million). The company was still heavily impacted by higher energy and fiber cost; however, the company is still relying on price realization from previous top-line sales increases. Volumes on domestic box shipments decreased by 6.2% on a yearly basis (Fig 3);

-

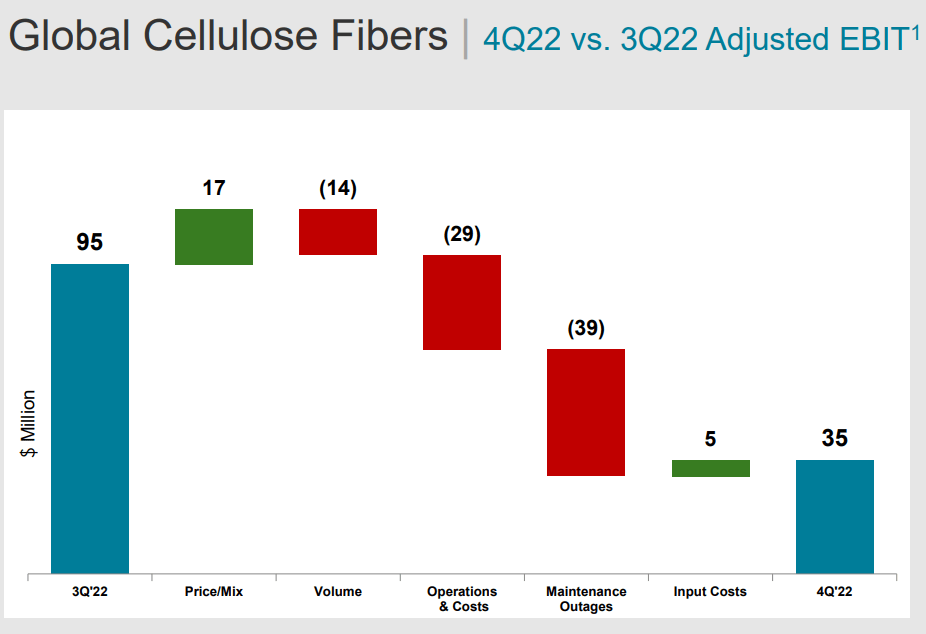

Global Cellulose Fiber’s performance was a positive contributor year on year; however, on a quarterly basis, EBIT was down by $60 million. The segment operating profit reached $35 million and the contraction was due to lower volumes and higher maintenance costs, respectively, at -$14 million and -$39 million. On a positive note, as recorded in the Packaging division, there was a positive price contribution of $17 million (Fig 4).

Industrial Packaging adj. EBIT evolution

Fig 3

Global Cellulose Fibers adj. EBIT evolution

Fig 4

Conclusion and Valuation

The company’s outlook confirmed a Fiscal Year 2023 EBITDA of $2.8 billion (versus the FY 2022 of $2.9 billion), 12% higher than equity research analyst average consensus and more in line with our internal estimates. We are guiding CAPEX at the guidance midpoint of $1.1 billion and a free cash flow range of $1 billion. As a reminder, Mare Evidence Lab’s target price is derived by the average between:

- An 8.0x EV/EBITDA on our 12-month forward estimates,

- A DCF analysis in which we assume a 10% cost of equity and a terminal growth rate of 2%, considering a risk-free rate of 3.5% and a debt cost of 4.5%.

Last time, given ILIM estimates, we lowered our target price and today we confirmed our buy rating at $50 per share. The company’s main risks are 1) a North American box demand slowdown, 2) supply constraints, 3) energy costs, and 4) higher competition.

Be the first to comment