Dilok Klaisataporn

A Quick Take On Intellicheck

Intellicheck, Inc. (NASDAQ:IDN) reported its Q3 2022 financial results on November 14, 2022, missing revenue but beating EPS estimates.

The firm provides organizations with identification verification and threat intelligence solutions.

IDN is making a transition toward more SaaS (Software as a Service) revenue, but that can take an extended amount of time.

I’m on Hold for IDN for the near term as revenue sags.

Intellicheck Overview

Melville, New York-based Intellicheck, Inc. was founded in 1994 and provides a suite of identity authentication and threat identification solutions for financial institutions, retailers, law enforcement and other customers primarily in the United States.

The firm is headed by Chief Executive Officer Bryan Lewis, who has been with the firm since 2018 and previously was Chief Operating Officer at Third Bridge Group Limited and Managing Director at BondDesk Group.

The company’s primary offerings include:

-

Intellicheck Platform

-

IDN-Portal

-

IDN-Portal+

-

APIs – Direct

-

SDKs.

IDN acquires customers primarily through its in-house direct sales and marketing efforts. It also has developed relationships with resellers in selected verticals.

Intellicheck’s Market & Competition

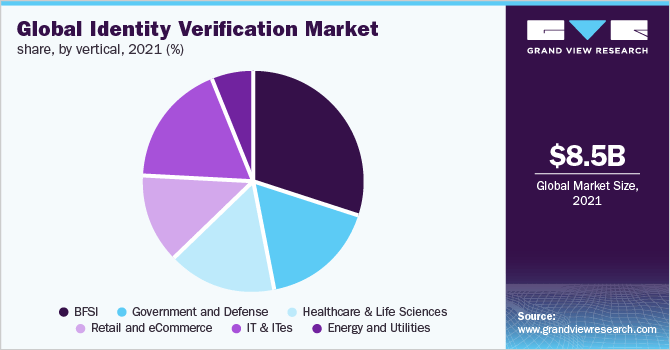

According to a 2022 market research report by Grand View Research, the global market for identity verification was an estimated $8.5 billion in 2021 and is forecast to reach $34 billion by 2030.

This represents a forecast CAGR of 16.7% from 2022 to 2030.

The main drivers for this expected growth are the growing incidence of identity fraud and the increased need for data security across more company and governmental touchpoints.

Also, increasing government regulations, specifically in the financial sector, will provide greater opportunities for market participants.

Below is a chart showing the global identity verification market by vertical:

Global Identify Verification Market (Grand View Research)

Major competitive or other industry participants include:

-

ID.me

-

Acuant

-

Mitek Systems

-

Nuance Communications

-

IDEMIA

-

Thales Group

-

GB Group Plc

-

Others.

Intellicheck’s Recent Financial Performance

-

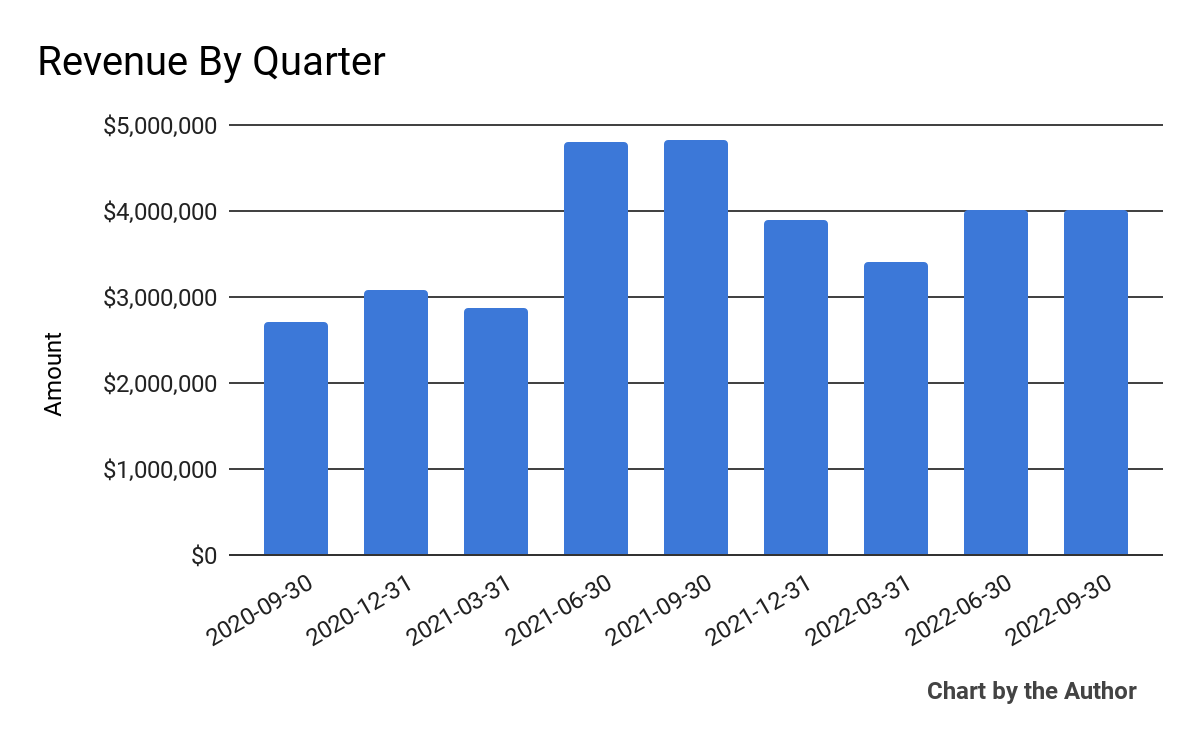

Total revenue by quarter has fallen in recent quarters:

9 Quarter Total Revenue (Financial Modeling Prep)

-

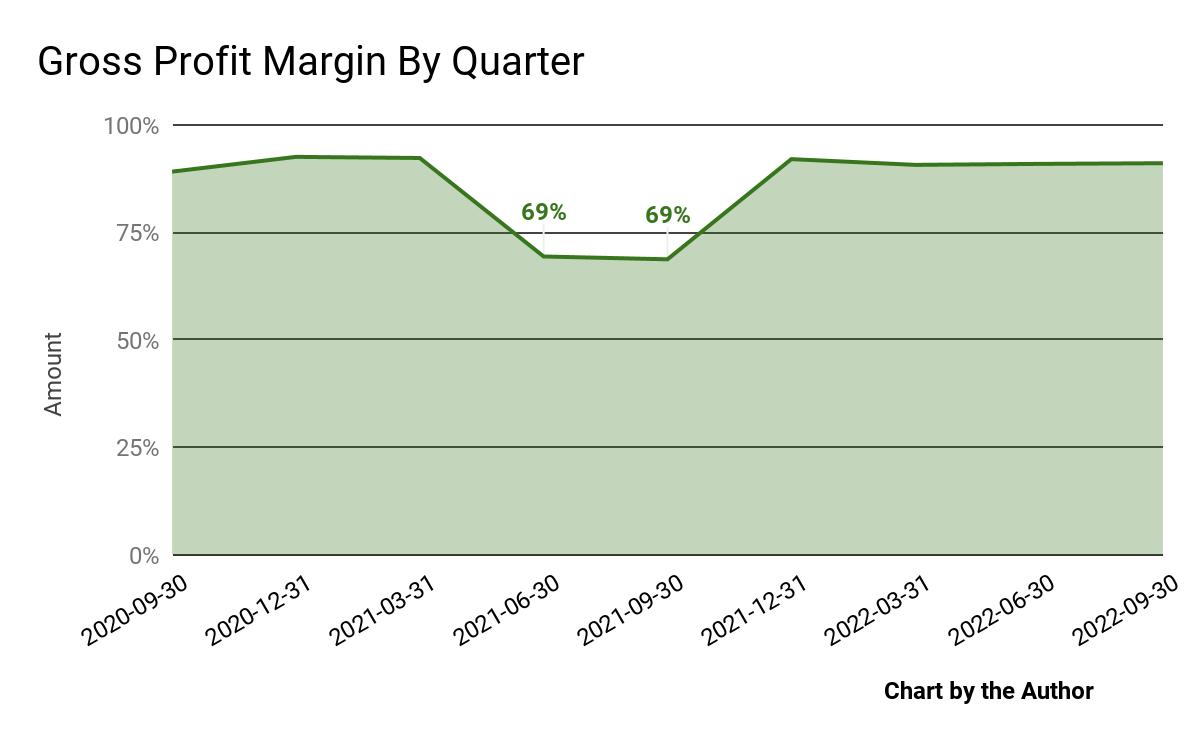

Gross profit margin by quarter dipped in 2021 but has since rebounded:

9 Quarter Gross Profit Margin (Financial Modeling Prep)

-

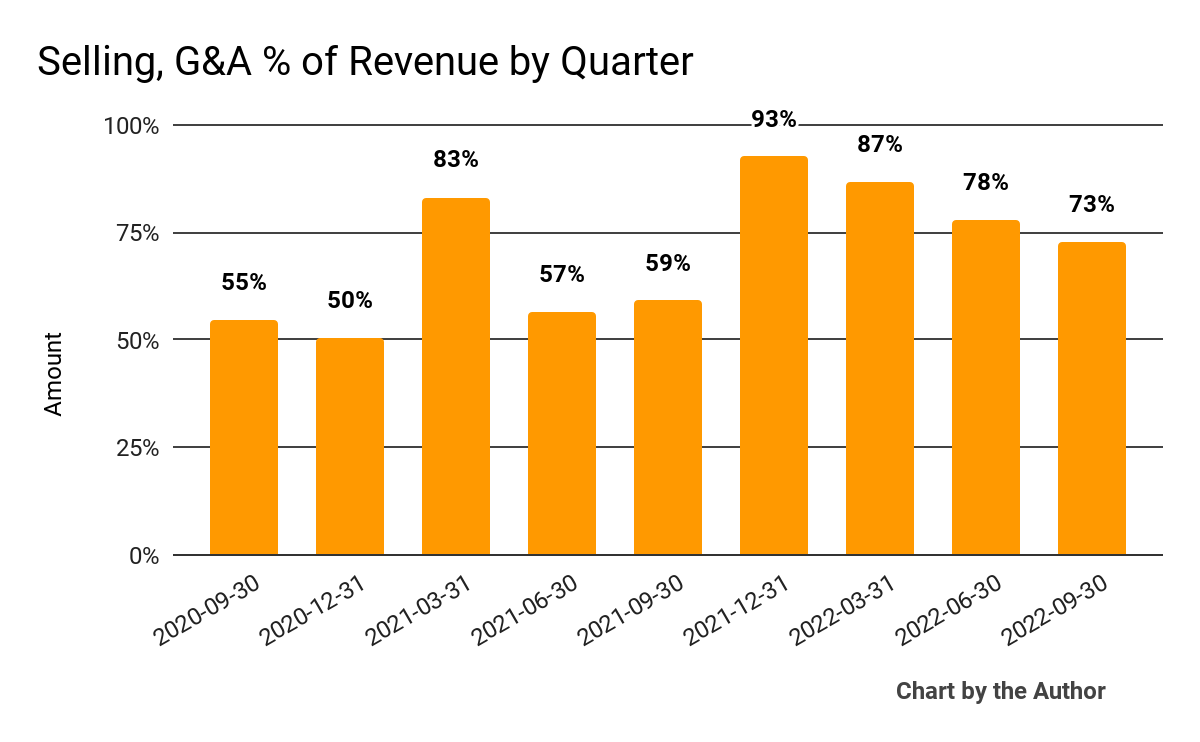

Selling, G&A expenses as a percentage of total revenue by quarter have been dropping recently, although they are still high:

9 Quarter Selling, G&A % Of Revenue (Financial Modeling Prep)

-

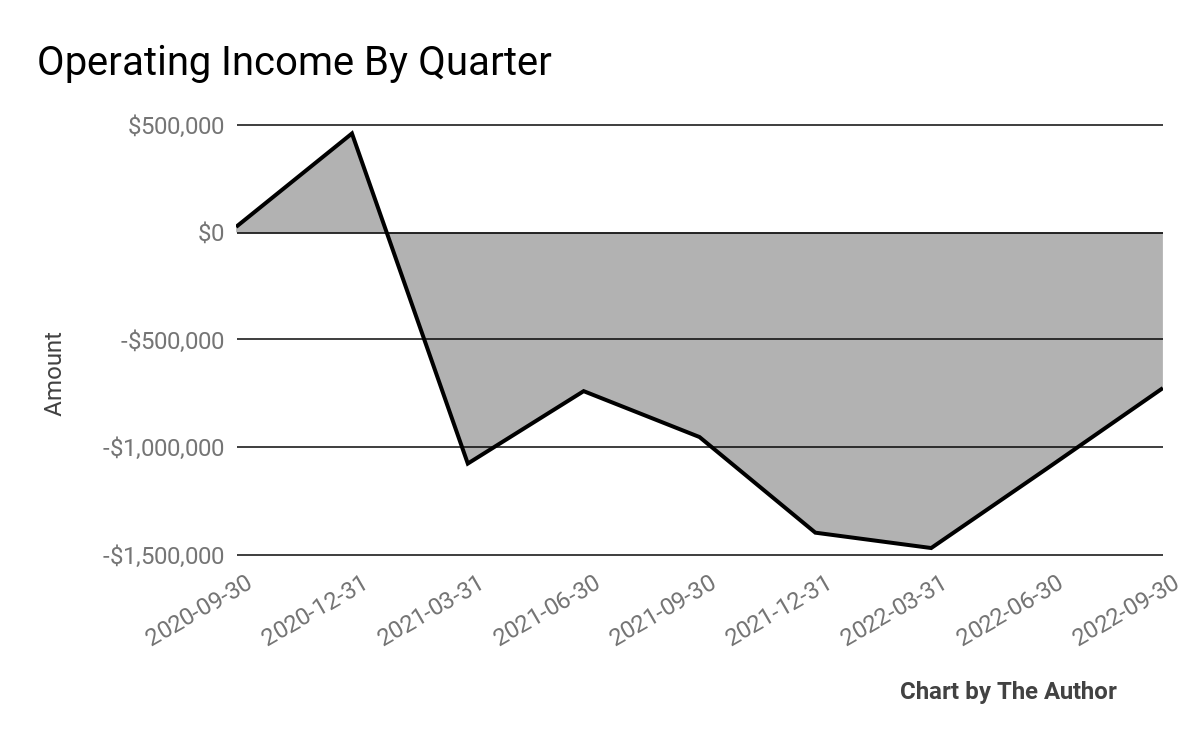

Operating losses by quarter have been more substantial in recent quarters:

9 Quarter Operating Income (Financial Modeling Prep)

-

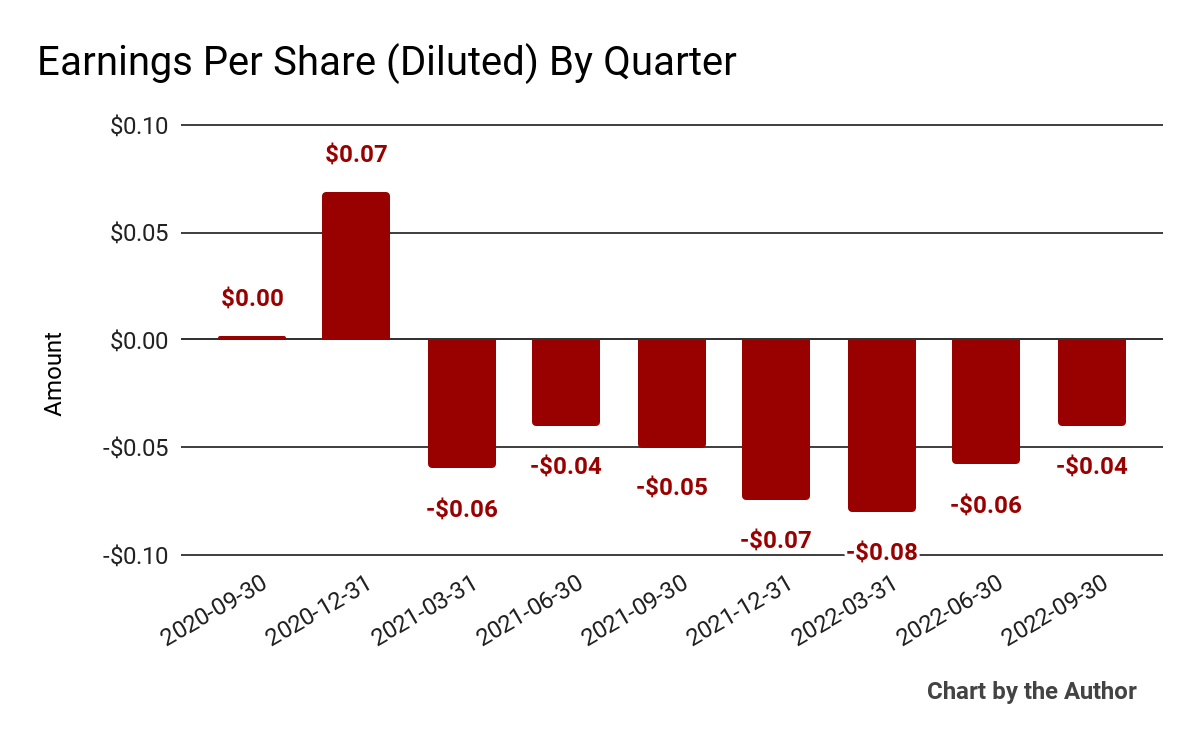

Earnings per share (Diluted) have remained negative for each of the last seven quarters:

9 Quarter Earnings Per Share (Financial Modeling Prep)

(All data in the above charts is GAAP.)

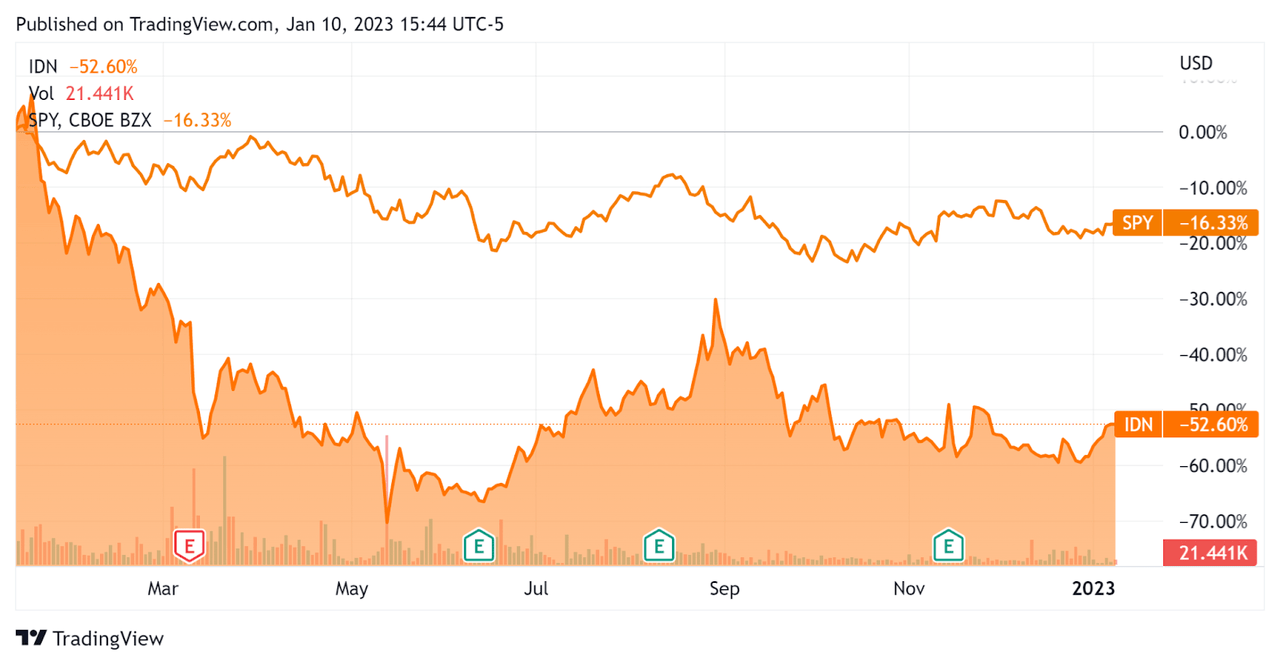

In the past 12 months, IDN’s stock price has fallen 52.6% vs. the U.S. S&P 500 Index’s (SP500) drop of around 16.3%, as the chart below indicates:

52-Week Stock Price Comparison (Seeking Alpha)

Valuation And Other Metrics For Intellicheck

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

2.0 |

|

Enterprise Value / EBITDA |

-7.1 |

|

Revenue Growth Rate |

-1.6% |

|

Net Income Margin |

-30.6% |

|

GAAP EBITDA % |

-28.9% |

|

Market Capitalization |

$43,209,720 |

|

Enterprise Value |

$31,361,291 |

|

Operating Cash Flow |

-$1,002,331 |

|

Earnings Per Share (Fully Diluted) |

-$0.25 |

(Source – Financial Modeling Prep.)

Commentary On Intellicheck

In its last earnings call (Source – Seeking Alpha), covering Q3 2022’s results, management highlighted the 22% year-over-year growth in SaaS service revenue.

Additionally, leadership quashed the “concern” that some had that the company would need to raise capital to fund its operations.

CEO Lewis indicated that the company will spend for sales & marketing efforts but that “those increases should create increased growth.”

As to its financial results, total revenue dropped by 17% year-over-year despite the above-mentioned 22% rise in SaaS recurring revenue.

Gross profit margin remained high due to lower hardware sales, while operating expenses rose from high recruiting efforts and increased marketing and advertising expenses.

As a result, earnings per share remained negative for the seventh consecutive quarter.

For the balance sheet, the company ended the quarter with cash and equivalents of $11.8 million and no debt.

Over the trailing twelve months, free cash used was $1.5 million, of which capital expenditures accounted for $500,000. The company paid $2.2 million in stock-based compensation (“SBC”).

Management did not provide any forward guidance but said it was managing the P&L to breakeven.

Regarding valuation, the market is valuing IDN at an EV/Sales multiple of only 2.0x.

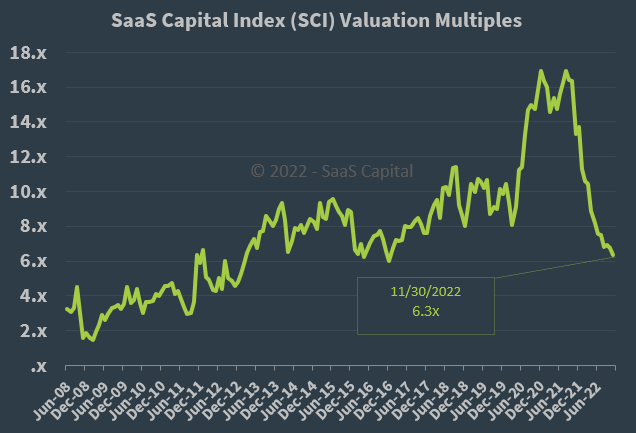

The SaaS Capital Index of publicly held SaaS software companies showed an average forward EV/Revenue multiple of around 6.3x on November 30, 2022, as the chart shows here:

SaaS Capital Index (SaaS Capital)

So, by comparison, although the company is not primarily a SaaS firm, IDN is currently valued by the market at a significant discount to the broader SaaS Capital Index, at least as of November 30, 2022.

Notably, IDN’s EV/Sales multiple [TTM] has dropped by 56% in the past twelve months, as the Seeking Alpha chart shows here:

Enterprise Value / Sales Multiple (Seeking Alpha)

The primary risk to the company’s outlook is an increasingly likely macroeconomic slowdown or recession, which may accelerate new customer discounting, produce slower sales cycles and reduce its revenue growth trajectory.

A potential upside catalyst to the stock could include an end to interest rate hikes and a reduction in the cost of capital that has pushed so many tech multiples down.

However, the other side of the coin is that revenue may continue to drop as we enter the slowdown or possible recession in 2023.

In any event, Intellicheck, Inc. is in a difficult spot, with already-dropping revenue as it seeks to transition to a SaaS company.

These transitions can take a significant amount of time and result in a lagging stock price while the company makes the turn toward more predictable revenues.

Until the transition is complete, I’m on Hold for Intellicheck, Inc.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment