wayfarerlife/iStock via Getty Images

Steel has numerous applications when it comes to the construction industry, as well as for other markets. One company dedicated to manufacturing and selling a niche portfolio of steel-oriented products is Insteel Industries (NYSE:IIIN). In recent years, the general trajectory for the company’s revenue has been positive. Although profits have been volatile, cash flows have been a little more consistent. They have also been generally positive over the years. This year, as management is able to pass the higher costs of its products through to its customers, the fundamental condition of the business has improved significantly. Near-term, if this continues, the end result could be further upside for shareholders. But even management is unsure of what the future holds and, because of that, there is some risk of a return to the kind of results we have seen in prior years. In that scenario, it’s difficult to call the company anything other than lofty. Because of that, investors should be wise to only consider buying this prospect if they see the current environment continuing for the foreseeable future. For anybody else, this might be one prospect to avoid for now.

A play on steel

According to the management team at Insteel Industries, the company operates as the largest manufacturer of steel wire reinforcing products for concrete construction applications in the US. The company produces and sells prestressed concrete strands, as well as welded wire reinforcement products. Under this latter category, you also have ESM, concrete pipe reinforcement, and welded wire reinforcement products. For the most part, these products are sold to producers of concrete products, with the end users ultimately working in the non-residential construction market.

To be more specific about the company’s offerings, it’s important to note that it’s prestressed concrete strand products our high strength, seven wire strands that are used to provide reinforcement for bridges, parking decks, buildings, and other concrete structures. Meanwhile, it’s welded wire reinforcement products are used for the reinforcement of concrete elements or structures, for the reinforcement of concrete pipes, box culverts, and precast manholes for drainage and sewage systems and other related functions, and for crack control applications in driveways, sidewalks, and other related uses. During the company’s 2021 fiscal year, 85% of its sales went to that end use, while the remaining 15% went to residential construction needs.

Author – SEC EDGAR Data

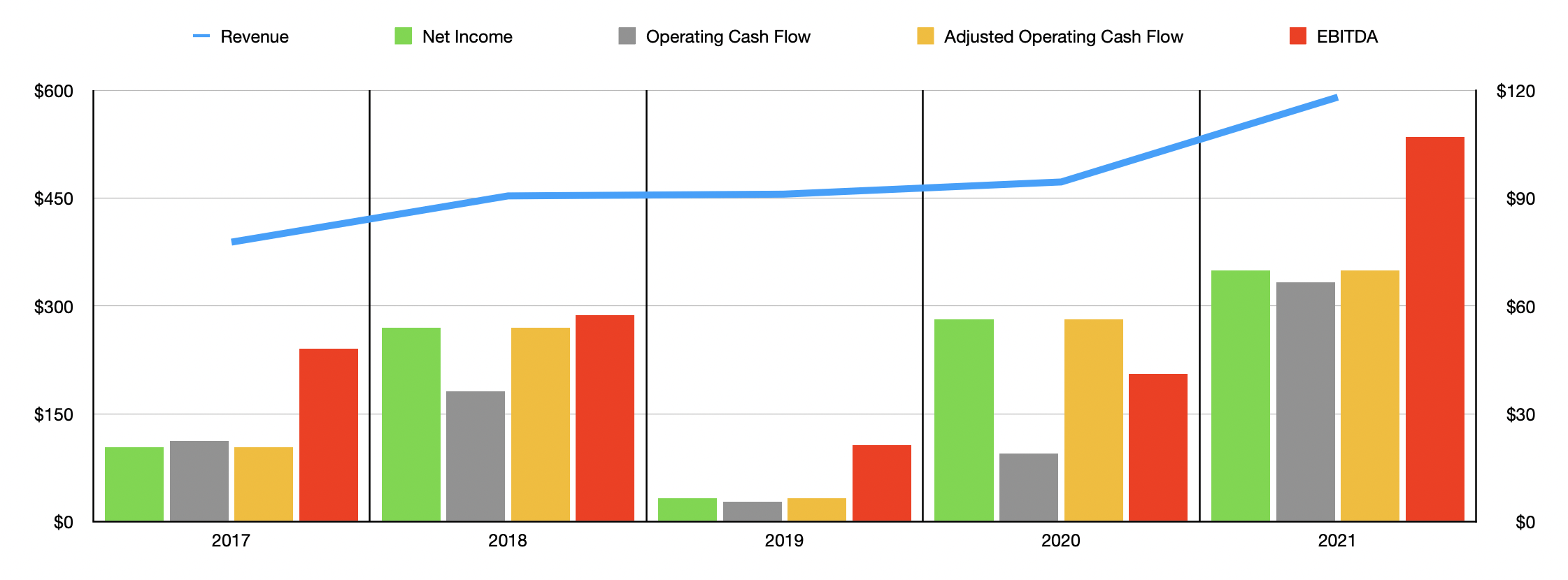

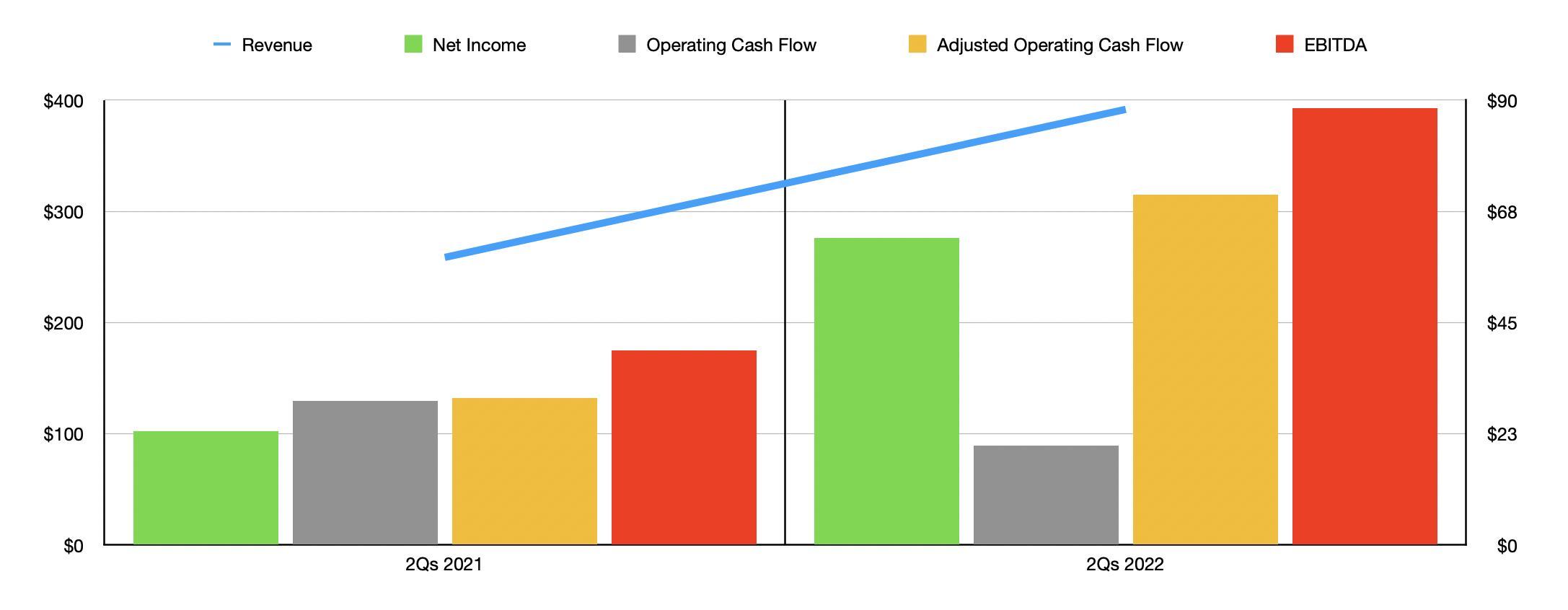

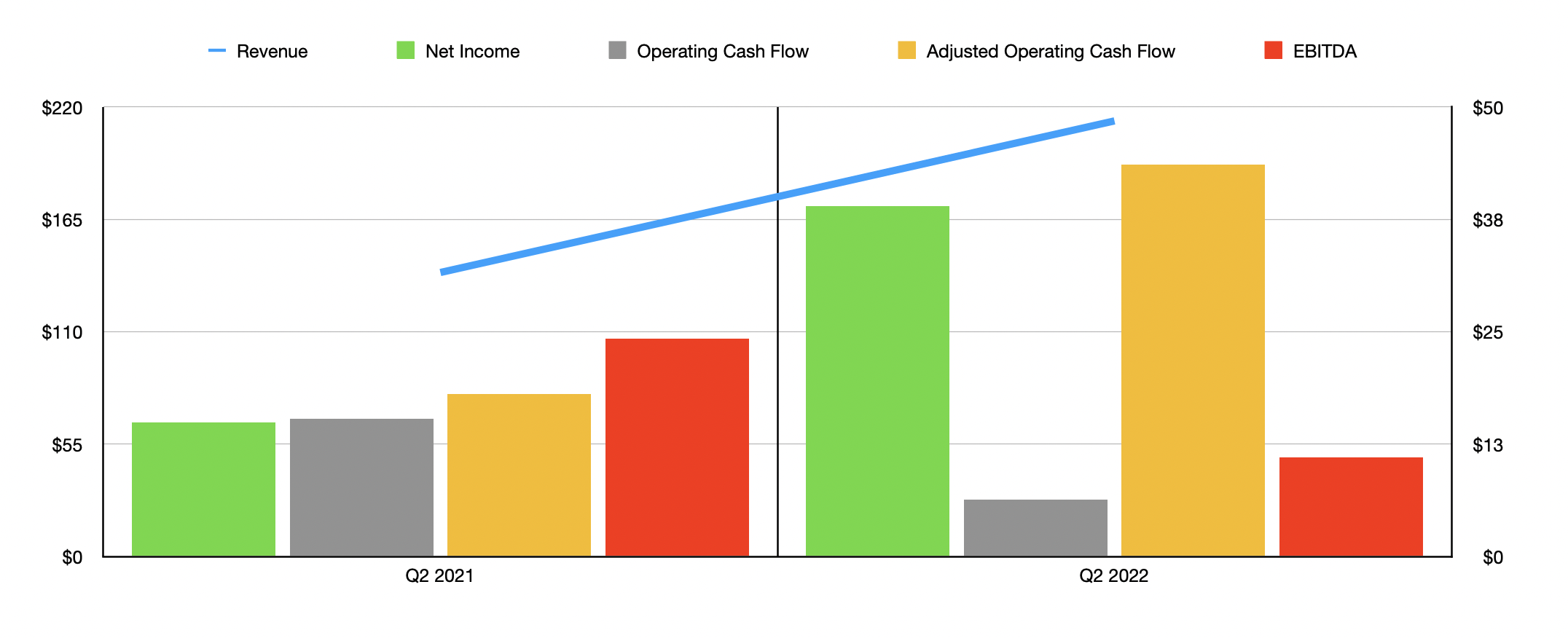

Over the past few years, fundamental performance achieved by Insteel Industries was rather impressive. Between 2017 and 2021, for instance, sales of the business expanded from $388.9 million to $590.6 million. The rise between 2020 and 2021 alone was 25%. The good news for investors is that the recent inflationary environment has supercharged results. In the first two quarters of the company’s 2022 fiscal year, sales came in at $391.7 million. That’s up for the $258.6 million reported one year earlier. Growth was particularly strong in the second quarter of the company’s 2022 fiscal year, the quarter for which data was just released. Sales for that timeframe totaled $213.2 million. That implies a year-over-year increase of 53.4% over the $139 million reported the same quarter last year. Sales for the quarter beat what analysts were anticipating by nearly $35.9 million. All of this increase and more was driven by a 65.4% rise in the average selling prices of its products. This was offset some, unfortunately, by a 7.2% decrease in product shipments.

Author – SEC EDGAR Data

On the bottom line, things for the company have generally been volatile over the years. Between 2017 and 2021, for instance, net profits have ranged from a low point of $5.6 million to a high point of $66.1 million, with no real trend visible from year to year. The high point was what the company reported for its 2021 fiscal year. Cash flow has been volatile as well, but at least the general trend for it has been obvious. Between 2017 and 2021, operating cash flow for the business expanded from $20.8 million to $69.9 million. If we adjust for changes in working capital, it would have risen from $38.3 million to $83.1 million. A similar trend can be seen when looking at EBITDA, with that metric rising from $48.2 million in 2017 to $107.1 million last year. Just like operating cash flow and adjusted operating cash flow, however, the company did hit a trough in 2019.

Author – SEC EDGAR Data

One good thing for investors is that management has done exceedingly well in transferring the increased costs it’s incurring as a result of the inflationary environment to its customers. Net income in the first half of this year, for instance, came in at $62.1 million. That’s nearly triple the $23.1 million received one year earlier. The strongest growth came in the second quarter of the year, with net profits of $39 million dwarfing the $14.9 million reported one year earlier. On a per-share basis, the company reported profits of $1.99. This was far higher than the $0.76 in profits achieved one year earlier and it beat analysts’ expectations of $1.12 per share.

Another way to measure profitability is to use cash flow. Operating cash flow at the company did decrease year over year in the latest quarter, dropping from $15.3 million down to $6.3 million. But if we adjust for changes in working capital, it would have risen from $18.1 million to $43.6 million. For the year-to-date timeframe, the decline in cash flow was from $29.2 million to $20.1 million, while the adjusted equivalent rose from $29.7 million to $70.8 million. The only area in which the company truly suffered was when it came to EBITDA. This declined from $24.2 million to $11 million for the latest quarter relative to the same time last year. But even so, for the year-to-date timeframe, this metric grew from $39.4 million to $88.4 million.

When it comes to the rest of the company’s 2022 fiscal year, management said that they expect performance to continue to be robust. Having said that, the business is expressing concerns surrounding inadequate supplies of domestically produced wire prod. To address this, the business did supplement their requirements with offshore material in order to bridge that gap. As such, the company expects to be fine throughout the rest of the fiscal year. However, they are also worried about the impact of record-high steel prices moving forward, even though demand remains robust.

Author – SEC EDGAR Data

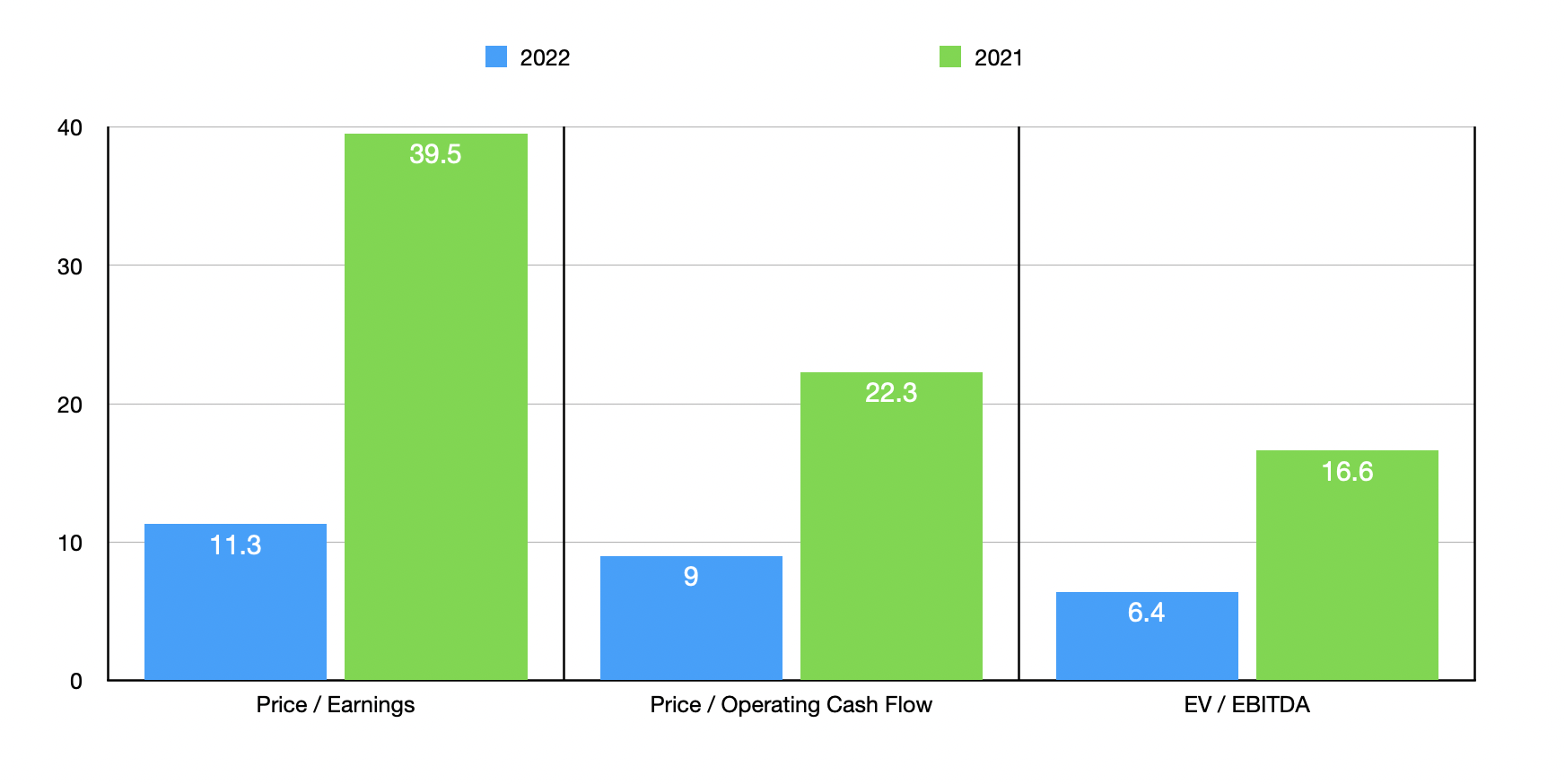

Given the likelihood that this current environment will not stay this way forever, and because we don’t have guidance for management covering the rest of the year, I do not think it would be a wise decision to forecast what financial performance might be for the rest of 2022 and to base the company’s valuation on that. Instead, I decided to price the company using both its 2020 and 2021 results. During this, we can see stark contrast depending on whether we think results achieved in 2021 represent the new normal or if fundamental performance will ultimately make shares rather pricey. Using our 2020 results, for instance, the business is trading at a rather high multiple of 39.5 if we use the price to earnings approach. This plunges to just 11.3 if we use the 2021 figures. The price to adjusted operating cash flow multiple of the company would drop from 22.3 to just 9, while the EV to EBITDA multiple would decline from 16.6 to 6.4. Giving the company the benefit of the doubt, I then decided to compare it to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 4.7 to a high of 435.7. Using the price to operating cash flow approach, the range was from 6.1 to 12. And using the EV to EBITDA approach, the range was from 4.1 to 19.9. In all three cases, three of the five companies were cheaper than Insteel Industries.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Insteel Industries | 11.3 | 9.0 | 6.4 |

| Builders FirstSource (BLDR) | 7.3 | 7.3 | 4.9 |

| Cornerstone Building Brands (CNR) | 4.7 | 8.1 | 4.1 |

| Tecnoglass (TGLS) | 16.6 | 9.6 | 10.3 |

| Apogee Enterprises (APOG) | 435.7 | 12.0 | 19.9 |

| Owens Corning (OC) | 9.2 | 6.1 | 5.6 |

Takeaway

Given current market conditions, Insteel Industries looks like a robust and rapidly growing enterprise. Having said that, I do worry about the long-term outlook for the market because I do not think that current price inflation will hold in perpetuity. If I am wrong, shares will make for an attractive opportunity for investors to buy into. Having said that, I worry about fundamentals eventually pulling back to what we saw in prior years. In that case, shares would look rather lofty. Even if that is the case, while the company may not make for a great investment prospect in that condition, it is a quality operator with a history of consistent expansion. So I don’t see some doomsday scenario significantly impacting the firm. Because of this, at the end of the day, I feel that a ‘hold’ rating is most appropriate. But investors who do buy into the company should keep a careful eye on what goes on with this market. Because the situation could change rapidly for the better or worse.

Be the first to comment