S&P 500 AND NASDAQ 100 OUTLOOK: SLIGHTLY BEARISH

- The S&P 500 and Nasdaq 100 finished the week lower after the Federal Reserve indicated that its terminal rate will be higher than previously expected

- Inflation will be the most important price action catalyst next week

- For market sentiment to improve, CPI data must show a meaningful slowdown in price pressures

Recommended by Diego Colman

Get Your Free Equities Forecast

Most Read: USD Snaps Back on NFP After Fed-Fueled Rally: EUR/USD, GBP/USD

The S&P 500 and Nasdaq 100 suffered steep losses this week after the Federal Reserve delivered another 75 basis-point hike at its November meeting. However, this decision, which was fully discounted, was not the main bearish catalyst: verbal guidance was. While the central bank signaled that it may downshift the pace of tightening at some point in the future, it also acknowledged that it is too premature to talk about a “pause” and that the ultimate level of interest rates will be higher than expected due to persistently elevated inflation.

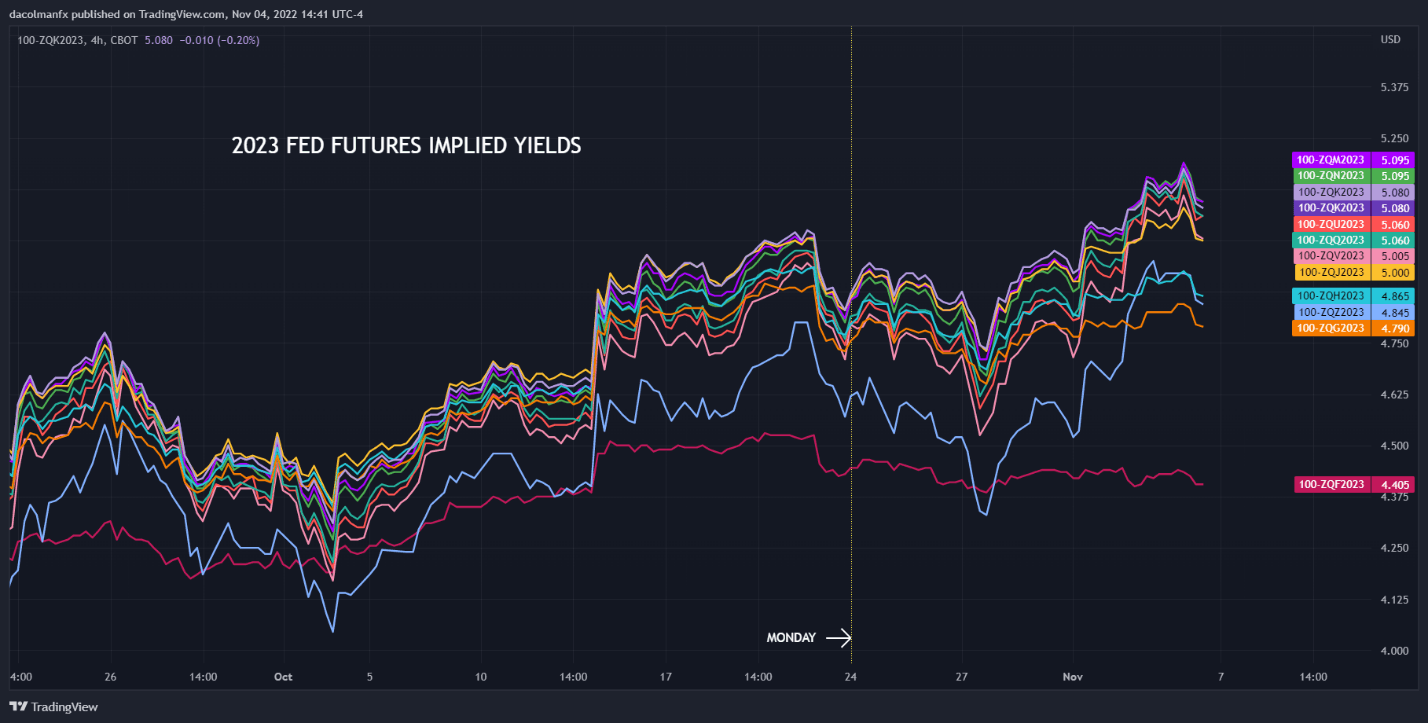

Powell’s hawkish message spooked traders, leading them to reprice higher the path of monetary policy, as reflected in the chart below, showing an implied terminal rate on Fed funds futures of around 5.1% by the middle of next year, up from 4.85% on Monday. This aggressive roadmap is likely to reinforce recession risks and undermine equities, even if the FOMC moves to a slower cycle to better assess the cumulative effects of its past actions considering the lag of policy transmission.

IMPLIED YIELD FOR 2023 FED FUTURES

{kind=link}

Source: TradingView

The latest U.S. employment report confirmed that policymakers have more work to do to cool the economy in their quest to tame inflation via demand destruction. In October, U.S. employers added 261,000 payrolls versus 200,000 expected, a sign that hiring remains extremely resilient despite numerous headwinds. A tight labor market should bolster household spending while preventing wage pressures from easing materially, a scenario that will complicate the fight to restore price stability.

In any case, we’ll know more about inflation next week, after the U.S. Bureau of Labor Statistics releases last month’s data on Thursday morning. That said, headline CPI is forecast to have risen 0.7% on a seasonally adjusted basis, with the annual rate seen easing to 8.0% from 8.2% in September. For its part, the core gauge is expected to clock in at 0.4% m-o-m and 6.5% y-o-y.

For the mood to improve and for buyers to return, the CPI outturn must surprise to the downside in a material way. Results that are in-line with or above estimates should keep sentiment depressed, paving the way for more losses for both the S&P 500 and Nasdaq 100. In this sense, the very near-term outlook for stocks hinges on the inflation report, but over a medium-term horizon, the underlying bias is still negative.

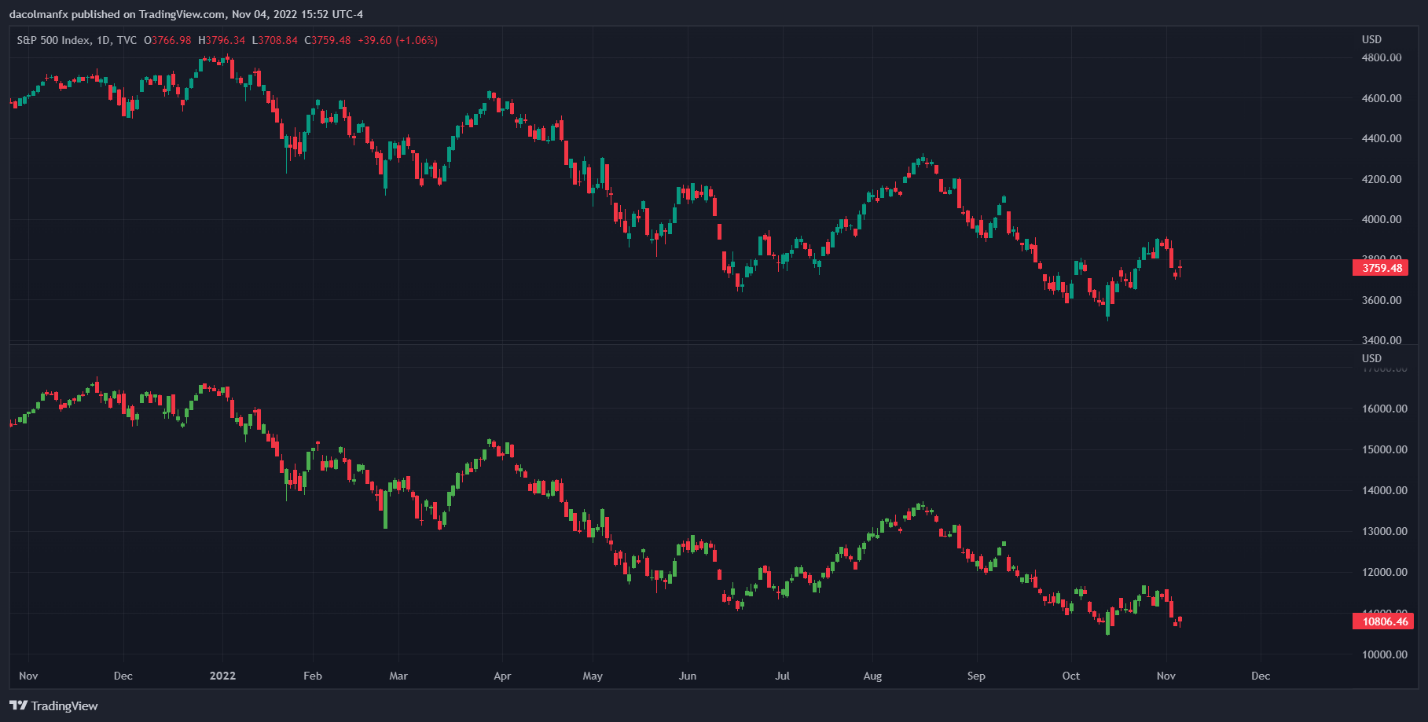

S&P 500 and Nasdaq 100 Daily Chart

S&P 500 Chart Prepared Using TradingView

Trade Smarter – Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team

Subscribe to Newsletter

EDUCATION TOOLS FOR TRADERS

- Are you just getting started? Download the beginners’ guide for FX traders

- Would you like to know more about your trading personality? Take the DailyFX quiz and find out

- IG’s client positioning data provides valuable information on market sentiment. Get your free guide on how to use this powerful trading indicator here.

—Written by Diego Colman, Market Strategist for DailyFX

Be the first to comment