Olena Lishchyshyna/iStock via Getty Images

Over the last several years, Infinera Corporation (NASDAQ:INFN), which provides optical transport networking equipment, software, and services around the world, has struggled to sustainably break out, always seeming to represent a lot of potential but never being able to quite reach it.

It if is able to execute its current strategy it could be on the verge of breaking out to the upside if it’s able to continue to gain market share with ICE6, and successfully introduce its 100-gig point to multi-point pluggables, which management believes will open up a multibillion-dollar addressable market for the company.

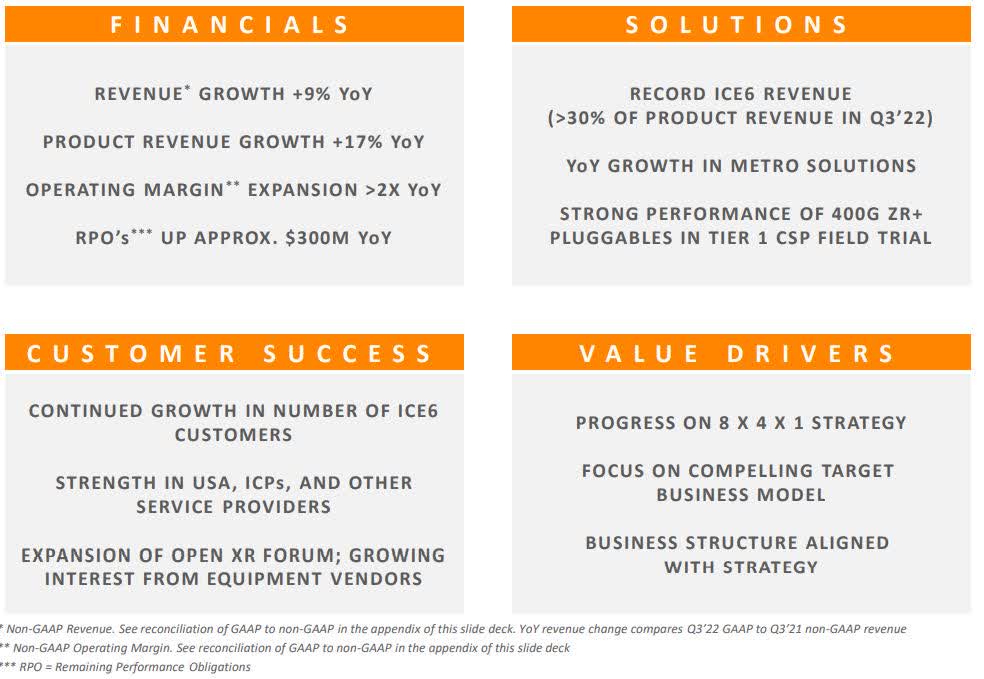

At the same time, it’ll have to continue to perform well with its mix of vertically integrated products, which account for almost 50 percent of product sales. ICE6 represented about 30 percent of product sales in the third quarter, and for full-year 2022 is projected to account for about 20 percent to 25 percent of total product sales.

In this article we’ll look at the third-quarter performance of INFN, the short-term headwinds it faces, and how its share price could finally, sustainably break through to the upper side once the economy rebounds.

Third quarter performance

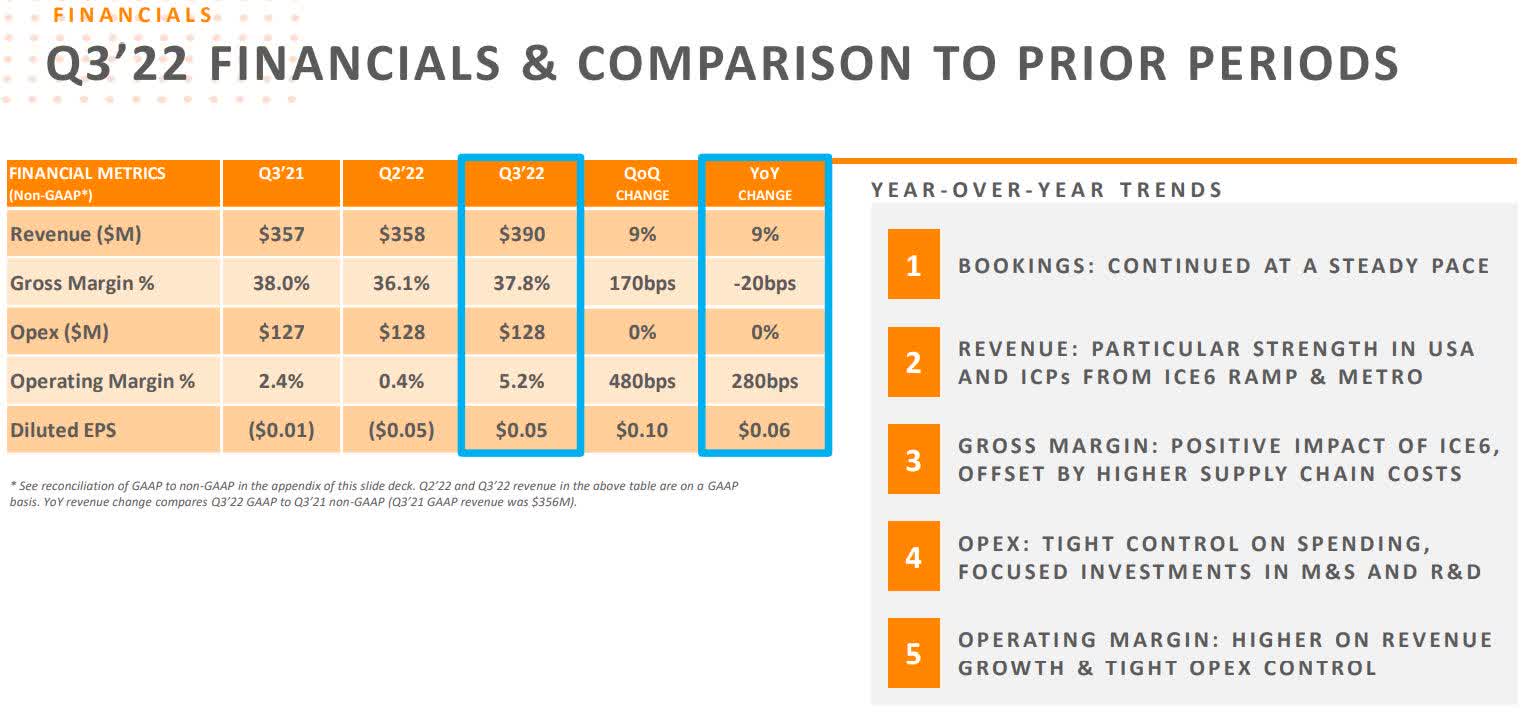

Revenue in the third quarter of 2022 was $390 million, up 9.7 percent from the $356 million in revenue generated in the third quarter of 2021. Revenue for the first nine months of 2022 was $1.087 billion compared to $1.024 billion in the first nine months of 2021.

Investor Presentation

Product revenue in the reporting period was $317 million, an increase of approximately $37 million from the $270.8 million in product revenue in the third quarter of 2021.

Service revenue was $73 million, down almost $12 million from the $85 million in service revenue generated in the third quarter of 2021. While service revenue was stable on a quarter-to-quarter basis, it remained down year-over-year because of its customers delaying deployment of capital in early 2022, which resulted in its backlog shrinking in services.

Including the company’s outlook for the fourth quarter, it expects revenue growth of about 10 percent year-over-year. Taking into account the company will likely have to absorb over $50 million in elevated supply chain costs for 2022, it points to an overall good performance.

Investor Presentation

A major question heading into 2023 is how much supply chain constraints will continue to weigh on the performance of INFN going forward. Another area affected by supply chain issues was gross margin, which was 37.8 percent in the third quarter, up 170 basis points sequentially. The company had to absorb about 400 basis points of headwinds associated to supply chain in the reporting period.

Operating expenses in the third quarter of 2022 were $127.5 million, with an operating profit of $20 million and EPS of $0.05 per share. On a GAAP basis the company had a net loss of $11.9 million and EPS of negative $(0.05).

Cash and cash equivalents at the end of the third quarter of 2022 was $198 million, with long-term debt of $667 million.

Key catalysts

Two positive catalysts for the near term and long term are ICE6 and it 100 gig point to multi-point pluggables.

ICE6

What ICE6 does is empower “network operators to meet the demands of rapid bandwidth growth by providing the greatest capacity at the greatest reach, resulting in a solution with the lowest cost and power per bit and the highest spectral efficiency possible.” ICE6, aka the sixth-generation Infinite Capacity Engine, has quickly gained market share and has become a key part of the product segment of the company, with it accounting for more than 30 percent of product revenue in the third quarter, and as mentioned above, should represent about 20 percent to 25 percent of total product sales for all of 2022.

With product sales increasing by approximately $37 million year-over-year, this could be a solid growth catalyst for the company in the quarters ahead, assuming it maintains growth momentum.

100-gig point to multi-point pluggables

This is more of a potential long-term catalyst for the company, which if it is successful with, would result in it competing in a new multibillion-dollar addressable market for INFN.

Its strategy is to develop the pluggables “based upon open multi-source specifications being developed in the Open XR forum.”

Some of the members of the growing forum include DriveNets, UfiSpace, Furukawa Electric, American Tower and Telecom Italia Mobile.

Management believes its pluggables that are underdeveloped in the Forum will revolutionize networks. If accurate, that would be another compelling revenue stream for the company. It’s nothing to count on in the near term but should be watched for future growth potential if it catches on. INFN is also currently developing its next-generation 800-gig pluggables, which management said was “progressing well.”

Quant, Peers and Valuation

Since mid-October INFN has made a nice upward move, but based upon its performance and headwinds it faces, it looks slightly overvalued at this time, even with its Price/Sales (TTM and FWD) being a solid 0.94.

While the company performed well when taking into consideration the headwinds, the fact is the headwinds had a strong impact on its performance, specifically in regard to having to absorb over $50 million in supply chain costs during the full year of 2022.

While that’s true, most of its peers, such as CLFD, and HLIT did very well under similar conditions, with both of them having better quant grades in valuation, growth, profitability, momentum, and EPS revisions. Outside of EPS revisions, DGII also had better quant grades in the other categories than INFN did.

Acknowledging the legitimate impact of the headwinds, the company does have room for operational and efficiency improvement when measured against its peers.

Conclusion

Infinera Corp. has struggled to gain traction since it hit approximately $25.00 per share in August 2015, and from there falling to a low of about $2.73 per share in June 2019, before reversing direction.

Over the last two years, it reached a high of around $11.00 per share on February 15, 2021, and after trading sideways through early April 2022, it pulled back to its 52-week low of $4.255 before rebounding to trade in the $6.00 to $7.00 per share range since November 3, 2022.

For a little over a month, the stock has traded at a floor of slightly under $6.40 while trying to sustainably break above the $7.00 per share mark. If it breaks below or above those levels for a prolonged period of time, it’s going to give a direction to investors on either side of the play.

TradingView

With supply chain issues continuing to eat into the performance of the company, it’s going to be hard to find short-term catalysts that will drive the share price of the company up and hold it there. On the other hand, there is enough sales support for the company to maintain a decent bottom as well.

In the near term we’ll have to see ICE6 continue to grow while its integrated verticals in the product line, account for almost 50 percent of product sales, continue to do well. On the service side it needs to rebuild its backlog there and grow it out.

If it’s able to do those things and it should find support in the current range it’s trading in, and if supply constraints improve, it could be the catalyst the company needs to push it above the $7.00 per share mark and climb from there.

Last, if its pluggables business expands as it hopes, it could be the catalyst, when combined with those mentioned above, which jumpstart the company toward reaching its potential.

I think the best way to play INFN is to wait for corrections in its share price and enter the trade from there. A lot of things will have to go right in the near term for the company to outperform, and getting in at a good entry point would lower risk and of course provide a much better reward to the upside.

Be the first to comment