DenisTangneyJr

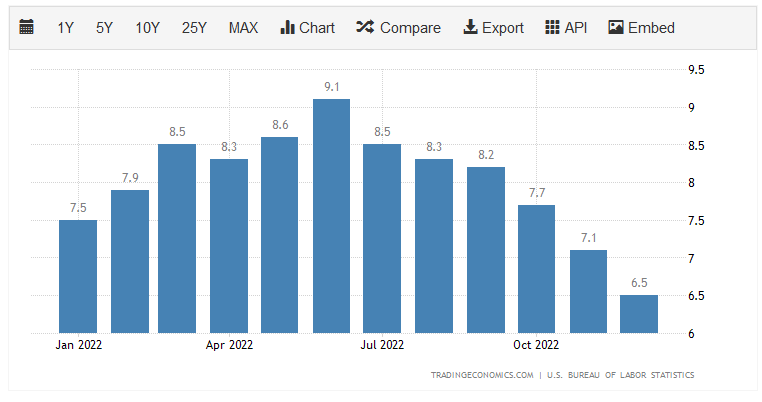

It seems certain that everyone would agree that one of the biggest problems facing Americans today is the high level of inflation that permeates the economy. Indeed, the country has not seen a single month in which the consumer price index did not increase at least 6.5% from the previous year’s level:

Trading Economics

This is the highest rate of inflation that we have seen in more than forty years and it has severely depressed the purchasing power of the money that many people have spent years of their lives saving up. As such, many investors are likely looking for ways to protect the purchasing power of their wealth. One potential option is to purchase real estate as real estate shares many of the characteristics of other things that increase in price during inflationary times. Admittedly, the sector as a whole has performed fairly poorly in the market over the past year but that is due to other factors that in no way diminish the ability of real estate to act as a store of wealth.

One of the best ways to invest in real estate for most people is to purchase shares of a closed-end fund that specializes in investing in real estate. This is because these funds offer the benefit of professional management, which can be a benefit in challenging markets, along with the ability to produce yields that greatly exceed that of the underlying assets. In this article, we will discuss the CBRE Global Real Estate Income Fund (NYSE:IGR), which is one closed-end fund that falls into this category. As of the time of writing, this fund yields an impressive 10.40%, which is clearly higher than that of any equity real estate investment trust. I have discussed this fund before, but that was well over a year ago so obviously, a great many things have changed. This article will therefore focus specifically on those changes as well as provide an updated analysis of the fund’s financial performance.

About The Fund

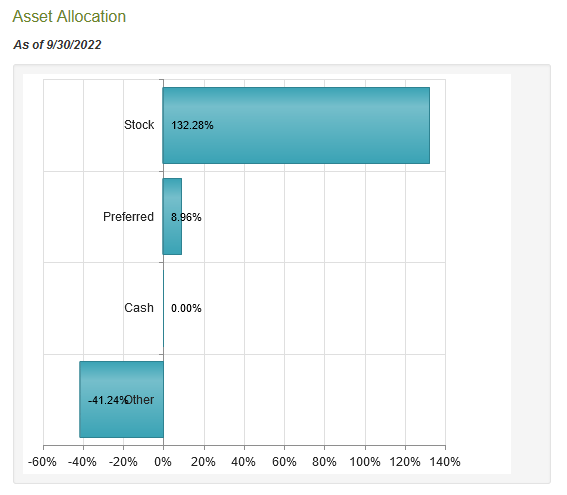

According to the fund’s webpage, the CBRE Global Real Estate Income Fund has the stated objective of providing its investors with a high level of current income. This is hardly surprising since the fund’s income purpose is right in its name. Unlike most income-focused funds though, this one does not primarily invest in fixed-income securities. In fact, only 9% of the portfolio consists of preferred stock and the fund’s portfolio includes no exposure to bonds:

CEF Connect

One thing that just about any reader will certainly notice is that the above figures total more than 100%. This is because the fund employs leverage, which we will discuss later in this article. For now, the most important thing for our purposes is that this is a common equity fund.

It is uncommon for a common equity fund to focus on income because common equities are themselves a total return vehicle. After all, most investors purchase stocks both for the dividend yield and for the potential for capital appreciation. However, real estate is a bit different because it can be an income vehicle. For example, real estate can be rented out to a tenant in exchange for rent. This differs a bit from other stores of wealth, such as gold (GLD). In the United States, many real estate properties used for the purpose of income generation are held by a company that is structured as a real estate investment trust. One characteristic of real estate investment trusts is that they must pay out nearly all of their income in exchange for immunity to corporate taxation. This results in all successful real estate investment trusts paying out distributions and, in most cases, the trust’s stock will have a higher yield than many other things in the market. Thus, income investors frequently include these companies in their portfolio as a vehicle for income and not solely for capital appreciation, as is the case for some stocks. The CBRE Global Real Estate Income Fund invests mostly in these companies, particularly in countries that have a similar type of real estate holding company.

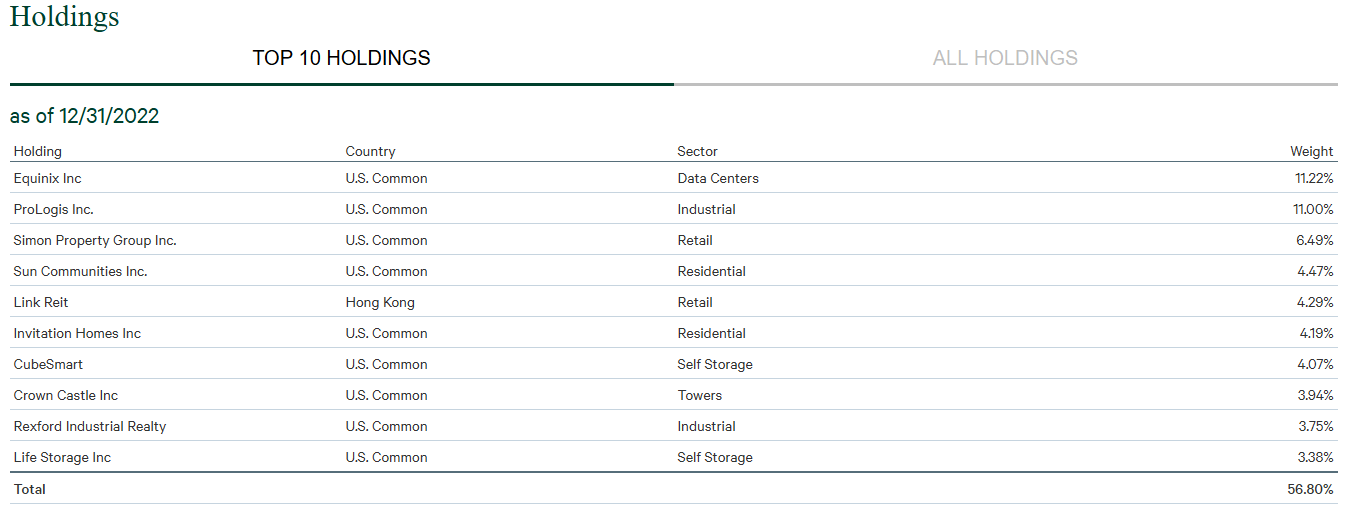

Although I have admittedly not devoted a ton of space in my column on Seeking Alpha discussing real estate investment trusts, many regular readers are income-focused investors and thus probably read about the various companies in the sector. As such, many of the largest positions in this fund will be familiar to most readers. Here they are:

CBRE

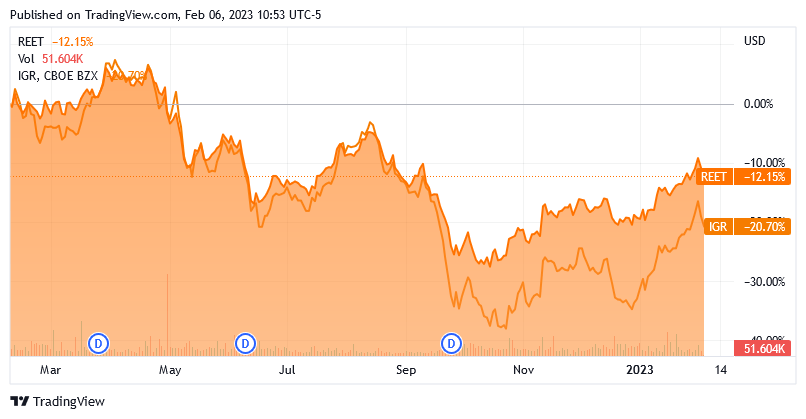

There have been quite a few changes to the fund’s largest positions over the past year and a half since I last discussed this fund. These include the removal of American Tower (AMT), Duke Realty, Extra Space Storage (EXR), and Camden Property Trust (CPT). Of course, Duke Realty was purchased by Prologis (PLD) back in June so its removal may or may not count. Regardless, these four removed companies were replaced with Equinix (EQIX), Sun Communities (SUI), Rexford Industrial (REXR), and Life Storage (LSI). Thus, three companies were outright removed from the largest positions list by the fund’s management and replaced. This may lead one to believe that the fund’s turnover rate is not particularly high as that was only three companies over the course of about eighteen months. In fact, the fund has an annual turnover of 78.44%, which is somewhat high for an equity fund. The reason that this is important is that a high turnover rate acts as a drag on the fund’s performance. After all, it costs money to trade stocks, which is billed to the fund’s shareholders. As such, the fund’s management needs to generate sufficient returns in order to cover these added costs and still have enough left over to please the shareholders. This is something that very few management teams have been able to accomplish consistently and it is one reason why most actively-managed funds tend to underperform their benchmark indices. This fund is certainly no exception to this as it has declined by 20.70% in the past twelve months compared to a 12.15% decline of the iShares Global REIT ETF (REET):

Seeking Alpha

With that said, the CBRE Global Real Estate Income Fund has a substantially higher distribution yield which helps to even up the performance difference between the two funds. However, someone that is holding the fund solely for the preservation of wealth might still opt for the index fund considering that it has managed to preserve its market value better in the increasingly restrictive monetary environment that was caused by the concerted tightening efforts by various central banks over the past year.

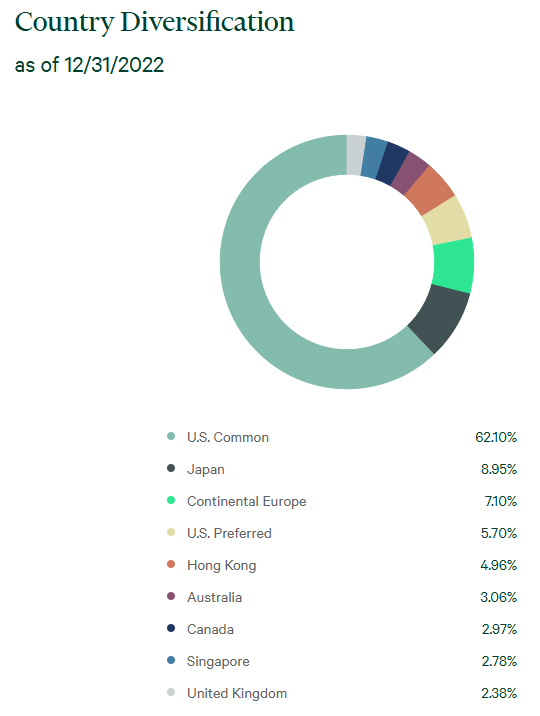

One thing that we notice from looking at the largest positions listed above is that nine out of the ten companies are American ones. This would seem to be at odds with the fact that the fund’s name states that the CBRE Global Real Estate Income Fund is supposedly a global fund. Fortunately, a look at the fund’s broader portfolio shows that it does include a fairly significant foreign allocation. In fact, only 67.80% of the fund’s portfolio is invested in American companies:

CBRE

The United States only accounts for a bit less than a quarter of the global gross domestic product so the fund’s allocation still represents an overexposure to the United States based on that nation’s actual representation in the global economy. However, it is not as bad as we might think just from looking at the largest positions list. It is not unusual for a global fund to have a marked bias toward the United States as that nation’s market has generally outperformed most foreign markets over the past decade. When we consider that the U.S. dollar is broadly strengthening against many foreign currencies, it is not really a bad thing for a fund to be heavily weighted towards America today, either. However, this fund’s high American exposure does mean that it should not be relied on to provide sufficient international exposure to your portfolio and you will want to structure your investments accordingly to achieve that goal.

Real Estate As Wealth Protection

In the introduction to this article, I stated that real estate can act as a way to protect your wealth in an inflationary environment. In order to understand why that would be the case, it is important to understand the root cause of inflation. Despite the claims that some economists make about inflation being a natural occurrence, it is actually the end result of the money supply growing more rapidly than the production of real goods and services in the economy. This is because such a scenario results in more units of fiat currency being available and attempting to purchase a given unit of economic output.

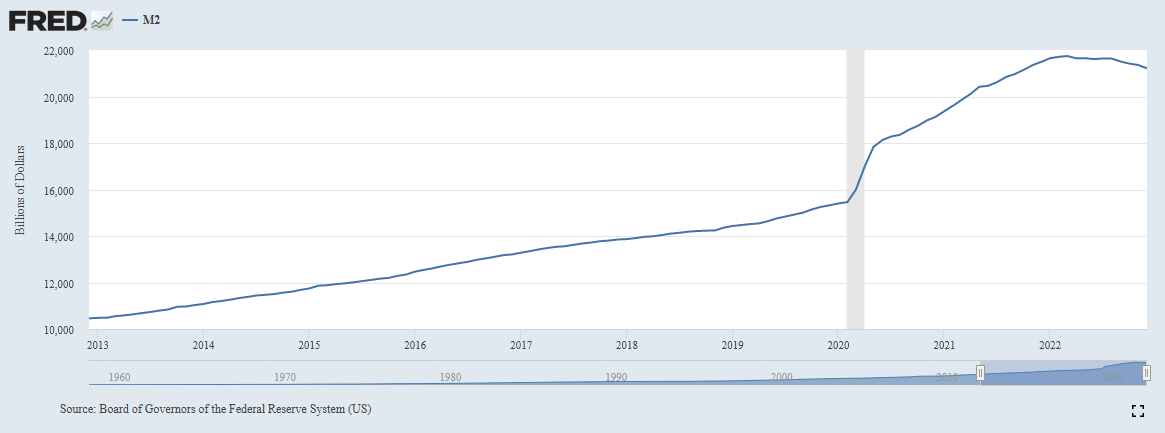

This has been the case in the United States for most of the past decade. We can see this by looking at the M2 money supply (the cash that people have on hand plus checking account balances, savings account balances, and other assets that can easily be converted to cash). As we can see here, the M2 money supply went from $10.4795 trillion in December of 2012 to $21.2074 trillion today:

Federal Reserve Bank of St. Louis

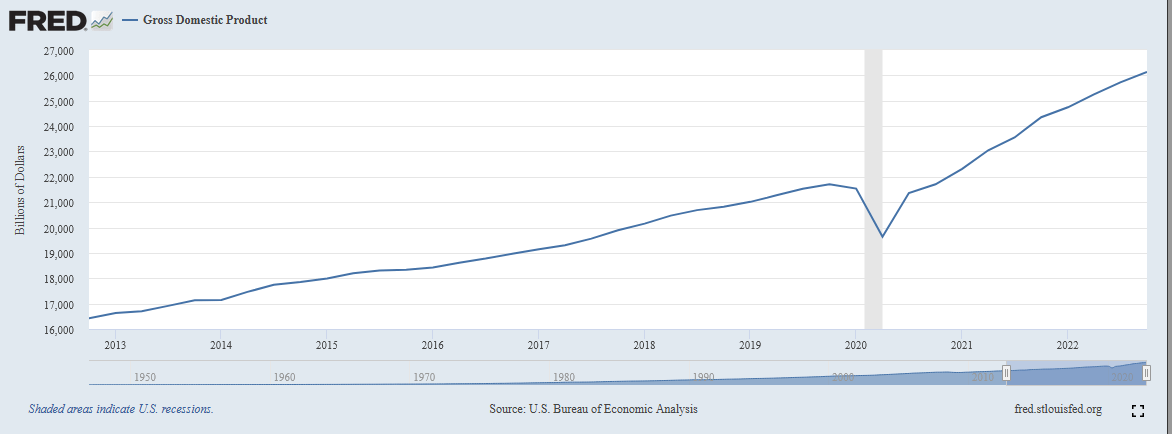

This is a 102.37% increase over the past decade. That is substantially higher than the increase in the actual production of goods and services in the United States. This chart shows the gross domestic product over the same time period:

Federal Reserve Bank of St. Louis

As we can see, the gross domestic product went from $16.420386 trillion to $26.132458 trillion over the same period. That represents a 59.15% increase over the period. Thus, the money supply has grown almost twice as quickly as the nation’s actual economic production over the past ten years. We also see that the money supply’s rate of increase went up fairly dramatically starting in 2020 when the government printed enormous amounts of money to combat the COVID-19 pandemic. That is the root cause of the inflation that we are seeing today.

Real estate can act as a way to preserve wealth because it shares many of the same characteristics as everything else that goes up in price during inflationary periods. For example, real estate requires actual human or mechanical effort to create or improve. Unlike fiat currency, a banker cannot just push a button on a computer and create a house out of thin air. In addition to this, there is only so much land on the planet and this cannot be changed on a whim as the money supply can. As such, as the money supply increases, there is more money available to purchase a given unit of real estate.

With that said, there will undoubtedly be some people that point out that real estate prices have begun to decline. This is perhaps most notable in the stock market as real estate investment trusts have been a losing asset class over the past year. This does not disprove the thesis, however. In the case of publicly-traded real estate investment trusts, what happened is that the rising interest rates made safer financial alternatives more attractive. For example, a 2.5% yield looks pretty good when savings accounts at a bank are paying nothing. When those same savings accounts are paying 4.0%, fewer people will put their money into the 2.5%-yielding stock. In the case of houses, many people purchase those based on the mortgage payment that they can afford. A $250,000 mortgage at 3% is much more affordable than that same mortgage at 7% so the rising interest rates serve to discourage some buyers and thus reduce the demand for a particular home. We have not seen any decline in home prices among those people that are able to purchase a property for cash, however. These individuals are still willing to pay just as much as they did two years ago. Thus, the source of the price reduction in homes is mostly that many people attempting to sell today cannot actually afford to buy a new home without selling their existing one and they are cutting their price in an effort to get someone to buy quickly. Overall, real estate still works pretty well as a store of wealth over the long term for reasons mentioned in the previous paragraph.

Leverage

As mentioned in the introduction, closed-end funds have the ability to generate yields that are often in excess of those possessed by the assets in the underlying portfolio. One of the ways that is employed by the CBRE Global Real Estate Income Fund to accomplish this is the use of leverage, as was mentioned earlier in this article. Basically, the fund is borrowing money and using that borrowed money to purchase shares of real estate investment trusts. As long as the yield that the fund gets from the purchased asset is higher than the interest rate that it has to pay on the borrowed money, this strategy works pretty well to increase the effective yield of the portfolio. As the fund is able to borrow at institutional rates, which are substantially lower than retail rates, this will usually be the case.

However, the use of debt is a double-edged sword. This is because leverage boosts both gains and losses, which is likely to be one reason why this fund declined more than the global real estate index did over the past year. For this reason, it is important that we ensure that the fund is not employing too much leverage since that would expose us to too much risk. I generally do not like to see a fund’s leverage exceed a third as a percentage of its assets for this reason. Fortunately, the CBRE Global Real Estate Income Fund does not appear to be too bad here. As of the time of writing, the fund’s levered assets comprise 29.33% of the portfolio. This is a fairly reasonable level that strikes a nice balance between risk and reward. Overall, it does not appear that we need to be too concerned here.

Distribution Analysis

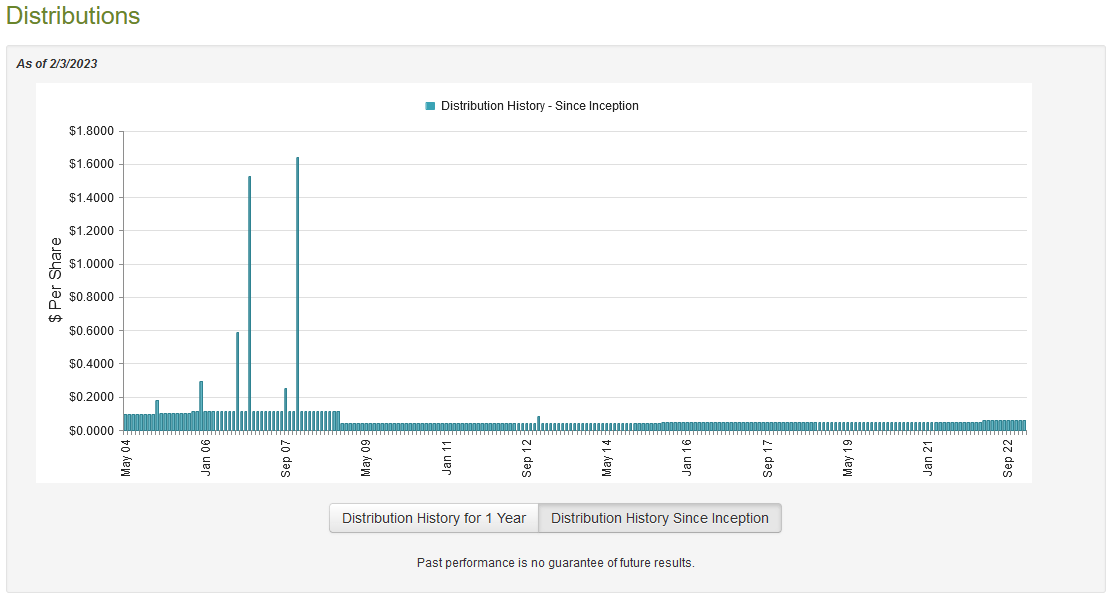

As stated earlier, the primary objective of the CBRE Global Real Estate Income Fund is to provide its investors with a high level of current income. In order to achieve this objective, the fund invests in a portfolio of real estate investment trusts and similar entities, many of which have fairly high yields. It then applies leverage to the portfolio to boost the effective yield of the portfolio. As such, we might expect that the fund would have a fairly high distribution yield. This is certainly the case as the CBRE Global Real Estate Income Fund currently pays a monthly distribution of $0.06 per share ($0.72 per share annually), which gives it a 10.40% yield at the current price. The fund has been remarkably consistent about its distribution since 2009 as it has increased it twice and did not reduce it:

CEF Connect

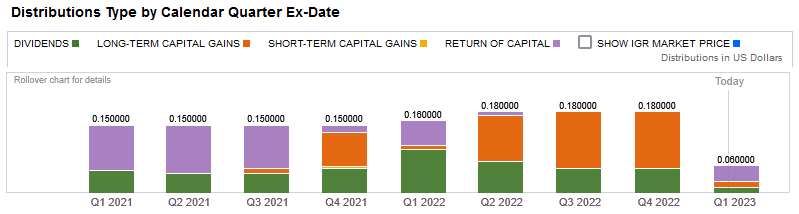

This is likely to be appealing to those investors that are looking for a stable and secure source of income to pay their bills and finance their lifestyles. It also helps further the thesis that real estate can act as a store of wealth over the long term. However, in the past the fund has made numerous return of capital distributions, although these seem to have become somewhat less common in recent quarters:

Fidelity Investments

This is something that may prove to be concerning to more conservative investors because a return of capital distribution can be a sign that the fund is returning the investors’ own money back to them. This is obviously not sustainable over any sort of extended period. However, there are other things that can cause a distribution to be considered a return of capital, such as the distribution of unrealized gains. We also see that the fund has made several capital gains distributions recently. These also may not be sustainable since the fund has to consistently generate large enough capital gains to cover its distribution if it is to maintain it. That is not always possible to accomplish. As such, it is important that we have a look at the fund’s finances in order to determine exactly how it is covering these distributions and how sustainable they are likely to be.

Unfortunately, we do not have an especially current document to consult for this purpose. The fund’s most recent financial report corresponds to the six-month period that ended on June 30, 2022. This report will therefore not include any information about its performance during the past six months. However, the Federal Reserve began its monetary tightening regime in March 2022 so we should still be able to see how well the fund weathered the early stages of that switch in the markets. During the six-month period, the CBRE Global Real Estate Income Fund received a total of $21,255,480 in dividends and $53 in interest from the assets in its portfolio. This gives the fund a total income of $21,255,533 during the six-month period. The fund paid its expenses out of this amount, leaving it with $12,264,803 available for the shareholders. That was, unfortunately, nowhere close to enough to cover the $39,640,768 that the fund actually paid out in distributions during that period, though. This is certainly concerning at first glance.

{kind=link}

Fortunately, there are other ways for the fund to obtain the money that it requires for the distribution. The most important of these is capital gains, and the categorization above indicates that a sizable percentage of the distributions were paid for by capital gains. The fund did certainly have some success at this during the half-year period as it achieved net realized gains of $61,973,214. These were more than offset by massive net unrealized losses of $398,792,346 over the first six months of the year. Overall, the fund’s net assets declined by $364,195,097 after accounting for all inflows and outflows. The fund clearly failed to fully cover its distribution. However, with that said, its net realized gains and net investment income were more than sufficient to cover the payouts for a while, and the strong performance in the market so far in 2023 probably helped its asset values a bit. The fact that the fund had such massive losses does make it more difficult to generate sufficient returns going forward to maintain the distribution. It is probably reasonably safe for now but we do want to keep an eye on the fund to ensure that it manages to generate strong enough performance going forward to keep the distributions covered.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the CBRE Global Real Estate Income Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all of the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund’s assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of February 3, 2023 (the most recent date for which data is currently available), the CBRE Global Real Estate Income Fund had a net asset value of $7.35 per share but the shares currently trade for $6.82 per share. This gives the fund’s shares a 7.21% discount to the net asset value at the current price. This is a more attractive discount than the 4.85% that the shares have had on average over the past month and it is overall a reasonable price to pay for the fund. Thus, the price is quite acceptable today.

Conclusion

In conclusion, the CBRE Global Real Estate Income Fund could provide some wealth protection in the face of the highest inflation that we have seen in nearly four decades. The fund accomplishes this by investing in a portfolio of real estate, which has several qualities that could allow it to act as a store of wealth. Unfortunately, real estate has not delivered the best performance in the market over the past year and that caused this fund to incur some heavy losses. It might be able to maintain the distribution if its portfolio performs fairly well going forward and its attractive valuation does provide some margin of error. The biggest risk here is that the Federal Reserve will continue to hike rates and weaken the market sufficiently to prevent the fund from earning enough capital gains to maintain the distribution. Overall, though, it might be worth taking a chance on this fund.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment