DNY59

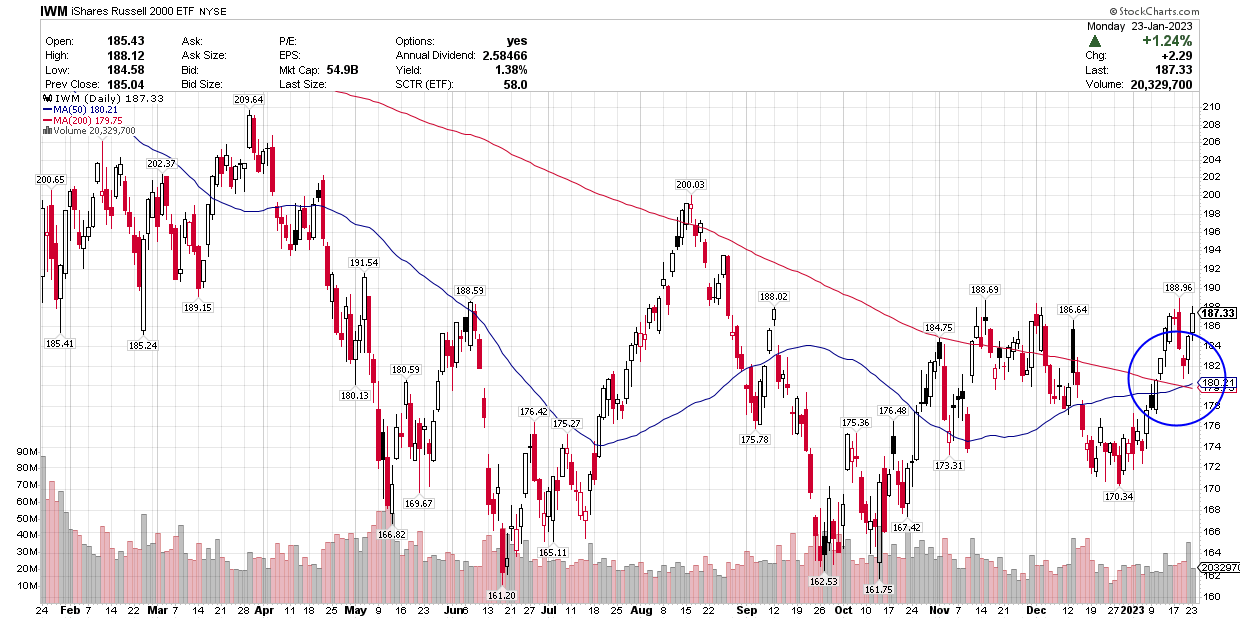

The bulls are clearly gaining ground over the bears so far this year in the ongoing tug-of-war over the major market averages. The S&P 500 (SPY) closed well above its 200-day moving average for a second time yesterday in as many weeks, joining a much stronger Russell 2000 index (IWM), which completed a Bullish Cross. In other words, this domestically-focused small-cap index saw its short-term moving average (50-day) cross above its long-term moving average (200-day), as seen in the chart below. From a technical standpoint, that is as good as it gets, suggesting higher prices ahead. If the market is serving as a leading indicator, then the outlook for a soft landing is starting to look more promising than the one calling for a recession and retest of the bear-market lows.

Finviz

The bears have obsessed over inflation and how the Fed has said it will respond to it. If inflation is the most lagging of all economic indicators, then the Fed is the most lagging of all financial institutions. Neither is a valuable input when determining the direction of the economy or markets. That is why I have repeatedly stated to ignore what Fed officials say the past several months and listen to the market. The market is the best leading indicator to follow, and it says that the macroeconomic landscape is on the mend. The bears will retort with the message the bond market is sending us through an inverted yield curve, but I’d say that is a mixed message at best. Beyond the inversion, we do not see stress in the credit markets that indicates a broad economic downturn.

Stockcharts

I first suggested the likelihood of a soft landing last November, which describes an economic environment whereby the rate of growth slows to the extent that it brings the rate of inflation down to the Fed’s target of approximately 2% without causing a recession. My outlook was based on the strength of consumer balance sheets, buttressed by post-pandemic stimulus and an extremely strong labor market. The market didn’t agree with that outlook at the time, but things have changed since last fall.

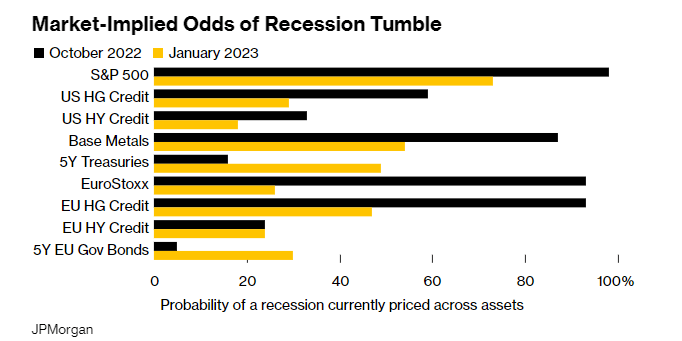

According to JPMorgan’s trading model, seven of nine asset classes now show less than a 50% chance of recession. The odds were closer to 100% last fall. As it relates to the bond market, US high-yield bonds have realized the sharpest decline, based on market prices, to just an 18% chance of recession. Morgan Stanley economists are now calling for a “softish” landing this year and suggest that even if we do have a recession it will be mild at worst. They are basing this on a labor market that has proven to be stronger than expected and a sharp downturn in the rate of inflation. This lessening of negativity explains the S&P 500’s jagged grind upward of approximately 14% from its October low, and I think it can continue.

Bloomberg

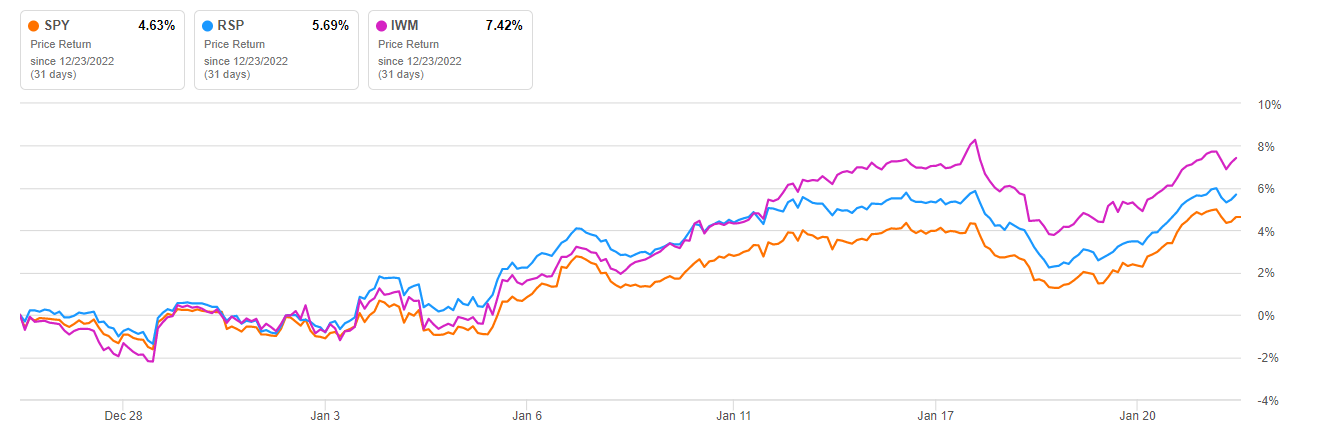

Last week I discussed the recent outperformance of the equal-weighted S&P 500 and Russell 2000 index with the point being that the average stock has been doing a whole lot better than the large-cap weighted indexes, which are still under the influence of the largest tech-related market caps. In other words, breadth has been improving, as more stocks are advancing than declining. This can be seen in the outperformance of small versus medium versus large companies over the past month in the indexes below. This does not portend an economic downturn.

Seeking Alpha

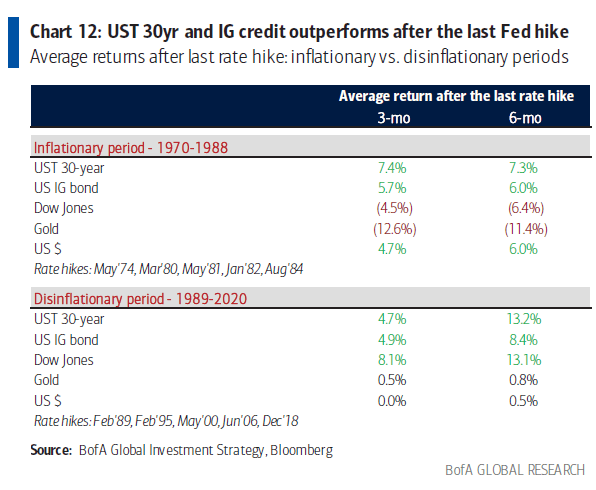

I think the market is also sensing that next week’s interest-rate increase by the Federal Reserve (25-basis-points) could be its last. I expect inflation measures and labor market conditions between now and the Fed’s next meeting in March will give Chairman Powell enough confidence to end its rate-hike cycle. The importance of this is that market returns during disinflationary periods following the last rate hike over the past 40-plus years have been bullish for stocks and bonds. This is not the inflation of the 1970-1988 period.

Bloomberg

While the odds increase that the bear-market lows are behind us, that doesn’t mean we rocket ship to new all-time highs anytime soon. I think the S&P 500 can produce a 10% return this year, but the better opportunities will be found in sectors and stocks that have more reasonable valuations than the major market averages, which remain expensive. The increases in volatility that lead to pullbacks in the market will present those opportunities.

Lots of services offer investment ideas, but few offer a comprehensive top-down investment strategy that helps you tactically shift your asset allocation between offense and defense. That is how The Portfolio Architect compliments other services that focus on the bottom-ups security analysis of REITs, CEFs, ETFs, dividend-paying stocks and other securities.

Be the first to comment