matdesign24

Markets had a tumultuous 2022. Inflation skyrocketed, interest rates rose, and most asset classes and investments went down, and by a lot. Market conditions have changed, and have changed in ways that broadly benefit high yield corporate bonds, at least vis a vis bonds in general.

Interest rate hikes almost always lead to lower bond prices. High yield corporate bonds tend to be of relatively short maturities and duration, and so fare comparatively well when interest rates are rising.

Worsening economic conditions and bearish market sentiment have caused high yield bond spreads to widen, with said securities offering comparatively strong yields today. High yield bonds always yield more than comparable investment-grade bonds, but the gap has widened these past few months.

Economic conditions have worsened, but remain reasonably good, with default rates at below-average levels. Analysts expect default rates to remain somewhere between below-average and average for the next few years too, even if a recession does materialize.

High yield bonds offer investors strong yields, low interest rate risk, and default rates remain, and are expected to remain, at reasonably low levels. Under these conditions, high yield bonds are set to have a strong 2023, at least relative to other bonds.

The iShares iBoxx $ High Yield Corporate Bond ETF (NYSEARCA:HYG) is the largest, most well-known high yield corporate bond ETF in the market, the industry benchmark, and benefits from the trends above. Other similar funds would benefit from the same trends as well.

HYG – Quick Overview

A quick overview on HYG before looking at some high yield corporate bond trends.

HYG is a high yield corporate bond index ETF, tracking the Markit iBoxx USD Liquid High Yield Index. HYG’s underlying index includes most relevant dollar-denominated high yield corporate bonds in the market, subject to a basic set of inclusion criteria. HYG’s underlying index is quite broad, and so the fund can be used as a benchmark for the dollar-denominated high yield corporate bond market.

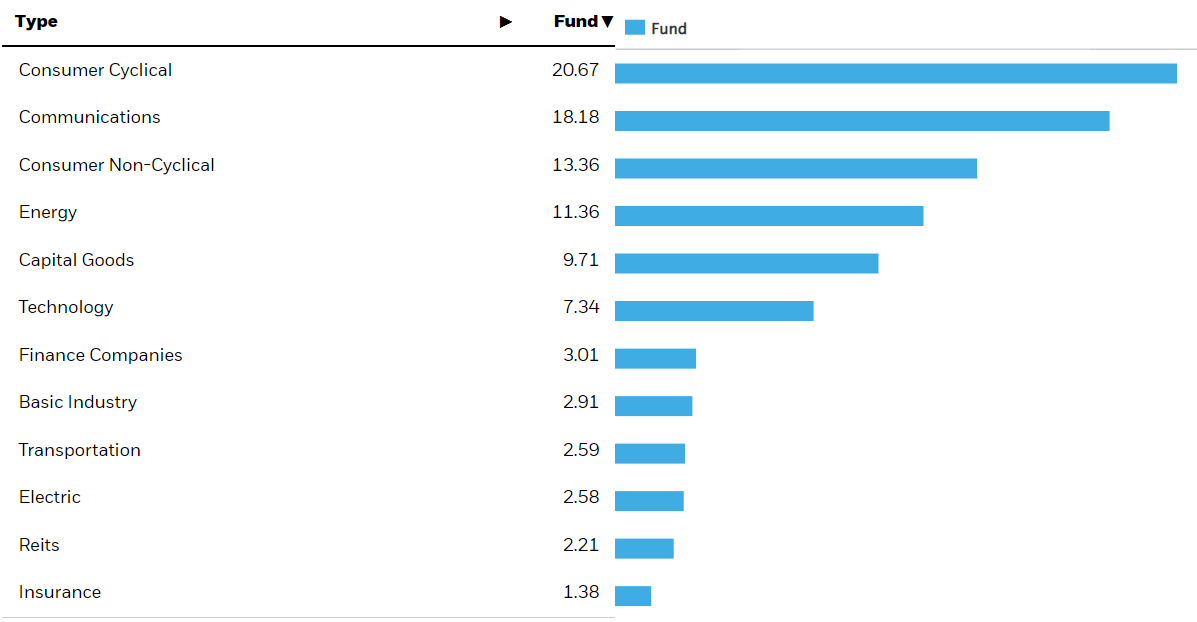

HYG is a reasonably well-diversified fund, with investments in over 1000 securities from all relevant industry segments. Concentration is low too, with the fund’s top ten issuers accounting for just 13% of its value.

HYG

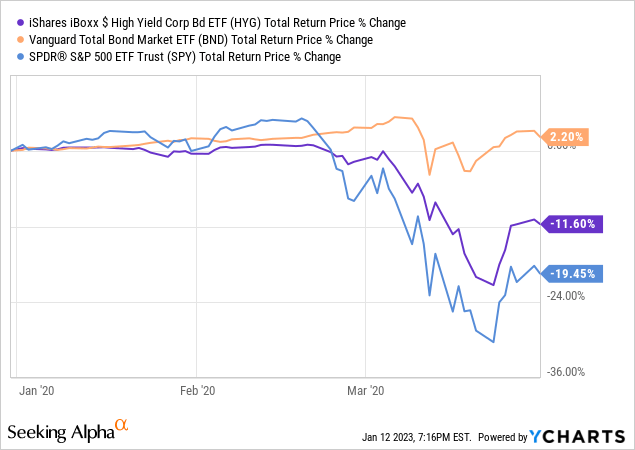

HYG’s underlying holdings are (effectively) all non-investment grade bonds, with low credit ratings. These are indicative of weak issuers, with poor balance sheets and financials. Repayment is somewhat dependent on economic and industry conditions, so default rates tend to increase during downturns and recessions, triggering losses. Expect the fund to underperform bonds during these scenarios, although it should still perform outperform equities. This was the case during 1Q2020, the most recent downturn, as expected.

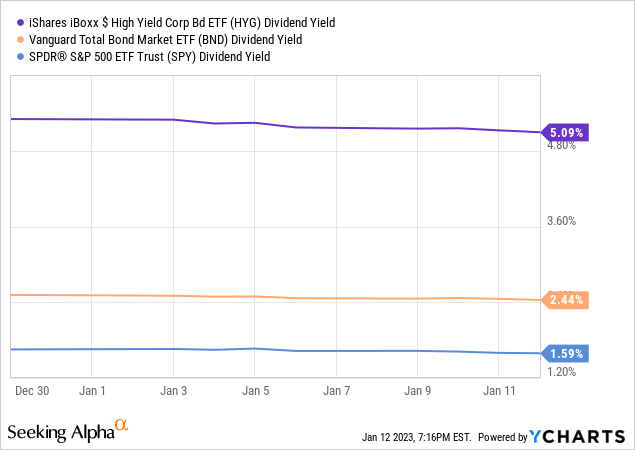

To compensate for the above, HYG’s underlying holdings sport above-average interest rates, which result in above-average dividends for the fund and its shareholders. HYG itself yields 5.1%, a reasonably good amount, and quite a bit higher than both equities and bonds.

High yield corporate bond interest rates are dependent on many factors, including Federal Reserve interest rate. All else equal, higher Fed rates means higher corporate bond rates, which means higher income for HYG, and greater dividends for the fund’s shareholders. Rates have risen these past twelve months, during which HYG’s dividends have seen healthy growth, as expected.

SeekingAlpha

HYG is a simple high yield corporate bond index ETF, with all that characteristics that entails.

With this in mind, let’s have a look at some important high yield corporate bond trends / characteristics.

High Yield Corporate Bonds

Low Interest Rate Risk

The Federal Reserve is aggressively hiking interest rates, in a bid to combat elevated inflation. Higher interest rates almost always reduce demand for older, lower-yielding bonds, including those owned by HYG and other ETFs. As demand goes down so do prices, leading to capital losses for bond investors and bond funds.

Although most bonds see losses when interest rates rise, the magnitude of said losses varies. Short-term bonds tend to see comparatively low losses, as these bonds mature quickly, and so are quickly replaced for newer, higher-yielding bonds. Long-term bonds tend to see comparatively high losses, as these bonds take a long time to mature. Interest rate sensitivity can be estimated through duration, with higher duration meaning higher interest rate sensitivity, and greater losses when interest rates rise.

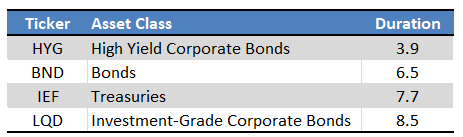

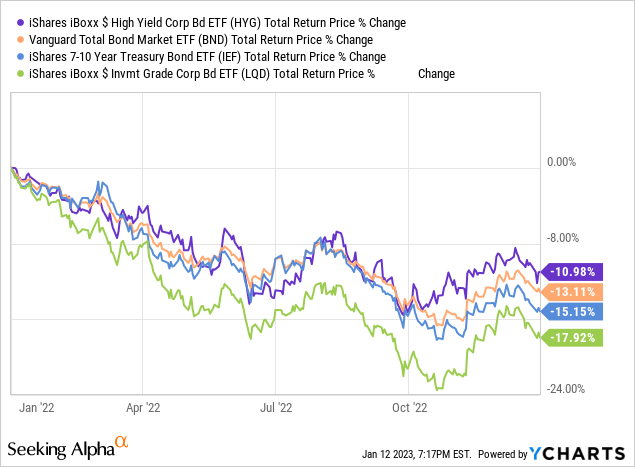

High yield corporate bonds tend to have below-average maturities, as investors are generally loathe to loan money to risky issuers at long maturities. Due to this, high yield corporate bonds tend to have low duration / interest rate risk, as is the case with HYG.

Fund Filings – Chart by Author

HYG’s relatively low duration should lead to below-average losses / outperformance during periods of rising rates, as was the case in 2022.

HYG’s relatively low duration is an important benefit for the fund and its shareholders, and one which is particularly important right now. Most high yield corporate bond funds have low durations too, benefitting their shareholders as well.

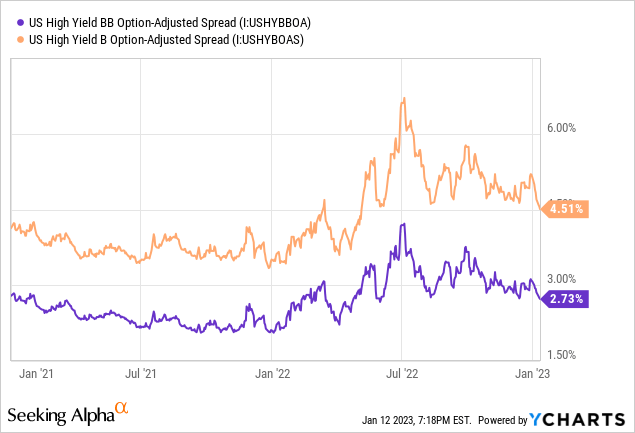

Above-Average Interest Rate Spreads

High yield corporate bonds effectively always carry higher interest rates than comparable investment-grade bonds. Spreads do vary, and are currently somewhat higher than average, due to worsening economic fundamentals and bearish investor sentiment.

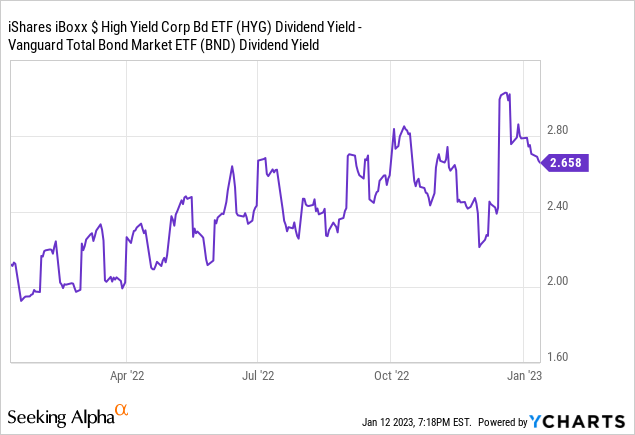

Spreads between HYG and broader bond index funds are also at above-average levels right now.

Wider credit spreads means high yield corporate bond yields and expected returns are looking very attractive relative to other bonds, and much more so than in the past. Treasuries, T-bills, investment-grade bonds and money market funds are all yielding more than in the past, but so are high yield corporate bonds, and by more than these other asset classes.

Economic Conditions

As previously mentioned, corporate bond spreads have widened due to worsening economic conditions and bearish market sentiment. Investors think a recession is imminent, and are selling risky investments, including high yield corporate bonds. Selling pressure has caused bond prices to go down, and yields to surge. Further selling pressure would almost certainly materialize if a recession were to occur, which seems possible, if not certain.

Although economic conditions have definitely worsened, conditions remain broadly adequate. The U.S. economy continues to grow, inflation continues to go down, and job growth remains strong. Default rates are ticking up, but remain significantly below historical averages.

J.P. Morgan Guide to the Markets

Some analysts are expecting a recession in the coming months, but few seem to expect a significant increase in defaults. S&P believes default rates could double by late 2023, reaching 3.75%. Although this would be a significant increase in default rates, defaults would remain at reasonably levels, barely above their historical average.

S&P

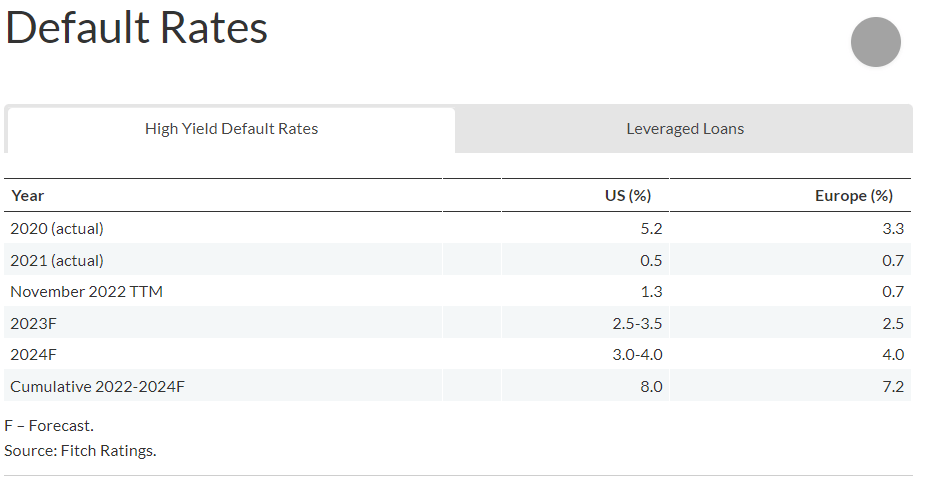

Fitch is more bullish, expecting default rates of 2.5% – 3.5% in 2023, 3.0% – 4.0% in 2024. As with S&P, the expectation is for a significant increase in default rates, but for conditions to remain at historically average levels.

Fitch

In my opinion, economic conditions are adequate enough for strong high yield corporate bond returns in 2023. I’m not seeing signs for or expecting a brutal recession this year, and neither are most analysts. Credit rating agencies do expect an increase in defaults, but nothing outside normal parameters. Under these conditions, high yield corporate bonds seem likely to perform well in 2023, in my opinion at least.

Conclusion

Market conditions have changed, and have changed in ways that broadly benefit high yield corporate bonds, at least vis a vis bonds in general.

Interest rate have risen, which benefits low duration bonds, which includes high yield corporate bonds.

Interest rate spreads have widened, benefitting high yield corporate bonds.

Economic conditions remain adequate, which should allow high yield corporate bonds to thrive.

Under these conditions, high yield corporate bonds seem like comparatively strong investments. HYG is a simple high yield corporate bond index ETF, and provides investors with diversified exposure to a strong asset class.

Be the first to comment