jimfeng/E+ via Getty Images

All values are in CAD unless noted otherwise.

We believe in the popular adage that “if you love a company, but it is overvalued, don’t chase it. If it comes back into your buying range, it is yours. Or else it was never meant to be”. Staunchly following it along with the equally popular saying that “there are plenty of fish in the sea” has generally worked in the favor of our investment returns.

Hydro One Limited (OTCPK:HRNNF) was one such Canadian utility company. A combo of the above two principals kept us away when we covered it back in September 2021. The business was thriving, but the numbers failed to make a buy case looking out to 2023.

The key reason here is that investors have piled in here into this “bond proxy” as benchmark yields have fallen. But that is what creates the issue here as bond yields are very far removed from the reality of inflation rates.

Any kind of normalization of rates would hurt Hydro One’s stock price by a fair amount. We would look at get constructive if we get a 4% dividend yield on this one.

Source: Hydro One: Where To Pick Up This Strong Utility

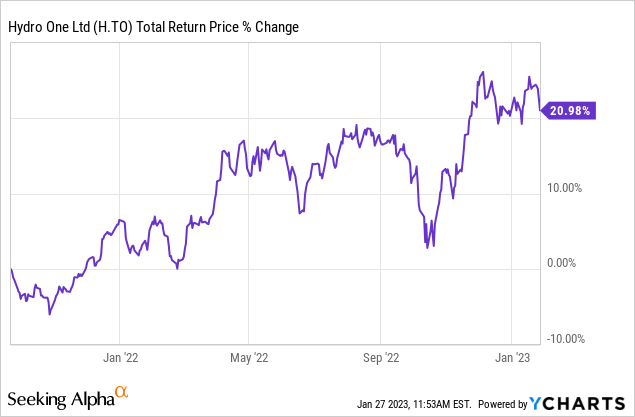

We suggested either staying away, or getting involved via cash secured puts. Simply going long served investors well instead as the stock has done very well since then.

It almost gave away all the returns a couple of times in 2022, but bounced right back up. Were those dips a precursor or warning to investors of what is to come? We review the recent numbers to see if perhaps this one was never meant to be for us or whether we think it will be ripe for bottom fishing soon.

Q3-2022

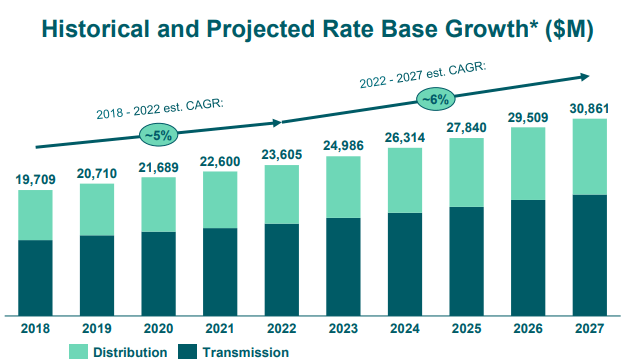

The recent results from Hydro One were strong and earnings came in at 51 cents a share, about 4% ahead of consensus. The results were driven by good cost control and higher peak demand. More importantly for Hydro One it filed a settlement agreement with the Ontario Energy Board. This agreement pertains to its Joint Rate Application (JRAP) for its transmission and distribution assets and runs from 2023-2027. Base rate revenue growth is expected to increase at least 6% a year through 2027.

Hydro One Q3-2022 Presentation

Further details can be seen in the slide below.

Hydro One Q3-2022 Presentation

Hydro One earnings and dividends could grow at about 4%-6% a year. This was a small overhang on the stock and with the next 5 year plan approved, the company can focus on execution.

Valuation & Outlook

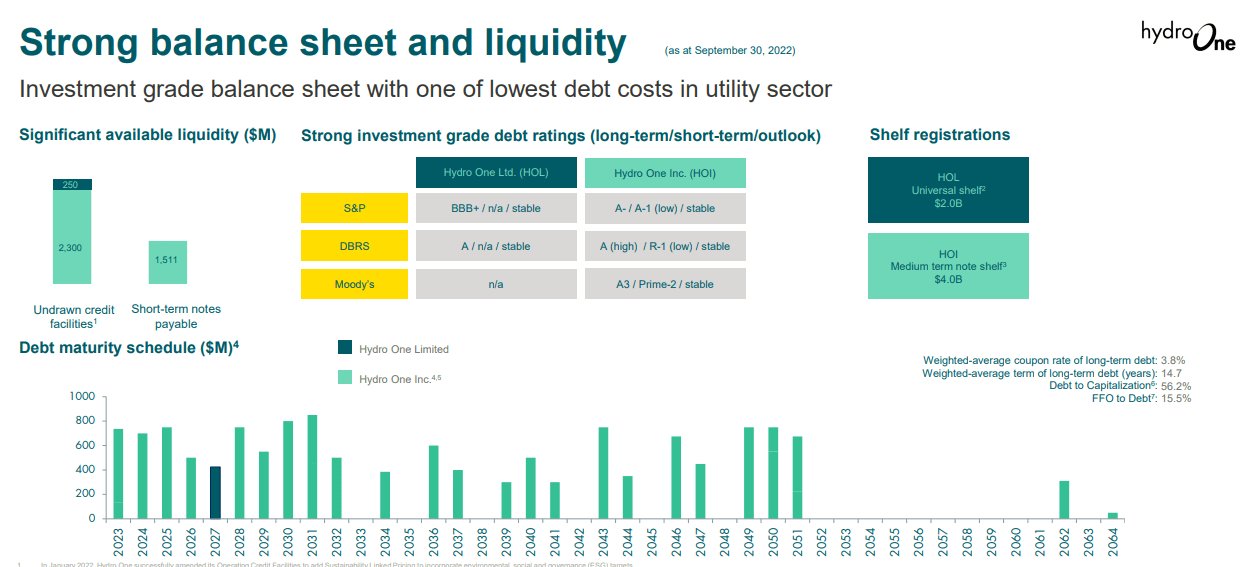

Thanks to the Government of Ontario’s stake in the company, Hydro One tends to have a lower beta than most other utilities. This government backing has also led to the lowest debt costs in the utility sector, coupled with high marks from the credit rating agencies.

Hydro One Q3-2022 Presentation

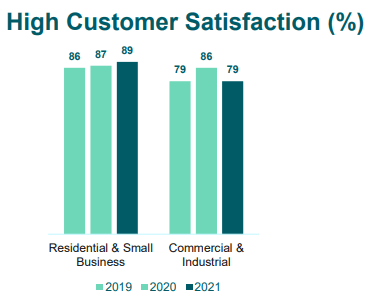

To be clear, it is not just the government backing. Historically, Hydro One has delivered very strong and consistent results. They have also done so while having an extremely high customer satisfaction rate.

Hydro One Q3-2022 Presentation

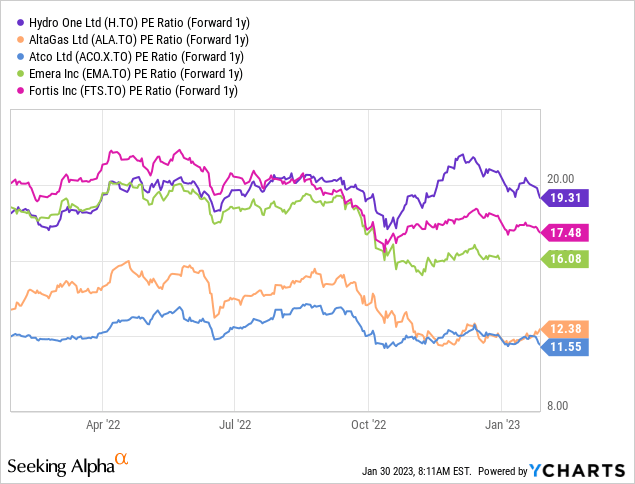

That is a rare combination for a utility company. But all that goodness looks well if not perfectly, priced in. As with all investments, your only hopes of great return come from what you pay for it. This is where the case for Hydro One really falls apart. As we write this, Hydro One last traded at $36.39. Full year earnings are not out yet, but Hydro One is about as predictable as they get and we would expect it not to stray too far from the expected $1.70 mark. We are trading at 21.5X earnings. Going out to 2023, this improves to about 19.5X. This is a tough sell for any investor who objectively looks at what they are paying. This logic also applies to people holding on a lower cost basis as by holding, that is what you are indirectly paying.

We ran this number against what we believe are good comparatives here in Canada.

1) AltaGas Ltd. (ALA:CA)

2) ATCO Ltd. (ACO.X:CA)

3) Emera Inc. (EMA:CA)

4) Fortis Inc. (FTS:CA)

The above companies are the ones we used to plot our chart.

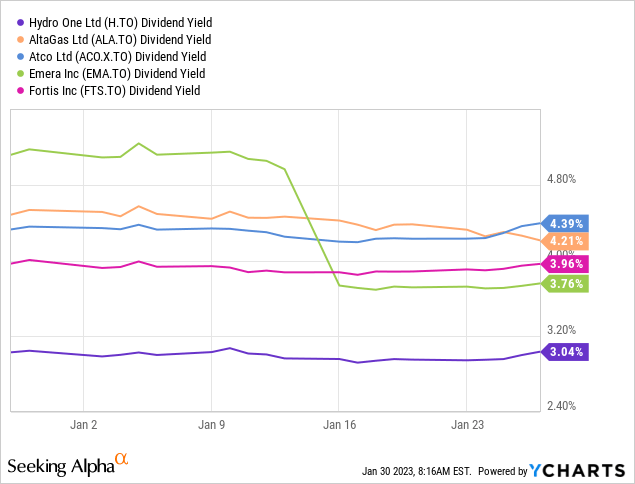

You can argue about the better model here for Hydro One (with quasi government support), but you are also paying through your nose here. From an income investor’s standpoint, the dividend yield isn’t really great, either.

Sometimes a higher P/E ratio (and consequently a lower dividend yield) is a result of lower debt ratios. That is certainly not the case here as AltaGas (post its planned Alaskan Utilities sale) and Atco Ltd, both will have lower debt to EBITDA ratios on 2023 numbers.

Verdict

As much as we would like to embrace investing in Hydro One, these valuations don’t support it. With any kind of modest valuation compression, you are likely to get negative total returns over 4-5 year periods. Within utilities, there are far better options designed to provide better income and better total returns. At a 3% yield, Hydro One is likely to be one of the most sensitive to any new tremors in the bond markets. We had rated it a “Hold” the last time, but the current valuation puts its squarely in the Sell zone. We are downgrading it as a result and think better opportunities lie elsewhere.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment