Just bringing in more crap that will go through TRNO’s industrial real estate.

bfk92

This article was previously provided to members of The REIT Forum.

Terreno (NYSE:TRNO) provided their Q4 2022 Update.

Portfolio results are still strong. Occupancy up. Cash leasing spreads are down from Q2 and Q3, but who hates 45.2%? A small increase in shares outstanding provides additional cash for redevelopment projects that significantly increase the rental revenue on properties.

Shares fell hard during 2022, but even after the decline, they’ve been a huge winner for long-term shareholders. The same real estate fundamentals that drove TRNO’s growth over the last several years remain in place. While interest rates are higher, demand from tenants is the more important metric from our point of view.

Note: Sometimes, we grade the quarter with a value out of 10. Since TRNO’s update doesn’t include 100% of the metrics, I’m hesitant to assign an exact number. However, we do have enough information to say it would be a high value.

Occupancy

Same-property occupancy increased from 98.9% to 99.5% as TRNO leased the majority of their remaining space. There simply isn’t much property remaining without a tenant.

Note: Total occupancy (which includes other properties) was still 98.6%, up from 98.4%. We focus on same-property occupancy as it is often a better metric for comparison.

Cash Leasing Spreads

These values will be a bit volatile from quarter to quarter because a few large leases can swing the results. However, they remain strong.

- Q4 2022: 45.2%

- Q3 2022: 65.9%

- Q2 2022: 55.4%

- Q1 2022: 34.8%

- Full-year weighted average: 49.5%

Leasing spreads could be coming in a bit as the economy weakens, but TRNO also was quite actively leasing as evidenced by occupancy moving up to 99.5% for the same-property pool.

Equity

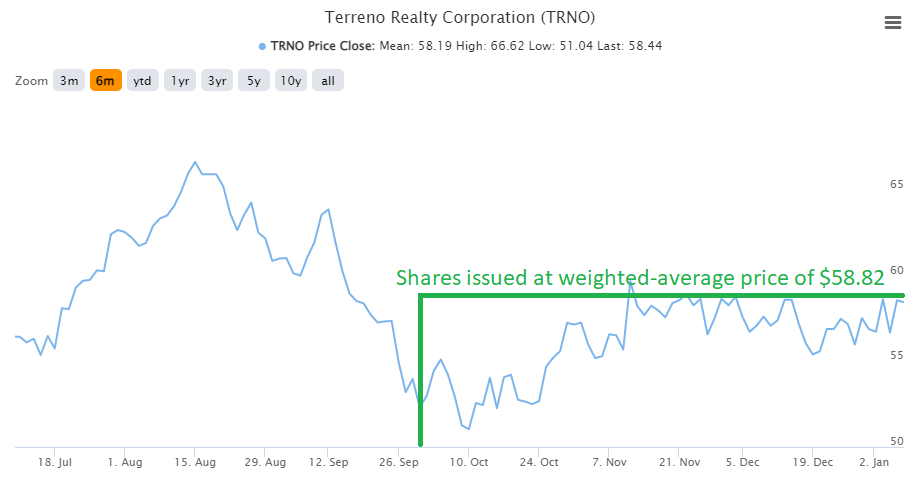

TRNO was actively issuing shares again. Their acquisitions have usually added significant value for shareholders. I’m not a huge fan of the decision to issue here, given the valuation, but TRNO’s management has been consistently wise. I’ll give credit where it is due and wait to see what they buy with the cash.

They issued 814,526 million shares for $47.9 million. The weighted average price was $58.82.

Wait, what? Only $47.9 million? That’s not very much. The 814,526 shares are about a 1% increase in shares outstanding. That’s not enough to warrant much concern.

Where Did the Cash Go?

- TRNO spent $59.4 million on buying industrial real estate.

- TRNO sold three properties for a total of $57.9 million.

For the real estate TRNO sold, they achieved unleveraged internal rates of return (cash flow analysis) from 14.1% to 20.7%. They’re good at running this REIT.

Those two values offset each other. However, TRNO invests in improving their property. They buy some properties that will need investment to maximize the value. Issuing shares is a way to get some extra cash to fund the redevelopment, which often provides a very attractive return to investors who can do it as well as TRNO’s management.

The returns on those redevelopments are high enough to warrant issuing shares, even at less-than-stellar prices. However, TRNO’s management has been pretty good at getting prices at the higher end of the range for the quarter:

TIKR.com

Within that period, they did a good job of issuing near the top.

I wouldn’t mind if TRNO took on slightly more debt to fund the redevelopment, though things get a bit awkward with higher interest rates. For AFFO per share, issuing shares around 35x to 36x AFFO (an AFFO yield of less than 3%) creates a smaller drag on AFFO per share than taking on debt around 5%.

I value the growth in NAV per share more, but this strategy helped optimize for AFFO per share growth in the near term. While projects could be delayed, the exceptional yield available on the final cash flows is excellent. Further, one of the reasons I like TRNO as an investment is because they are so careful with their leverage.

Current Price Update

Shares have rallied since early January and now trade at $64.13. The market hasn’t quite closed at the time of writing. Therefore, the closing price today may be slightly different.

TRNO took advantage of the rallying share price to issue shares at $62.50. I would’ve liked to see a slightly higher price since they closed at $65.12 the day before the announcement.

However, I’m confident in management’s ability to drive value for shareholders. Since consensus NAV estimates were lower than the issuance price, the decision to issue shares pushed NAV estimates slightly higher.

Conclusion

Looks like another good quarter for TRNO. Even if rent growth cooled down a bit during the period, it remains strong. Further, TRNO has been very effective at bringing in tenants. When they wanted some cash for funding redevelopments, they still achieved a price near the top of the range. I remain bullish on TRNO and continue to expect them to deliver significant growth across the next several years.

TRNO is one of our larger positions. It comprises about 4.25% of our total portfolio.

Outlook: Bullish on TRNO

Be the first to comment