jimfeng/E+ via Getty Images

The housing market continues to show strength in terms of pricing, but primarily due to issues in volume. What’s going on? Shortages all around, born primarily of issues in logistics, with ports overwhelmed, flatbeds insufficient and container prices having doubled since they’ve become so hard to come by. Materials are short, and housing inventory has slowed down substantially in terms of turnover because there are so many unfinished units. With the fact that Millennials are finally forming families and there is underlying population growth, not to mention more square-footage needed for work-from-home purposes, the slowing inventory has exacerbated an already forming housing shortage and rising prices. What stocks stand to benefit from this current situation of bottlenecking at the end of the building cycle? We think there is sustainable demand for PVC and finishings, and that there is pent-up demand for lumber and OSB on the next start of the building cycle. Moreover, you can never go wrong with commodities used in paint and coatings.

While rising rates are a legitimate concern for investors, the big development from our previous view that predicted substantial rate increases is the return of the experience economy, which could take the pressure off the productive frontier by claiming share from the goods trade. Rate hikes might not have to be the only instrument to reduce goods demand, and we are more likely at this point to avoid a deleveraging.

Goods vs. Services

Services are actually a much bigger proportion of GDP than goods. Globally, services are about 60% of GDP, and tourism alone is 10%. Services generally fell quite a lot, with tourism probably being the worst, falling by 50%. With out-of-home commerce being a large proportion of services, which we knew fell at least 30% during the pandemic, you can imagine the substantial hit that services took, with money printing allowing goods demand to take their place. Goods demand increased by perhaps 18% as a consequence of the pandemic.

Capacity increases are coming to the tune of 20-30% in some cases, and this should have been enough to deal with inflation. The problem is that shortages are slowing down capacity increases, and logistic shortages are some of the most acute shortages of all. So this is not solving the problem soon enough. In the meantime, expectation effects leaking into the wage-price mechanism, as well as speculation, especially worsened by Russia invading Ukraine and their supply of energy being hoarded and less than reliable, are creating a massive economic problem that could require pretty substantial rate increases to calm down. The key thing the Fed is trying to do is not cause a deleveraging as a consequence.

Our view was that rates would have to increase to 6% in order to smother disposable income enough to take the burden off of the goods trade and tackle inflation. A 6% rate would be a mess for the housing market, even though a housing shortage is creating secular demand. But our newer view incorporates a very promising return of the experience economy, and the recovery in mobility which should together restore services. We are seeing good recovery in a lot of the barometers that track mobility. Even commercial aviation manufacturers, where capital outlays are quite risky by customers, are seeing an uptick. Airports are full, and that is a sign that the experience economy is coming back. Even if it only partially recovers, that should reduce the needed interest rate to stymie inflation to no more than 4%, which is a manageable figure for the economy, with capacity increases hopefully allowing it to come down again to 2-3%.

While the limited increases in rates are something we are hopeful about, we still recognise that it is all very uncertain, especially with geopolitics playing a role. Nonetheless, the stocks we are looking at are priced as if the housing market is looking at certain disaster. The housing shortage already means that there is pent-up demand, making it a stronger point of the US economy, but with the return of mobility, we could be in an even better place where excessive worries about interest rates might not be necessary anymore, certainly rendering all these stocks’ late-cycle multiples unwarranted. Nonetheless, these quality picks have a lot going for them regardless.

Tronox (TROX)

The first stock to consider is Tronox. They are a vertically integrated producer of titanium oxide, which is used to give paints and coatings their luster. The vertical integration is what you should focus on, because titanium is one of several resources that are found in large part in Russia, and could become dangerously scarce. Tronox owns their own titanium and zircon mines which account for 85% of the company’s used feedstock. This is resilience in both the cost structure and business continuity that they can offer. For asset-heavy companies, having the lowest cost assets is an excellent competitive advantage, and having their own titanium mines, which is a key input for aerospace including military aerospace, is critical.

While TROX is not entirely dependent on real estate construction, painting and coatings are major products used in the construction industry, in addition to automotive. With cost savings coming in at more than 20% in the coming years, the current 4.9x EV/EBITDA multiple could shrink on current income to about 3.9x. The margin of safety here is substantial on the low valuation, and a fixed cost structure puts them way ahead of any competitors.

Westlake (WLK)

Another very interesting company is Westlake. They are quite explicitly involved in the manufacturing of products and materials that are more often used later in the building cycle, indeed where shortages currently are. WLK is a chemicals company that produces polyethylene, styrene, vinyls and PVC as well as sells to end-markets finished products like windows, fittings and piping, where they capture the full chain of value by bringing it to the final customer. Many of these products come from cheap NGLs that are total commodities from shale oil processes, products that are sometimes even burnt or flared off rather than piped over. The margins are strong for this company, where it is of course still cyclical, but less so because they are closer to final customers.

When shortages of garage doors and other finishings for houses are what is keeping inventory unfinished and out of the hands of the market, it means that the demand for products like Westlake’s involved in getting a house ready to be brought to the typical buyer is also experiencing pent-up demand. With the shortage of housing constituting a long-term opportunity for demand for WLK’s products, the company appears very attractive at valuations of 7x for PE and 4.6x for EV/EBITDA. Again, substantial margins of safety and a great value proposition if you believe that we are still in an upcycle for building product volumes, where the housing shortage constitutes a supercycle for these products.

West Fraser Timber (WFG) and Interfor (OTCPK:IFSPF)

Westlake and Tronox are a little less commodified thanks to their final-customer facing businesses and the valuable mines respectively. Interfor and WFG are much more commodified as sellers of lumber, and in the case of WFG also OSB.

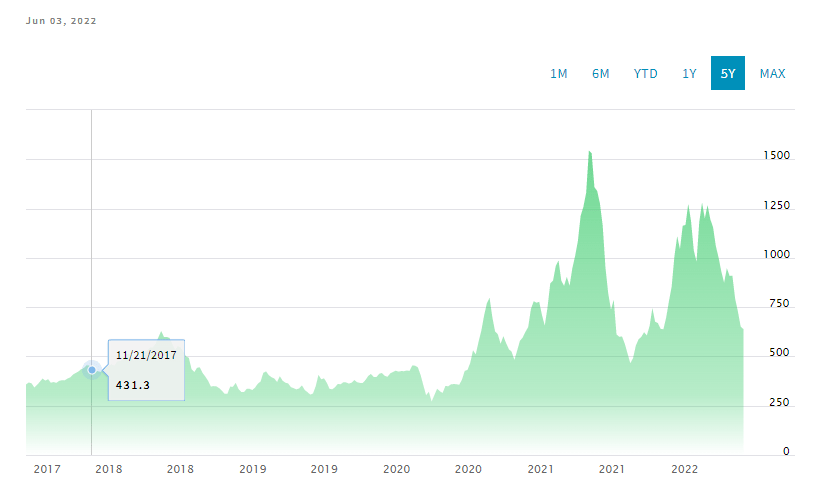

Lumber is in a bit of a different spot than other building products, even though we still think there’s a case for it having pent-up demand. The issue with lumber is that the part of the building cycle where lumber is most important has passed, indeed, right when you stopped hearing about all those lumber shortages. Lumber isn’t in a shortage right now, and that is well reflected in its price which has come down meaningfully from peaks.

Lumber Prices (Nasdaq)

In fact, mills have had to slow down because the real issue is in getting flatbed trucks to offtake the lumber. The shortage is no longer in mills or forests. Where does this leave companies like Interfor, which produces pretty much only lumber? Well, we think that if there is a housing shortage, and the current inventory is stuck at final stages before completion, it’s only a matter of time before that gets resolved and lumber is needed again. In fact, rising rates could actually help this happen sooner as goods trade declines and makes more flatbeds available. Therefore, there is possible pent-up demand for lumber. WFG also produces lumber, as well as OSB which is a little more processed and has been taking share away from regular plywood, constituting an additional secular trend in favour of that product in particular.

Interfor trades at 3x EBITDA, and WFG actually trades at the same value, which is probably why we’d prefer it. Since WFG also has OSB markets, that makes them slightly less commodified. They deserve a premium for that which they don’t currently have, which implies a 20% relative undervaluation. However, both Interfor and WFG are cheap in our view as when the building cycle restarts, that will be able to sustain lumber prices and volumes at least at the current levels for another couple of years. With the payback period on these investments being exactly that, only a couple of years given the multiples, we’re pretty happy with the valuation, where any better than expected outcome renders their valuations very flawed.

Bottom Line

Housing might be a bright spot in the US economy, even if rates rise. In fact, building product volumes, in particular, could even benefit from initially rising rates as it would free up logistics to help the building cycle move quicker as explained above.

However, there are clear risks. Many are right to be worried about the economy. Shortening credit is a scary prospect for the economy, and at some point, high enough rates could cause a deleveraging. If the ability to repay the large amount of debt accumulated by privates in these last years of low rates, the housing market will take a massive hit, and developers will certainly stop pushing to build houses.

So there is a sweet spot of interest rate hikes that will possibly help, or at least not hurt, these stocks. Not moving beyond that sweet spot will be helped by the return of the experience economy too, which should take pressure off the goods trade. But because you’re playing that game, these stocks should all be considered speculative. They aren’t far from all-time highs, and the market is pricing them as if they’re at the end of their cycles. If the economy is doomed to suffer a recession, then these multiples are probably quite correct. But even with recession risk, the multiples are low enough where every year of benefiting from the housing shortage meaningfully increases the safety of the investment at current prices.

Be the first to comment