tdub303

Dear readers/followers,

In this article, we’re going to take a closer look at Houlihan Lokey (NYSE:HLI), a somewhat under-covered and underappreciated financial company headquartered in Los Angeles. A reader of mine has worked with the bank in various ways, and wondered if I thought it worth investing in – so here’s my answer with regards to that.

Let’s look at what we have here, what makes Houlihan Lokey an interesting company – and what might make it an attractive investment.

Houlihan Lokey – What the company is and does

Houlihan Lokey is an interesting business. On paper, it’s a multinational investment bank and financial services company that was founded nearly 50 years back. On a high level, it’s not your standard IB/Brokerage – instead, its focus is on services higher on the scale, with things like M&As, capital market, restructuring services, distressed M&A’s, fairness consulting, and valuation advisory.

The company is essentially experts in a world of experts. HLI employs over 2,000 people across the world, and all of these work in a business that was founded by two PricewaterhouseCoopers employees.

The company has 35 worldwide locations and focuses on the extremely high expertise and tenure in management – a very insular sort of business, where you’ll need to work for a long time before climbing the ladder. The current average years of tenure for a manager in HLI is 33 years.

The company has annual revenues of around $2.3B and serves around 2,000 clients per year. From that revenue, it makes around $500M in EBIT.

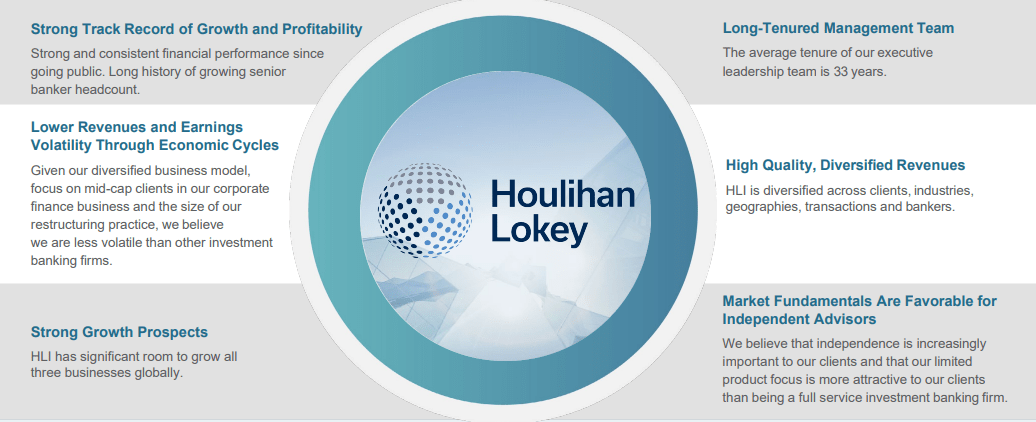

One of the primary arguments for investing in HLI is its strong track record, which really leaves very little to be desired.

HLI IR (HLI IR)

The world is increasingly favorable to companies such as these, which focus on being experts as opposed to being jacks of all trades. The same sort of trend can be observed not only in one sector but in sectors across the global business spectrum. Rather than being “masters of none”, companies are trying to focus on what they are becoming masters and experts of while divesting the rest. What I see is that companies can’t afford, in today’s globalized world, to be mediocre at one of their operations – it’s simply not profitable.

And Houlihan Lokey is a very profitable operation. Since 2017, the company has averaged EBIT growth of 27% CAGR, with revenues of 21% CAGR, meaning pre-tax income is growing faster than revenues. Margins have grown from 23.7% to nearly 30% in 2022, despite the way the market has been moving.

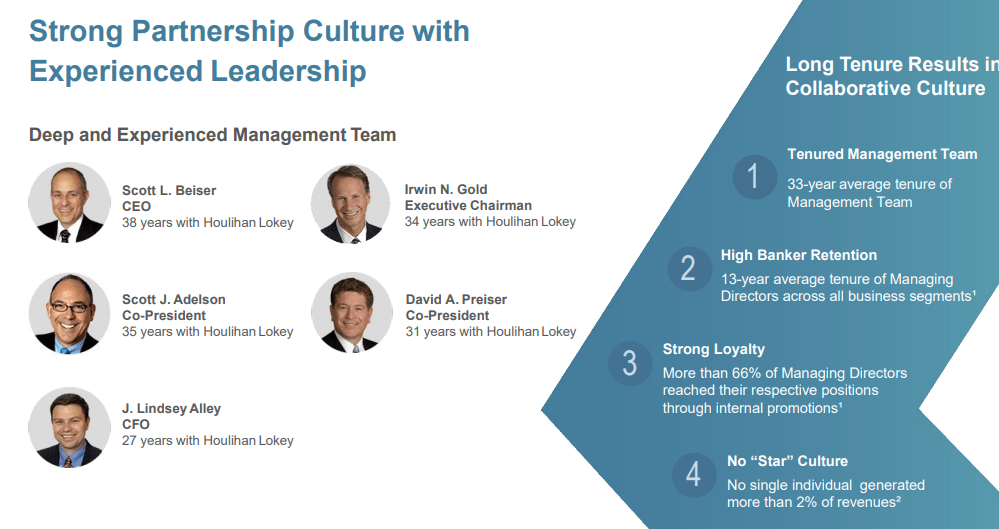

The company’s C-suite is brimming with experienced managers that have spent large periods of their lives walking the halls – it’s fair to say that for many, it’s the majority of their lives.

HLI IR (HLI IR)

I also like the fact that the company has a no-star culture, no “prestige” in its lines backed up by actual revenue numbers. Its retention numbers are sky-high, and its strong loyalty – all of these facts bespeak a company that promotes talent, loyalty, discipline, efficiency, and character. No company can grow as this one has grown without an internal code, and it’s clear even looking in from the outside, that this company has a great one – otherwise these numbers and these trends simply wouldn’t be as strong as they are.

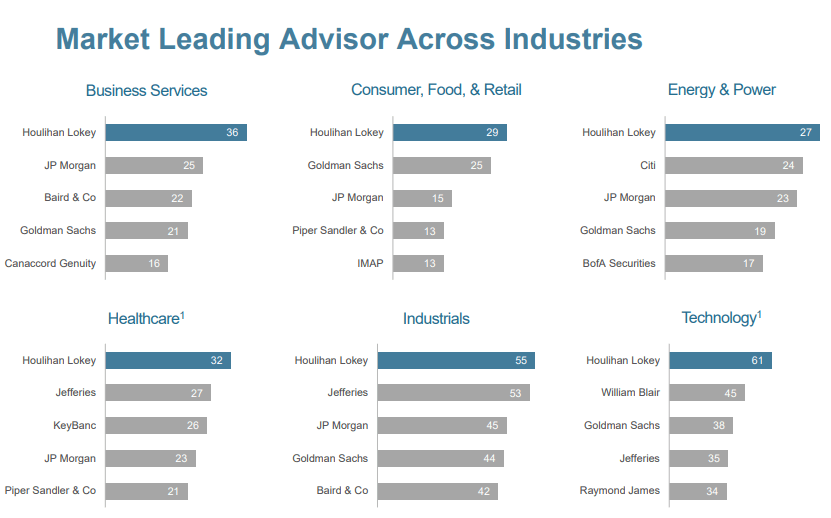

The fact is, Houlihan Lokey is a market leader. The company has extremely strong market positions in its expertise areas, being the top global:

- M&A Firm

- Restructuring Firm

- Fairness Opinion firm

As well as leading the market on advisory in every segment.

HLI IR (HLI IR)

The company has an appealing global client mix that trends towards private non-sponsor as well as other institutional, with 14% public and government-owned businesses. Its industry mix is extremely diversified, with no single segment accounting for more than 18%.

The only drawback is its mix could be said to be that HLI is very US-heavy – over 70% of the company’s revenue mix comes from the states, as well as being almost 70% corporate finance. That’s a bit of a weakness, but you can’t really carry that one “far”, because there are no real implications that the company is “suffering” as a result of this. Also, Houlihan Lokey has representation worldwide.

HLI IR (HLI IR)

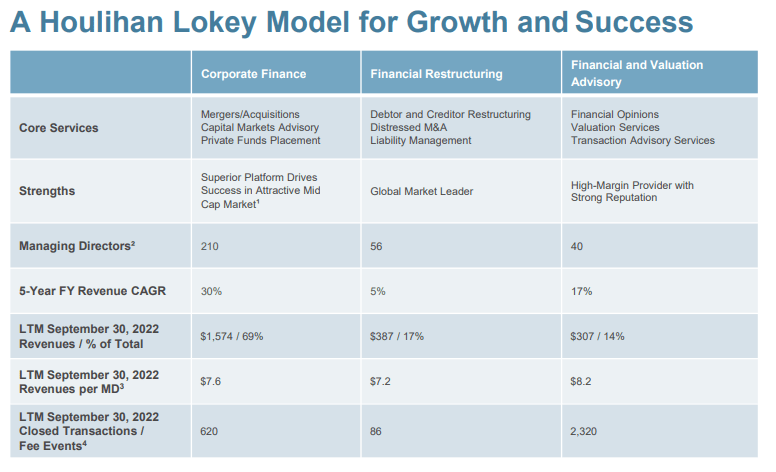

The company has been streamlining and concentrating its approach for years. The current managing director count is up 11% CAGR, which would usually be a red flag for me (being versed in organizational theory), but that is quickly rebutted by the fact that in the same timeframe, the average revenue per director is up more than 15% to nearly $8M on a per-directory basis.

HLI is an M&A-heavy grower, that expands its expertise through the use of inorganic growth. Simply put, the organization can be summarized into the following three segments which currently look something like this.

HLI IR (HLI IR)

It’s natural that the company’s deal flow and business volume tend to be somewhat heavily correlated with the shape of the broader market. For instance, during tech-heavy 2021, the company reached record revenues and volumes, with more than twice the amount of closed deals as the preceding years. However, this doesn’t mean that downturns bring fundamental issues – only normalization.

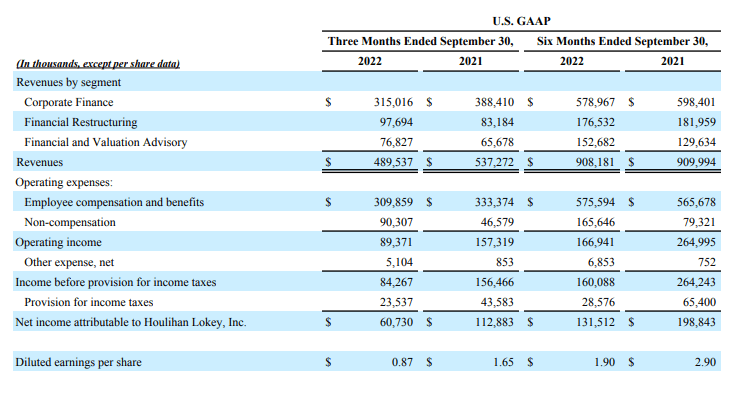

The company’s 2Q23 results are the latest ones we have, and while the company saw a downturn in overall revenues and net incomes compared to the 2021 period, this is to be taken on a comparative perspective while also considering what an outlier year 2021 was. Instead, I view 2Q23 as stable, with significant growth in financial restructuring and key segments in valuation advisory business arms, which are offsetting the downturn in corporate finance. For Financial and Valuation Advisory, the results were in fact the second-best quarter on record despite the downturn, and HLI is growing this business going forward.

The company is also seeing a reversion to the norm in its Corporate Finance segment, which promises that things should return to normal and growth at some point in the future.

The key question for me when looking through the filings and earnings of a company like HLI is…

HLI 3Q22 Press Release (HLI 3Q22 Press Release)

…is this company an attractive business with a fundamental upside?

To this, my answer would be a resounding “Yes!”. This is exactly the sort of business that I love investing in – a business run by, and managing competent experts in a field that’s needed. At the right valuation, this company shows every external sign (almost, at least) of being an investable sort of business. It grows its earnings, is a leader in its field, it has a dividend and a tradition in this field.

With regards to its credit rating, it doesn’t have an IG or any real credit rating I can find. However, I’m prepared to not put any sort of importance on this in this case – because Houlihan’s business is advising in exactly these sorts of matters, such as helping Grünenthal GmBH to refinance bank terms and revolvers through two bonds and a new revolver, with corresponding S&P and Moody’s ratings. (Source) The company, with less than 11% LT debt/Cap, also isn’t really in any sort of danger here.

HLI is also a significant dividend grower. It has more than doubled the size of its quarterly payout in less than 5 full years, and the future is bringing more increases to the table as well.

So from that, and most other perspectives, HLI is an extremely attractive business. Let’s look at the valuation of the company.

Houlihan Lokey Valuation

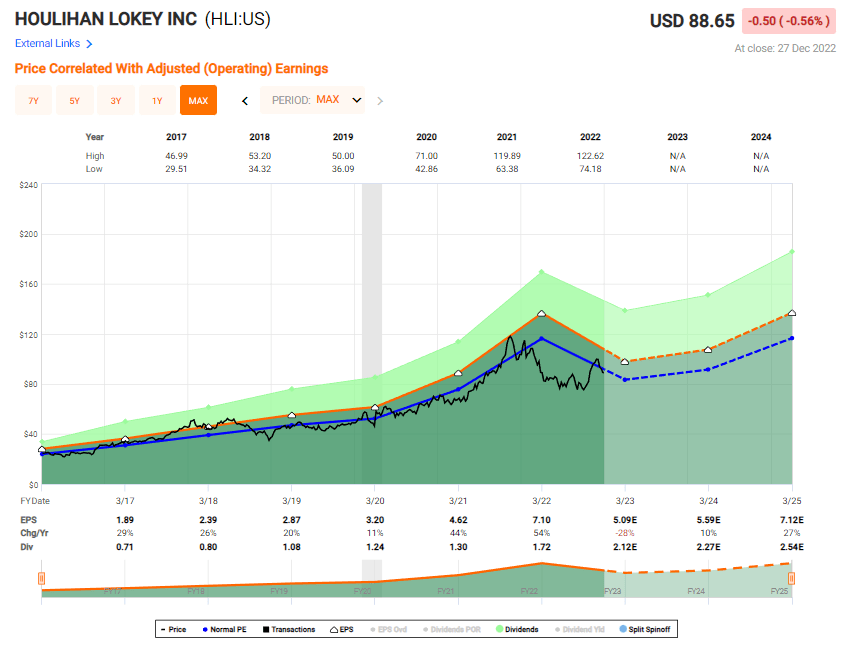

HLI commands an average valuation of between 16-18x P/E, owing to its very strong EPS growth rate of nearly 20% annually for the past 7-8 years. The company is volatile however and saw an extreme peak during 2021, from which it has and is currently dropping. For 2023 the estimates look like this.

HLI Valuation (F.A.S.T. Graphs)

The company is correlated to how the economy moves – so it’s natural to see this sort of trend, though I fully expect given recent results for the company to start reversing this trend in line with expectations. I do believe that what was once a 20% EPS Growth rate will go down to perhaps double digits at 10-15%. If we look at the 2022-2025 trend, the average EPS growth rate including the dip this year is around 3%, which puts into question how high we should value HLI here.

The company has traded as low as 12-13X P/E normalized, which is really when we should have started putting money to work in the company – but there could still be an upside to be had here.

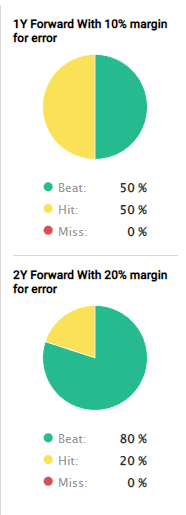

If the company were to normalize to expected trends, around 15-16x P/E for 2025, and those results materialize, which based on earnings forecast accuracy is more than just “quite likely”…

HLI analyst accuracy (F.A.S.T. Graphs)

…then that upside could be as high as 14-15% annually or 36.66% per year over the next 2-3 fiscals. Not a bad return in a market that’s expected to be pretty risky, all things considered.

Overall, I consider HLI to be an undoubtedly above-quality company. To my reader who asked regarding their investability, I can only say that I view HLI as very investable at the right price. So when is the right price?

I would say based on today’s forecasts, anything below an $80/share price makes this company a very attractive overall prospect. I forecast HLI to grow at least 12-14% per year once through its 2023 trough, and that’s going with the conservative estimates here. The company hasn’t been a good performer this year it’s down around 14.4% so far over the year, but this is still better than most indexes this year, and it’s led to some extremely interesting buying opportunities at great prices.

Current analyst estimates call for the company to trade between $77 at a low and $102 at a high, with an average of $91, implying a 2.8% upside at the current valuation. I would call that valuation a bit too high. While I could go for a long-term fair value estimate of around $85 based on forecasts, I choose to put my initial PT at around $80/share, at the conservative end of the forecast stick.

There are ways to invest in HLI that do give some other upsides – and I’ll show them to you, but for now, this is my initial thesis on Houlihan Lokey.

Thesis on Houlihan Lokey’s Common Share

- Houlihan Lokey is a market-leading expert in a field that demands the highest sort of financial expertise. The company has every hallmark of a qualitative, well-run, and sound business, making it a highly investable prospect at the right price.

- For me, that right price currently comes at a PT of $80 given the current share price and forecast trends, but also where the company is going from here.

- Based on these targets, I give HLI a “BUY” here with a slight upside.

Remember, I’m all about :

1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The options play

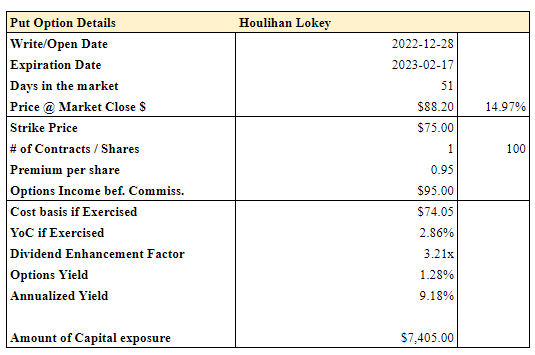

The possibility for an options play exists, which could put you in a better position to buy the company at a cheaper price while making some money regardless of how things go. This would require you to put buying power on the table though. This is a CSP I found for Houlihan Lokey today.

Options HLI (Author’s Data)

That data is pulled straight from the HLI options chain 10 minutes before market close, and that 9.18% annualized is attractive, even though the capital outlay is slightly higher than I would like for an option like this. I’ve not pulled the trigger on this one, but it’s a possibility in the near term if the premiums stay somewhere around this level or above.

These are the ways you could invest in HLI.

Be the first to comment