katleho Seisa

Thesis

I view background screening as a large and growing global market that has room for multiple winners, including HireRight Holdings Corporation (NYSE:HRT).HRT is one of the largest providers of background screening services, along with First Advantage (FA), Sterling Check (STER). I remain constructive on the company’s automation/digital transformation program, that I expect to result in a 500 bp lift to margins by FY24. The shares trade at a P/E multiple of 6x to my FY23 earnings estimate, setting up what I view as a highly favorable risk-reward given the strong demand backdrop and solid competitive positioning. My $22.4 price target is based on a P/E multiple of my 12x FY23 earning estimate.

Why do I like HRT?

Provider of Background Screening Services with a Focus on Highly Regulated Verticals

HRT is a global provider of background screening services that include job history/education verification, professional license verification, criminal background checks, and more. I view background screening as a large and growing global market, with a study by Stax estimating a TAM of ~$13 billion and a 6% CAGR. Based on the Stax study, HRT has a 6.4% market share, making it one of the largest companies in the space along with FA, followed by STER, which has an estimated 6.1% market share, as the industry’s third-largest player.

HRT specifically targets the background screening market by focusing on verticals such as transportation, healthcare, and technology, which tend to have large and global employee bases and high levels of regulation. While ~40% of revenue comes from these large verticals, no single customer contributes more than 3% of overall revenue, which I believe limits logo/customer concentration risk. I believe HRT’s vertical focus and penetration of a large and growing market puts the company in a strong position to generate healthy revenue growth over the next several years. In addition, the company also has a unique SMB offering (Backgroundchecks.com), which operates as a self-serve platform that individuals/SMBs can use to run background checks. While this SMB offering is still small (~4% of service revenue), I believe it is unique and could serve as an additional tailwind to long-term growth.

Digital Transformation Should Lead to Significant Margin Expansion

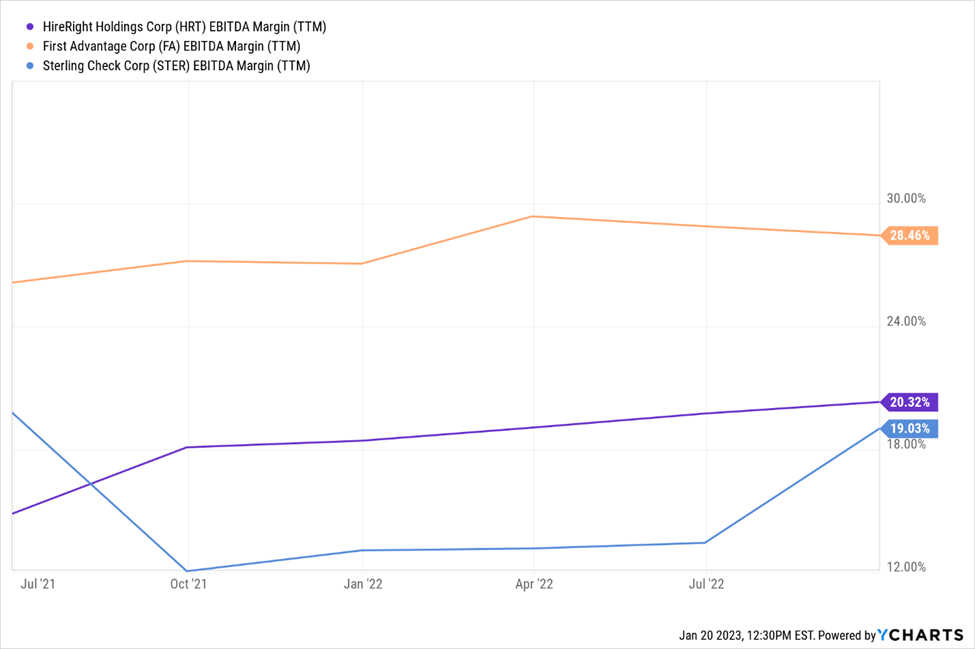

HRT’s EBITDA margin of 20.3% is solid, but below the industry-leading margins of its peer FA (28.4%). However, HRT is in the midst of a large digital transformation/automation program with a major IT services provider that is expected to boost its EBITDA margin by 500 bp by FY24. I view HRT as a multi-year margin expansion story and believe there could be further opportunities to expand margins in the coming years as the business grows. In the following chart, I have shown HRT’s improving EBITDA margin trajectory.

EBITDA Margins of HRT vs. Peers (Ycharts)

Leverage is coming down

Given its history as an acquisitive private equity-backed company, HRT has historically operated with a significant amount of leverage. Due to a combination of the IPO proceeds, organic EBITDA growth, and debt reduction, HRT reduced its net debt/EBITDA ratio to 11.1x at the end of 3Q22 from 22.5x one year earlier. I believe that the stability of HRT’s business model allows the company to operate comfortably with more leverage than companies with more volatile demand/revenue. However, I suspect that the current choppy financial market conditions result in companies with pristine balance sheets being viewed favorably by investors. Given these dynamics, I expect the shares to re-rate higher as the company reduces its balance sheet leverage.

Financial Outlook

HRT operates its business with two streams of revenue: Service revenue and Surcharge revenue. The surcharge fees are typically charged to customers at cost and dependent on the pricing from the third-party data providers. In 3Q22, surcharge revenue accounted for 28% of revenue. For the core service offering, customers order desired screening/monitoring records, and the revenue is recognized when HRT delivers the screening report to the customer.

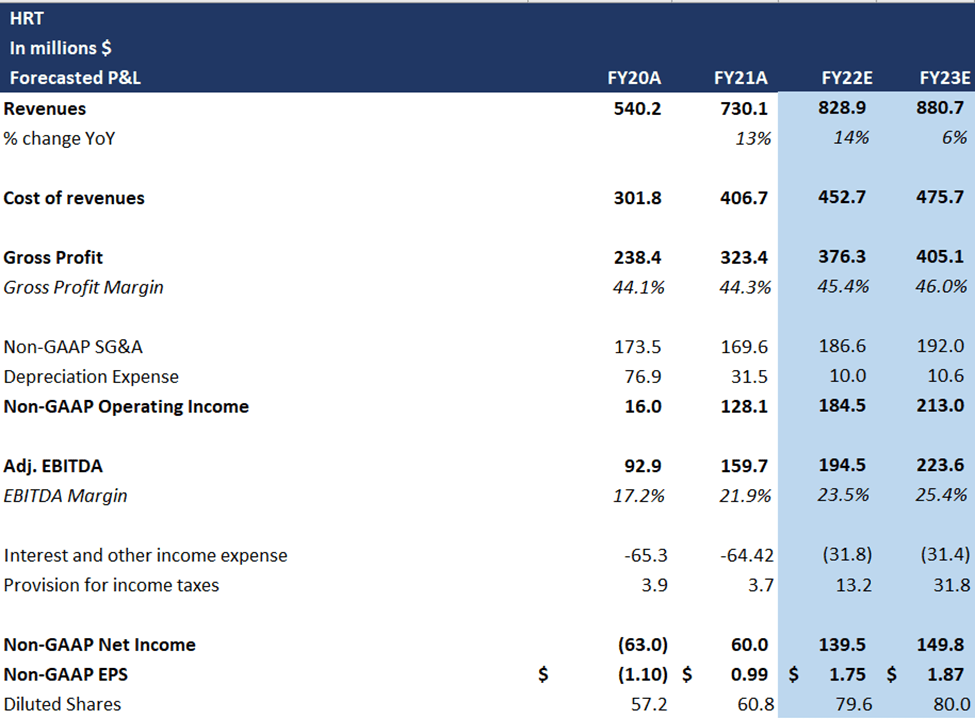

HRT’s EBITDA margin contracted meaningfully in FY20 due to a combination of pandemic-related impacts that weighed on revenue and a step-up in investments aimed at modernizing the platform to keep it competitive on a global scale. Margins bounced back in FY21 to 21.9%, up from 17.2% in FY20 and near pre-pandemic levels (22.6%). HRT recently brought in a major IT services provider to conduct a multiyear transformation project to accelerate the company’s automation efforts through implementing AI and machine learning capabilities, which I expect to serve as a key driver of HRT’s EBITDA margin expansion in the coming years.

HRT’s forecasted P&L (my estimates)

Discounted Valuation despite Strong Execution

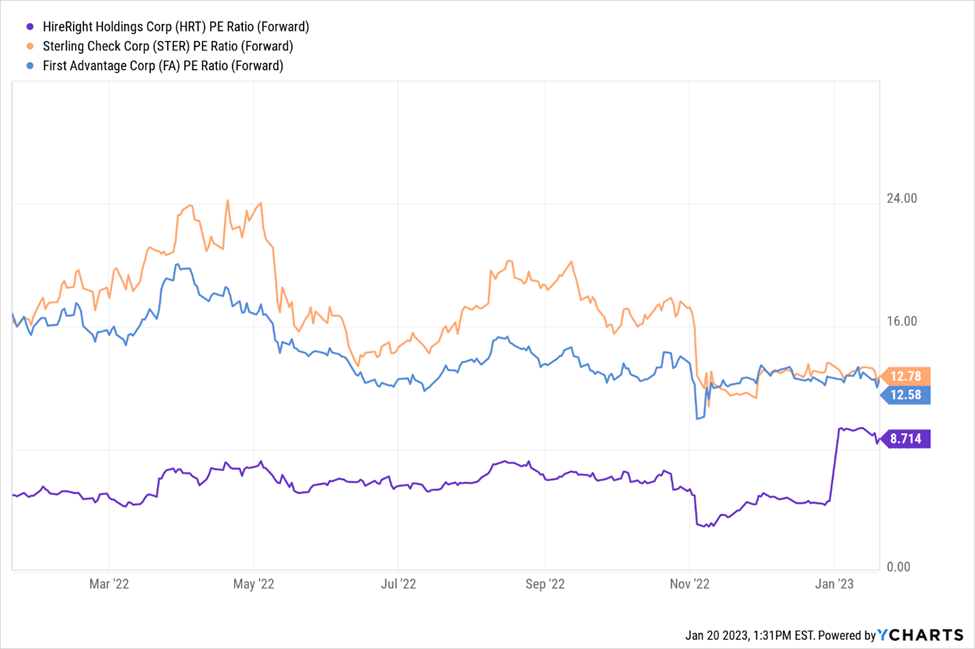

HRT trades at a P/E multiple of 6x of my FY23 earnings estimate, a discount to both STER and FA, and a sharp discount to a peer group of FinTech and information services companies. This comes in spite of HRT posting several impressive beat-and-raise quarters since the 2021 IPO. I believe the discount is due to HRT’s relatively short track record as a public company and lower margins compared to the other two public background screening peers. However, I believe there is a line of sight toward higher margins given the company’s digital transformation/automation efforts. I also believe that the entire background screening space could re-rate higher as investors get increasingly comfortable with the growth, cash flow, and durability of the business models through different points in the economic cycle. My $22.4 price target is based on a P/E multiple of my 12x FY23 estimate.

HRT’s forward P/E ratio vs. Peers (YCharts)

Risks

- A prolonged economic downturn could reduce job turnover in the labor market, reducing the demand for background screening services.

- Increased competition from other major players in the background screening market, such as Sterling Check, First Advantage, or Checkr could result in pricing pressure and/or share losses for HRT.

- HRT is in the midst of a significant digital transformation/automation program. Any delays or challenges in these efforts could prolong HRT’s ability to expand margins and weigh on the shares.

- HRT has a significant amount of debt, most of which carries floating rates. Rising interest rates would increase the interest burden and could pressure FCF and/or HRT’s ability to swiftly reduce leverage.

Final Thoughts

I believe HRT has established itself as a leading provider of global background screening services, focusing on highly regulated verticals such as financial services and healthcare. I am constructive on the global background screening market as a whole, given that the global pandemic and increased popularity/acceptance of remote working has increased job turnover, which should help the market continue to grow above historical levels, allowing HRT to combine solid organic growth with significant margin expansion for the next several years. I keep a price target of $22.4 on the company’s stock.

Be the first to comment