imaginima

Hess Midstream LP (NYSE:HESM) can be looked upon as an asset that Hess Corporation (HES), the parent company, has available as a source of cash should cash be needed by Hess. Obviously, for Hess Corporation, the main concentration is on Guyana, which appears to be by far the most profitable part of the company as well as a very fast-growing part. However, Hess Midstream is located in the Bakken. As such, it is part of the cash back-up system Hess has in place to make sure that the Guyana development keeps going.

Hess Midstream had announced earlier in the year a secondary offering by the backers of the company. The offering raised money solely for the backers who were selling shares. Hess Midstream floated $400 million of bonds to participate in the purchase of some units that would have been sold. It is a little complicated in that the noncontrolling interests needed to convert to the public shares in order to sell. Hess Midstream saved some of those interests that step. But the repurchase benefitted public holders because the additional float was lower while the relative interest of each share increased.

This was also met with a distribution increase that was larger than had been the case. The management of what is usually a situation that results in share price weakness for a while instead changed the narrative to a very positive situation that resulted in considerably less pricing weakness.

That appears to have been a hallmark of this midstream for some time. There is a sizable noncontrolling interest that in theory could lead to periodic pricing weaknesses as those shares come to market. But the backers of this midstream appear to know how to manage things to minimize periods of pricing weakness. That is highly unusual. But it has also been to the benefit of public shareholders.

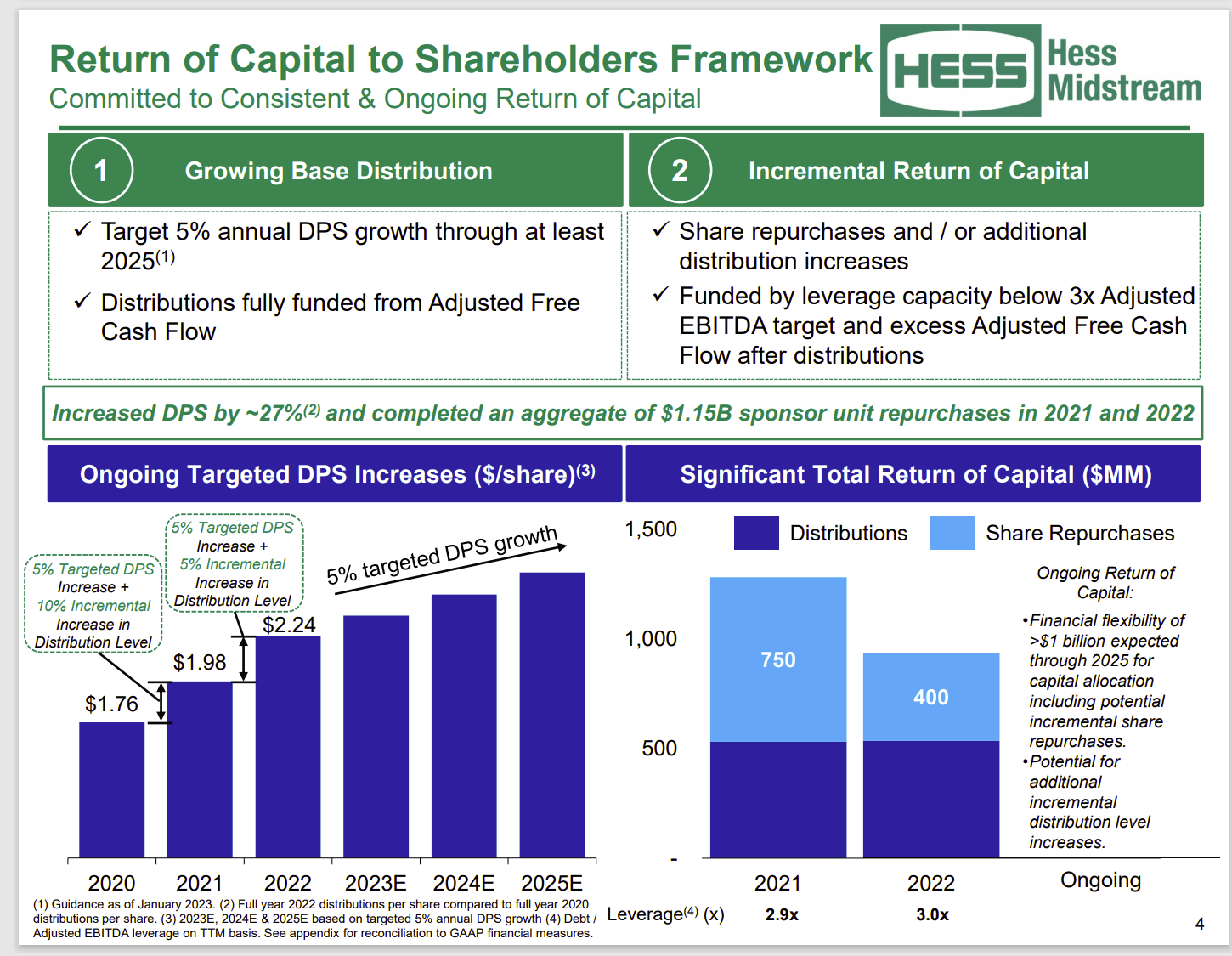

Hess Midstream Return Of Capital And Leverage Strategy (Hess Midstream January 2023, Corporate Presentation)

Management still has a targeted increase that would lead one to believe that the distribution raises that have come every quarter are going to continue into the future for the time being. The distribution is extremely well covered with a goal of more than 1.4. Actual fourth quarter coverage was 1.5 with a leverage of 3.0. The leverage shown above is one of the lowest for the midstream industry companies that I follow. What is even better is that the parent company, Hess Corporation, is investment grade. So, there are really no finance worries with this issue.

Hess has been growing the production in the Bakken to make sure there is a backup cash flow source if needed. That also means more business for Hess Midstream to service. The midstream has been growing business at a decent rate and that looks to continue for the foreseeable future.

The periodic repurchases of common aid the per unit growth. The low financial leverage assures a potential investor that the capacity exists for more purchases of common units in the future.

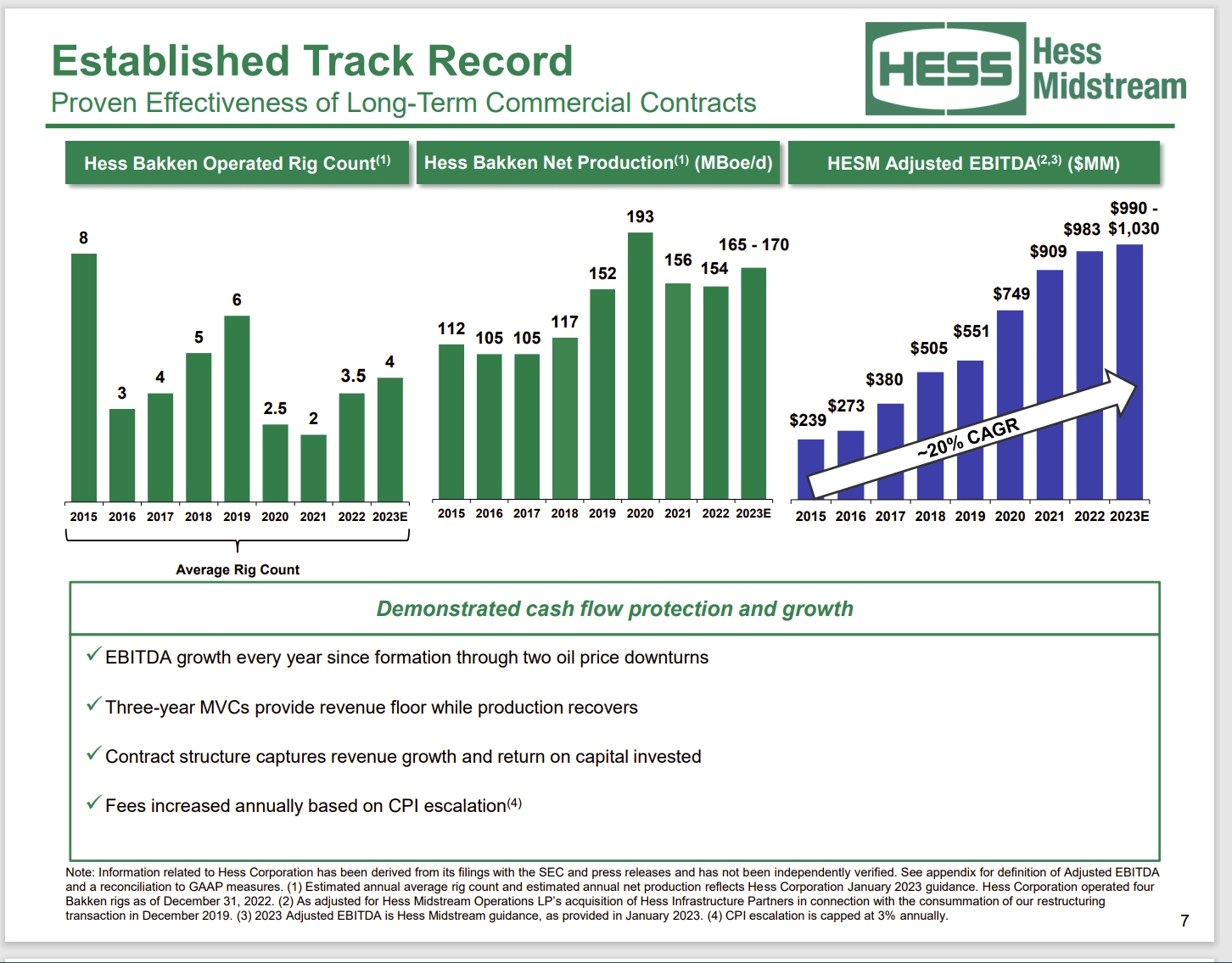

Hess Midstream Growth Record Throughout The Industry Cycle (Hess Midstream January 2023, Investor Presentation)

Hess Midstream, like many of these subsidiary midstream companies, does not service all the Hess acreage. It is therefore possible for the midstream company to continuously grow throughout the business cycle. Obviously, the goal is to lower costs for the total organization by way of that growth. In so doing, the midstream was able to grow right through the nasty 2020 downturn.

Midstream companies are normally fairly recession resistant. It is not unusual though for the common shares of midstream companies to follow upstream companies down during an upstream cyclical downturn even though this is a fee business with “take-or-pay” provisions. The market acts like the business is not as steady as it turns out to be.

Hess Midstream Connections To Long Haul Transportation To Customers (Hess Midstream January 2023, Investor Presentation)

The variety of connections is very important at this time. DAPL is operating with two revoked permits (or easements in one case which is a special permit). Both of those situations should be resolved in 2023. In the meantime, any good business has alternatives to cover for such an uncertainty no matter how insignificant some may think it is.

The alternatives allow the company to choose the best market for the price it receives from its production. Many companies I follow literally “dump the stuff” locally thinking that “what is the difference?” The difference is that from time to time, the companies with the ability to choose from several markets often rake in a little more money.

Hess will sell its excess transportation capacity from time to time. But for the time being there is considerable selling price flexibility that can come in handy.

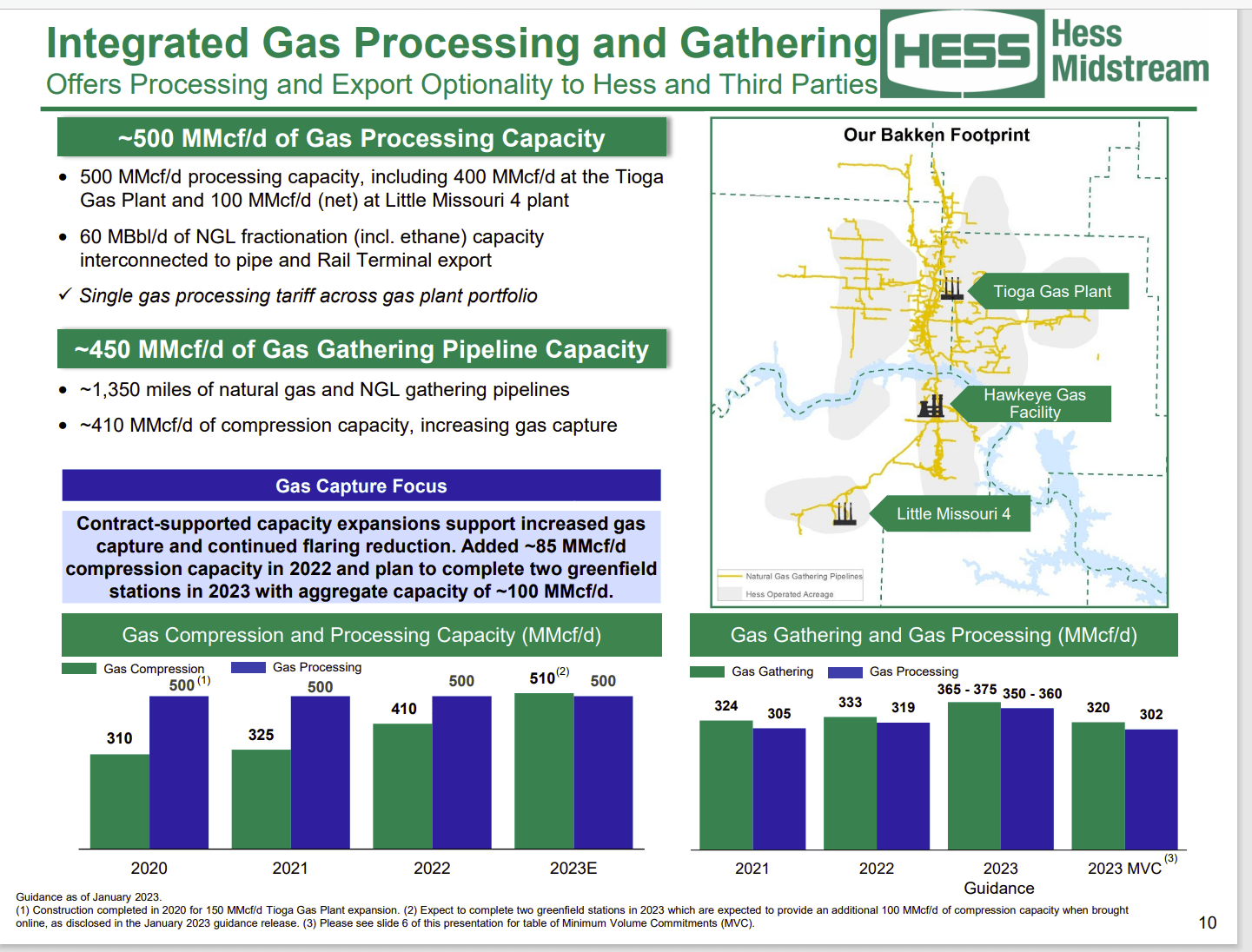

Natural Gas Processing

This midstream is a bit more integrated than is many in that it also has natural gas processing abilities. The abilities of fractionation and separating out different products from the natural gas stream are abilities usually seen at far larger midstream companies. This integration helps make this midstream very profitable.

This part, along with water distribution and transportation allows for considerable growth as more Hess acreage is covered by the midstream infrastructure. That continuing drive to cover more of Hess operations should enable midstream growth throughout the business cycle well into the future.

Oil gets a lot of the news coverage because it is the most valuable commodity produced. But the natural gas really appears to have had the most growth over the last several years and the water business is newer as well.

The Future

For as long as I have covered this midstream, it is rarely a bargain. However, it also generally outperforms the industry. So, it may be worth considering for an investment as a growth and income story. The company is likely to repurchase shares whenever there is a secondary offering.

Right now, Hess does not need the money. But the other partner may decide to sell shares from time to time.

The midstream has an extremely low debt level for the midstream industry. So, Hess Midstream can repurchase shares using debt should that be necessary. The well-covered dividend is likely to be raised every quarter at least through 2024. That combined with appreciation potential of the common should provide a return in the teens.

The midstream business is considered fairly low risk and a very steady business. This one has grown at an above average rate due to the need to service the Hess upstream business. It has also aided per share growth with periodic share repurchases. There is no sign of that growth rate slowing all that much at the current time.

Be the first to comment