lumenetumbra/iStock via Getty Images

While we are at the beginning of the lithium EV revolution, I feel (to some extent) as though many of the companies and choice property locations have been discovered.

This makes finding ultra-value lithium stocks difficult to find; some of the smaller plays like Neo Lithium (OTCQX:NTTHF) grew up and have been bought out. Lithium Americas (LAC) has evolved from an aggressive tadpole to a 2,664 pound shark, fueled by its partial ownership of Arena Minerals and acquisition of Millennial Lithium. Lake Resources (OTCQB:LLKKF) went from a scrappy 5-cent roll of the dice to a buck+ high flier. Could HeliosX Lithium & Technologies Corp (OTCQB:HXLTF) be a hidden sleeper? I think perhaps.

I enjoy looking at the small hopeful players; little guys who are not as well known and easily overlooked. Let’s explore a small (albeit risky) one:

HeliosX: A Risky (& Potentially Overlooked) Lithium & Gold Play

Dajin Lithium and HeliosX recently completed an amalgamation and fused into one company and thus HeliosX Lithium & Technologies Corp was created.

A recent video from late March sheds light on the entire company and is well worth your time to watch. Moving on.

I’ve been following Dajin since they were gold hunting in Canada during the mid 2000’s. Since then, they have added lithium and actually found a pretty good property in South America which we will cover later.

From 2018 until recent, things had been pretty quiet on all fronts for Dajin. One reason you did not hear much about them is because the financials were nothing to write home about. Frankly, it appeared as though they were hibernating and just waiting for partners to move forward with projects. This was somewhat dependent upon lithium prices. With lithium prices going plaid, I sense stirrings occurring within the merged entity.

Recent Events at HeliosX Lithium

Before we get into the various properties, we need to catch up on current company events so we have an idea of direction. Writing frankly, Dajin was challenged financially but had various lithium properties and deals in place that offered opportunity. Thus, a fusing of sorts took place between Dajin Lithium (with its lithium property) and HeliosX (which brings capital, lithium, and a potential gold tailings operation). The pairing of the two companies makes sense. HeliosX gets several potential deals and Dajin gains capital to advance deals via drilling (one might suppose).

A final point I failed to mention is the CEO of HeliosX (Christopher Brown) brings a background of oil & gas along with reservoir experience. We will look at management later, but first let us look at the various properties of HeliosX Lithium has.

HeliosX Has 5 Catalysts for Potential Success

HeliosX Lithium has five potential catalysts that may ignite the stock:

- The first is the South American Project

- Second is the Lilac project in Nevada at Alkali Lake

- This is followed by the third project – Teels March

- Fourth, HeliosX Lithium has lithium property in Canada at the very early stages of exploration

- Lastly, the fifth project is a gold recovery project in Canada

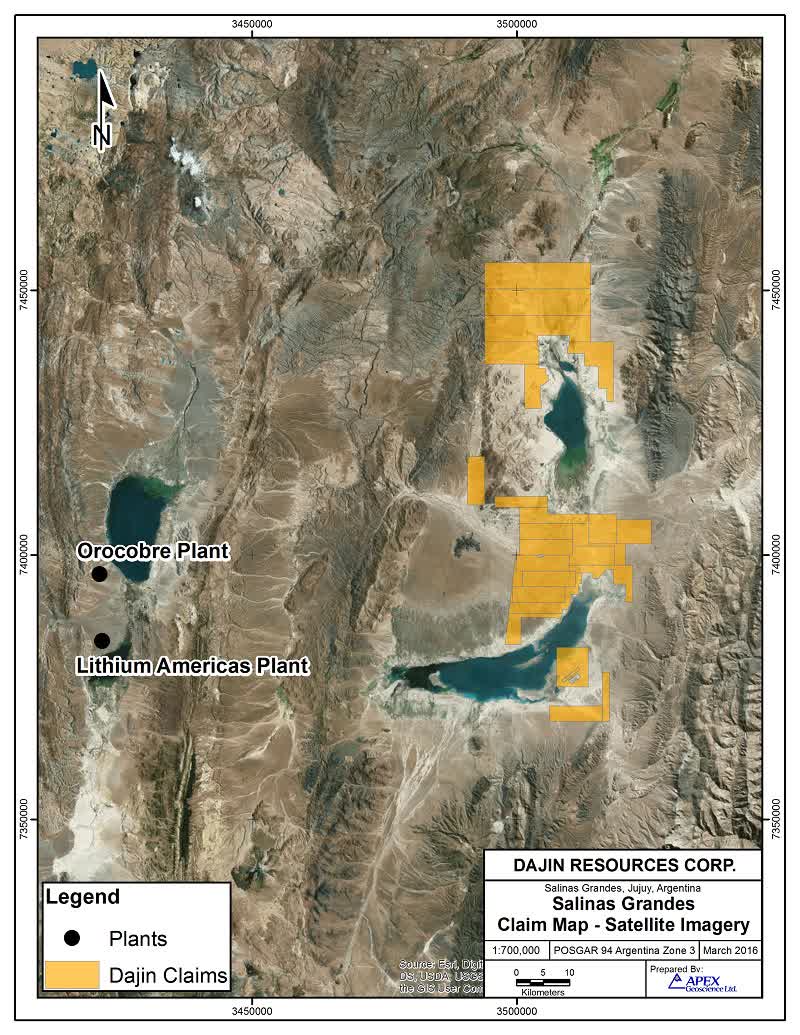

Project #1 – The Guayatoyoc/Salinas Grandes Salar

The crown jewel of all of HeliosX Lithium projects is arguably its lithium property in Argentina. I might even go as far as to call the project the keystone of the company.

Koch working with HeliosX Lithium

In a very surprising PR concerning Koch, the company said:

|

For those not tracking, Craig Brown helped set up Standard Lithium’s (SLI) DLE technology along with Cypress Development (OTCQB:CYDVF). Furthermore, Koch (Yes, the same Koch that funded Standard Lithium for $100 million a few months ago) is working with HeliosX.

One might speculate on where this relationship is leading, but I will leave that to the reader’s ponderings and imagination (given that Koch has billions available to invest). Give it additional thought though. It could be just simply a DLE push, but what if it evolved further?

The company goes on to state:

|

Various HeliosX lithium properties (Feb 2022 HeliosX Fact Sheet)

Background on the Guayatoyoc / Salinas Grandes Salar Project

HeliosX Lithium has partnered up with Pluspetrol to form Dajin Lithium S.A., of which Pluspetrol owns a 51% stake in the subsidiary, having spent $1.25 million CDN via an earn-in agreement along with paying Dajin Lithium $600,000 CDN.

Here is the official statement concerning that event and it is worth a read to garner more data on how Pluspetrol got into bed with Dajin (and hence HeliosX Lithium). It gives more detail on the percentages of the lithium grade. Do pay close attention to the percentages below. Often a company that is trying to mislead will push things such as listing the highest grade only while avoiding telling investors what the average grade is.

In our case, the company does a good job of letting us know 60% of the surface (key word) exploration was over 500 mg/l with 16% returning over 800 mg/l. Typically (from what I’ve been told), is that the deeper you go the better the odds of hitting higher grades.

|

Now it is interesting to note the property is rather immense at 230,000+ acres.

HeliosX Lithium SA Properties (HeliosX Lithium )

Yet, while size is impressive, how much of this property is valuable? This is a question where the answer will require further drilling. However, surface samples of brine did yield some results that evidently attracted Pluspetrol to dip its toe in the water. Next, let’s look at a second statement concerning the lithium grade.

|

The important note here is that on the low end, we are seeing 281 mg/l of lithium to 1,353 mg/l on the high end. Average grade is 591 mg/l.

I always pretty much throw the high end values out of my mind (as it can just be a fluke). The average values are more important and in this case they average 591 mg/l (which is more than acceptable for DLE extraction). The real question is when will Pluspetrol move forward on this project? Clearly they will have to drill more.

More, More, Moar, MOAR POWER!

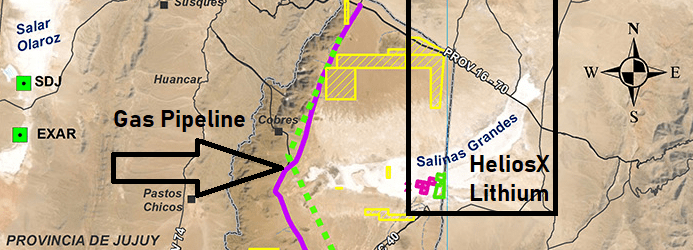

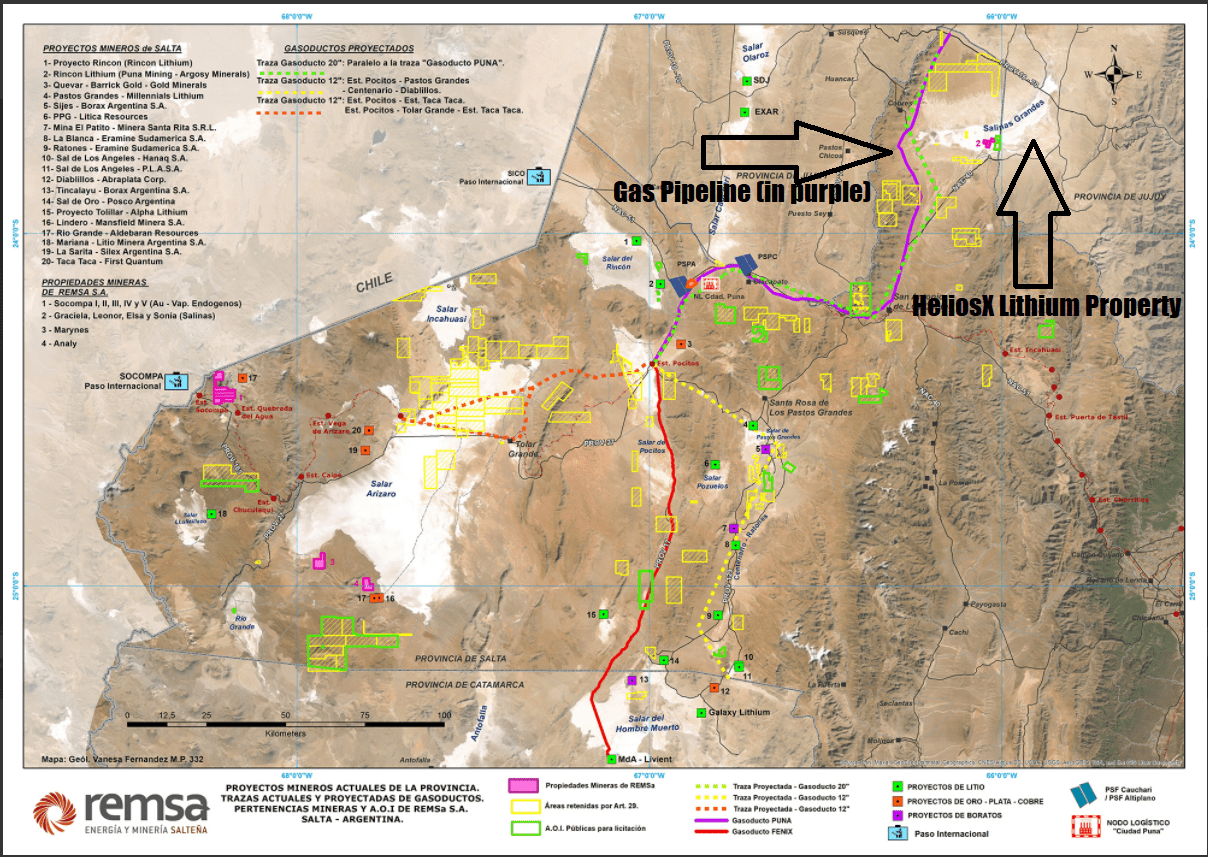

Any project requires power, be it from electrical lines, diesel generators, gas sources, geothermal, or solar. Of course, some of this presents logistical challenges if you are in the middle of nowhere or at extreme elevations. HeliosX Lithium, however, appears to have a large gas line just to the west of the property and they have road access.

Gas Pipeline near HeliosX Lithium (Remsa)

(Note: Black graphics are the authors, the property outline is a rough outline.)

Looking at the map above, we see the purple line is the PUNA gas line. To the right of that we see the Salinas Grandes salar where HeliosX will be working and if we look at the below graphic we can see legends if we expand it or you can see the source via this link if you scroll down.

Gas Overview (Remsa)

(Note: Black graphics are the authors)

Road Access

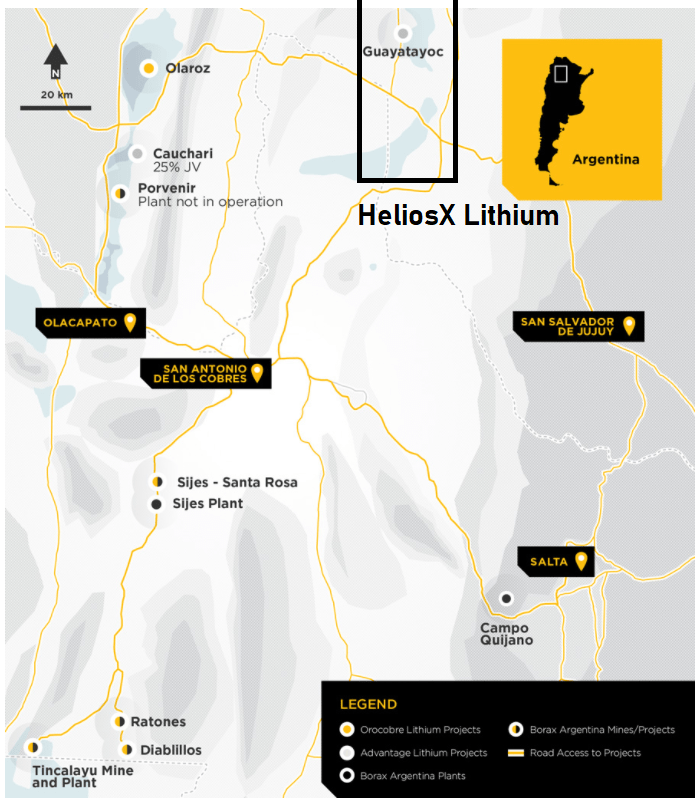

While power is critical so is road access. It appears this should not be a problem per the yellow colored roads on the below map.

Road access to HeliosX Lithium (Orocobre )

(Note: Black property rough outline is the authors)

Given the massive scope of the property, it seems that the real crux is determining the optimal places to extract lithium while simultaneously discerning which communities are supportive and which might be hostile. Another point to consider is that Pluspetrol (via Litica Resources) has a plethora of properties under its belt (per the below graphic). How much priority do they give this one project? How does it stack up compared to other projects on grade of lithium and total cost to bring the project to reality? This is where a drilling program has to come in and a feasibility study has to reach its conclusion.

Litica Resources via Pluspetrol properties (Pluspetrol)

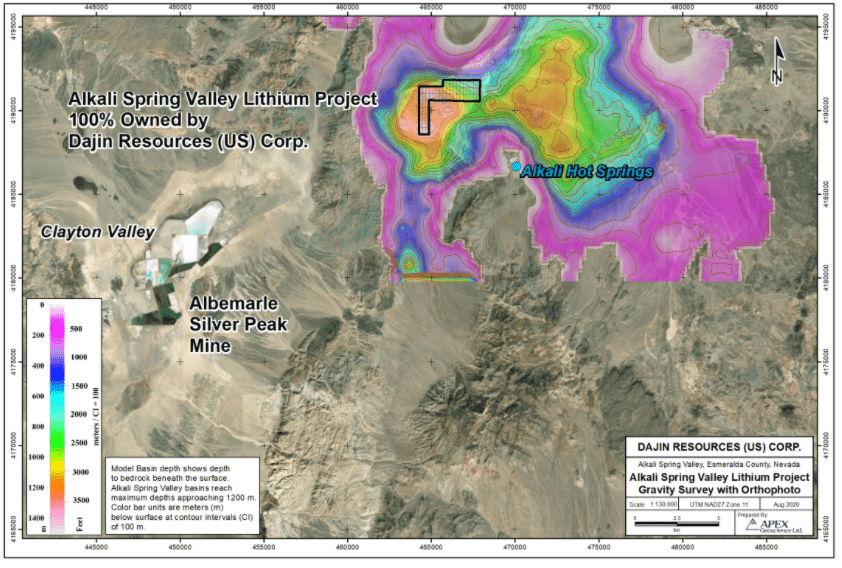

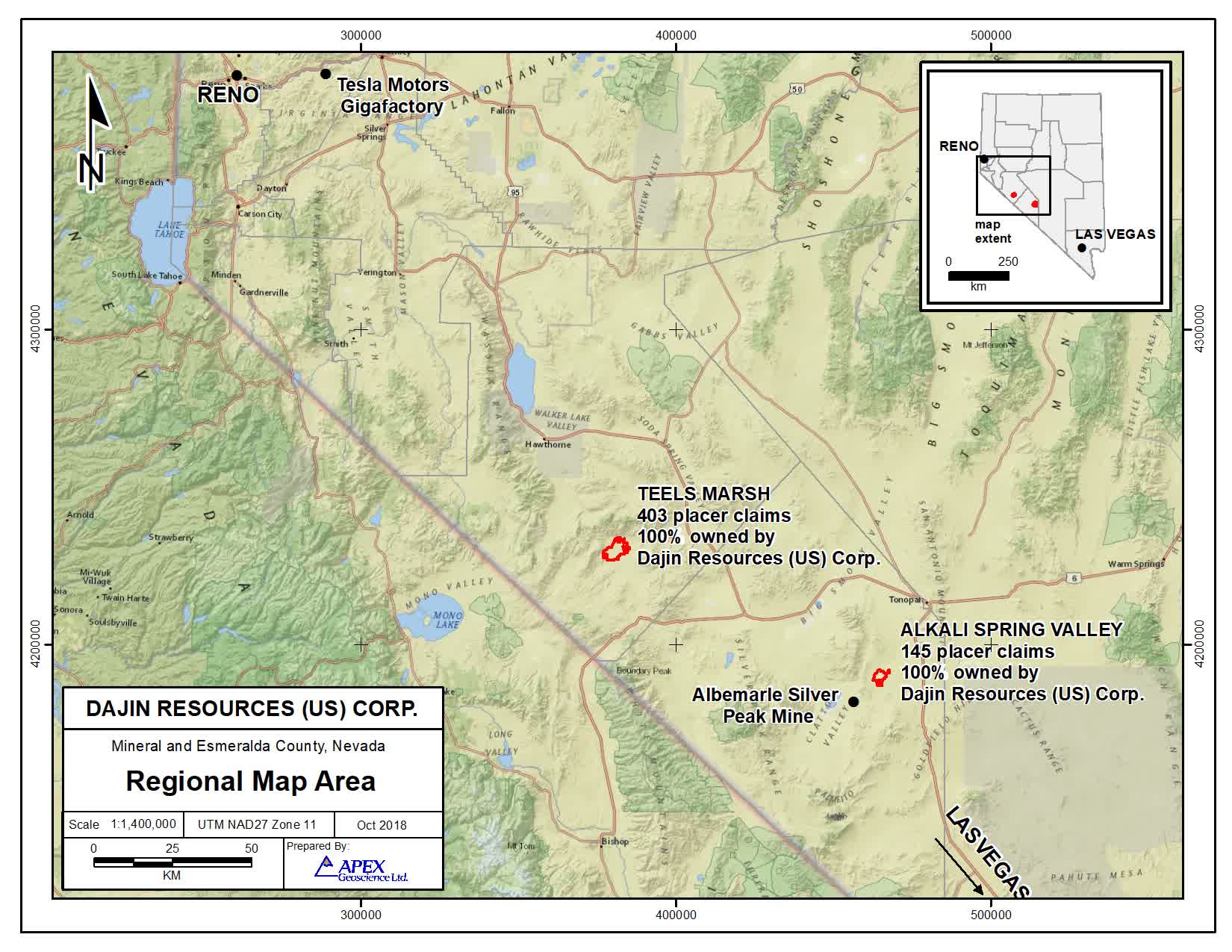

Project #2 – Alkali Lake & Liliac Solutions

Located 7 miles northeast of Albemarle’s silver peak mine, Lilac Solutions (via affiliate Lone Mountain Resources) has signed a deal as of Nov 10, 2020 for an earn-in on the 1,240 acres of Alkali Lake.

Alkali Lake (HeliosX Lithium)

Looking at this gravity model, the first thing that strikes me is why they do not have additional land to the east. Well, perhaps the company answers this via:

|

If HeliosX Lithium has detected lithium on the western basin, one might assume no lithium was detected on the eastern basin and hence they did not stake that land.

Lilac Solutions

Glancing at Lilac Solutions, we see they have been quite busy having just raised $150 million as of October 6, 2021 (after having raised an additional $20 million the prior year).

Now Lilac is all over the world working with various lithium companies to include Lake Resources (OTCQB:LLKKF), but HeliosX Lithium has been given a well notification by Lilac Solutions. Lilac has until August to meet the terms in order to earn 75% of the project. If they do not, then they forfeit the rights to the earn-in. Hence we see Lilac moving forward with plans to drill the property to meet the terms in order to earn the 75%.

Per the company:

|

Alkali / Teels Marsh Lithium Properties (Heliosx.ca)

I do question how this plays out concerning water rights for Alkali Lake, but I suppose richer pockets can figure it out (or we will learn more as things advance). Currently the project does not have water rights, but it appears the valley is not locked up like Clayton Valley. Hence obtaining water rights here may be possible unlike Clayton Valley that is over subscribed. Only three companies in Clayton Valley have any water: Albemarle, Cypress Development, and a gold company.

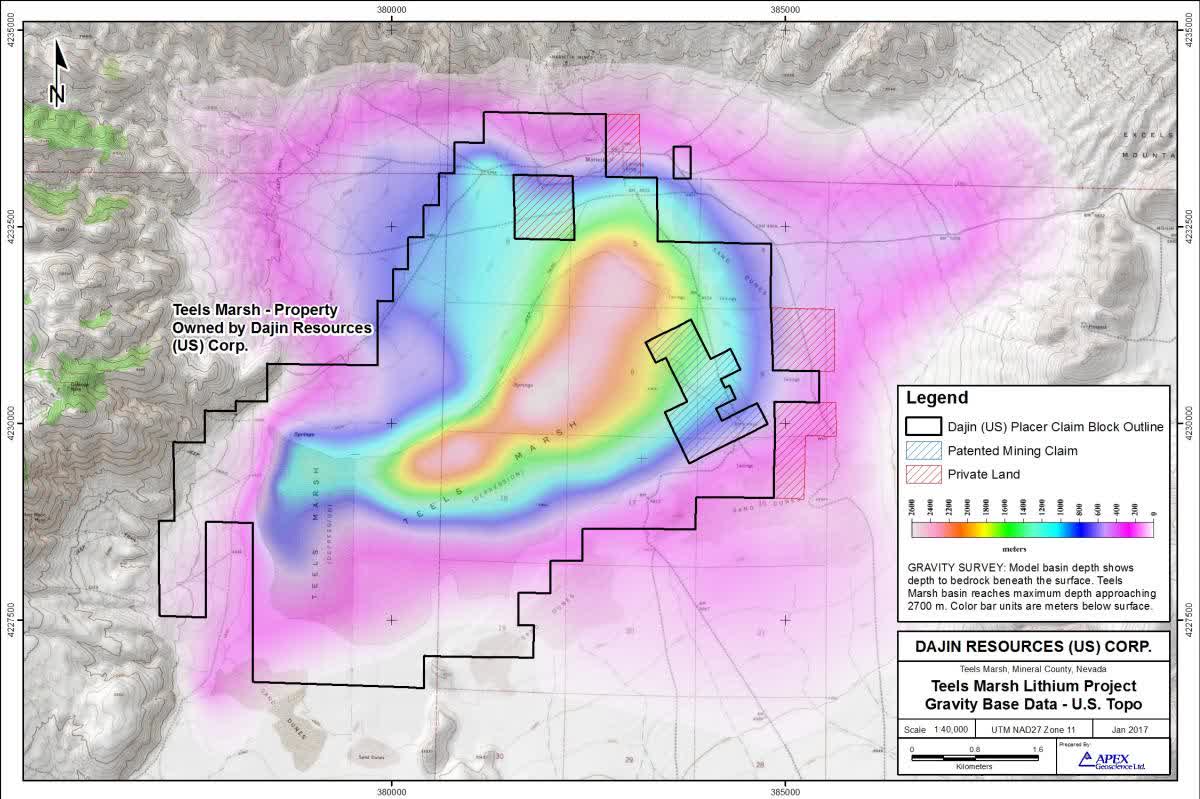

Project #3 Teels Marsh

Teels Marsh at 7,414 acres is a wildcard and I find it very intriguing as it is the most mysterious of the bunch. On one side, you have water rights granted and the project is 100% owned by HeliosX Lithium.

Per the 43-103 from Feb 2022.

|

On the other side, at first glance, the surface analysis is only a mere 79mg/l of lithium. Simply not impressive, but it might hint that a deposit is lurking under the surface. The basin is about 2.5 kilometers deep (8,200 ft). Put in miles, this is 1.55 miles deep. That is quite the depression and what lithium lurks under that ground?

Teels Marsh – Gravity model basin depth (Heliosx.ca)

In talking to various industry insiders, it has been explained to me that deep basins are associated with possibly having higher lithium concentrations (as you go deeper) as opposed to super shallow basins where the lithium laced water did not sink downward over the course of millions of years of erosion.

Instead, shallow basins push the water over the surface covering a wide area. I am no geologist, so I cannot personally confirm that statement; yet at 2.5 kilometers deep it appears the company is going to explore and see what that deep basin might yield (or not yield). Per HeliosX Lithium:

|

It is interesting to note in the 43-103 Feb 2022 talks about Albemarle’s (ALB) Silver Peak operation and how it did not initially display good surface readings of lithium either (till they drilled deep).

|

(Source: 43-103 Feb-2022)

Geothermal reading are mentioned which obviously could translate to energy for the project. Getting back to the topic of lithium value, I find it very interesting to note that southern neighbor Surge Battery Metals (OTCPK:NILIF) announced the following from January 2022:

|

Now the key word to note is the “up to” phrase. Typically, I look down on such phrases but on the flip side detecting “up to” 500 ppm of Li from a geothermal asset does make me wonder what is lurking under that property. Given that surge is on the fringes of the property from a gravity depression standpoint (aka not optimal property), it makes me wonder what the deepest parts look like lithium wise. This could be a real undiscovered gem or a total dud. Only drilling will determine if my theories prove correct. Per the March 29 conference, HeliosX is working on permitting to drill this year or 2023.

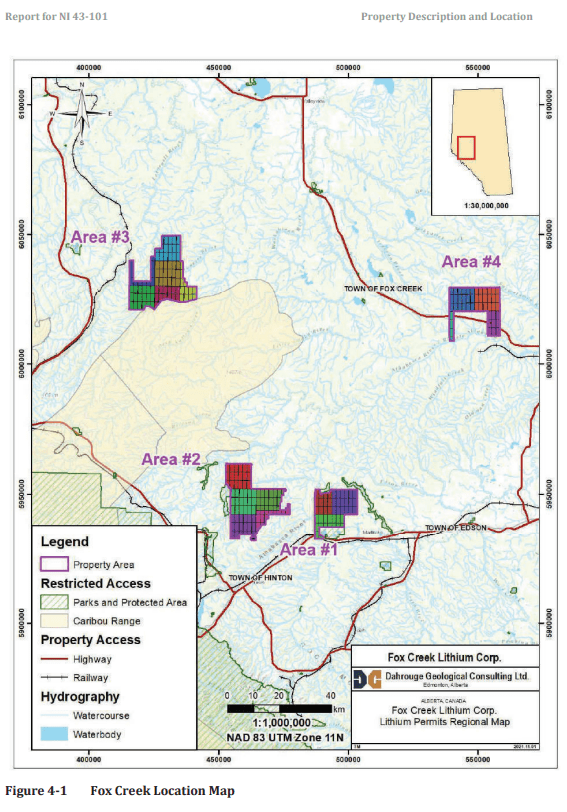

Project #4 – Fox Creek Lithium Project

The fourth project is the Fox Creek Lithium project. Per HeliosX Lithium:

|

Fox Creek Lithium Project (HeliosX)

Looking at the lithium in the illustration above, we can see the company has four potential locations for lithium extraction. I’ll explore and share more about this project in a future article.

Project #5 – Gold Recovery in Canada

Lastly, HeliosX Lithium has a gold recovery play in Canada and a letter of intent has been signed:

|

The question at hand would be how will the company finance the operations? For the various lithium plays where partnerships exist (Lilac in Nevada, PlusPetro in South America, and mayhap Koch is getting involved with the South American property — financing comes from the partnership. For the gold play one might venture whomever is agreeing to provide feedstock from waste tailings might be interested in providing funding. It would be logical after all if I can get additional capital from my waste tailings then why not fund that operation if the capital costs make sense?

Hence some potential paths are visible to push projects forward given the restricted capital available.

Politics & Lithium

Love politics or hate politics, the fact is politics can go a long way to giving a project the green light to go or deep sixing a project to development hell. Thankfully, the HeliosX Lithium South American play is located in mining friendly Argentina as opposed to Chile.

Per HeliosX Lithium:

|

(Source: HeliosX Lithium PR)

Expanding upon politics, if any reader has investments parked in Chile then realize this: Some socialists in Chile are trying to nationalize copper and lithium. Will it pass or not? I do not know, but it does not hurt to be aware of this for situational awareness. Further reading can be found here on the topic. Also Per this article, Chile is the largest producer of lithium. Lastly, it appears that the rational old-guard in Chile is pushing back against running lithium investments from the country. Thankfully, HeliosX Lithium has no investments in Chile.

Risk

To quote the late Steve Irwin “Danger, Danger… Danger”.

Each individual investor has a different tolerance towards danger. Some people can handle an extreme amount of risk (such as myself). Others are better off in bonds. Humorously enough, I have a cousin that drives high-end sports cars at speeds that cheat death. Yet, when it comes to stocks, he will not buy anything because he is not a “gambler”. To each his own.

The smaller lithium plays often come with extreme risk, from lack of capitalization and questionable management, to having zero experience outside of finance. Additionally, in some of the microcap plays, one will see assets that frankly are just borderline — be it low lithium grades or assets that have a multitude of problems ranging from locals (A rancher at Thacker Pass via LAC) to birds roosting in a the salar.

The point is know what you are comfortable with and know what you are getting into. More so, know how much capital to put into a gamble. I see people over betting all the time. It is one thing to place a small bet on something questionable that might play out in spades. It is another thing to bet the farm on a speculative stock and be chock-full of Hopium.

In the Land of Lithium Dreams

HeliosX Lithium is a gamble: The market cap is low and the total cash (while notable at $1.5 million CDN as of Feb 9, 2022) simply has to be improved. This might happen via the various partnerships in place. (Koch comes to mind.) If Koch can fund Standard Lithium (SLI) for $100 million and they have some relationship with the HeliosX Lithium Canada asset — might one dream we see something evolve from this? Maybe, one is, after all, allowed to wistfully dream. However returning to reality and risk, the limited cash is something investors need to take notice of. Yet with CEO Chris Brown at the helm (along with his engineering and financial background), I think he can unearth the path to success.

Playing the devil’s advocate, let us pretend for a moment that even with exploding lithium prices and partnerships project funding does not pan out. What happens? Well, you lose your money on this bet and that is why you do not put all of your eggs in one basket. This is not to say you can’t bet with conviction. This is not to say you can’t bet hard, but no bet should equal “game over” for you. Young grasshoppers take oversized risk or chase hot items too frequently. Old cantankerous veterans have learned the hard way that proper risk management is far more important than chasing that maximum outcome. Hence, be careful. Now, moving back to my biased viewpoint.

HeliosX Lithium Management Has Real World Experience

When I look at HeliosX Lithium, I see management has actual real world experience. Typically when glancing at lithium companies, I prefer CEO’s who have operational experience in mining. This is not to say this is always the case. Some outstanding CEO’s are present whose background is more financial in nature, but I still prefer those with an engineering background. In this case, Chris Brown fits the bill, but in a well rounded way. One might even call him a cross-breed (being that he has both a financial and an engineering background).

We can see from his LinkedIn profile that he got his start as a reservoir engineer (after obtaining a chemical engineering degree) back in 1994, before moving on to other resource companies for 11 years. He was then in a financial analyst role for 11 years before making his return to the management / engineering side of the house with HeliosX. While here, he managed reservoirs before merging with Dajin Lithium. This makes him well rounded in my book because he can think like an engineer and yet he understands the needs of the capital markets.

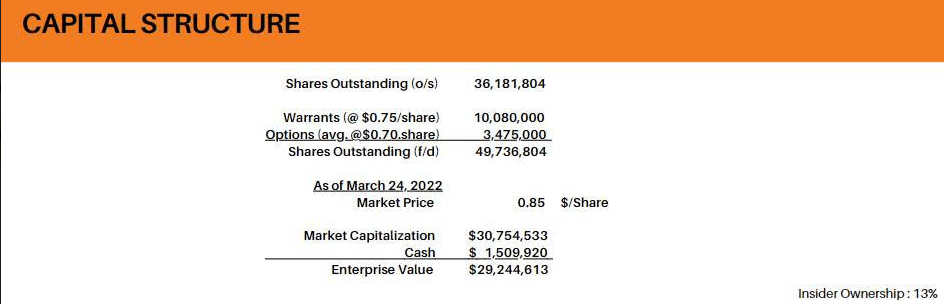

Financials

HeliosX Lithium only has $1.5 million CDN and that is not a massive bankroll. Yet, as a minority holder of some projects, in a sense they can afford to just sit back and wait. As lithium prices continue to blast off, this only makes projects appear more favorable. I would like to see more capital raises, but they need to get the share price up before that happens. The 13% insider ownership also needs to be noted.

Capital Structure – March 2022 (HeliosX Lithium)

Realize that companies that have smaller bank rolls obviously have less room for error. Frankly, all HeliosX has to do is keep playing the waiting game. As the price of lithium continues to rise, Lady Luck shifts more and more in their favor. This is not a stock for those that have the slightest amount of risk aversion. While you could make good returns if plans pan out, you could also lose all of your speculated money. Caveat emptor comes to mind. Now that I have scared some sense into most people, let’s look at some big picture catalysts impacting lithium.

Big Picture Lithium & Demand Catalysts

- Unconfirmed reports place Ford at investing $40-$50 billion in EV.

- A Porsche Taycan goes coast to coast on 2.5 hours of charging.

- Firestone offers charging stations.

- LG Energy to spend $1.7 billion on battery factory in the US.

- Glencore & Britishvolt to build lithium / cobalt recycling plant in the U.K.

- US Gov to put $5 billion into EV chargers nationwide over five years. An additional $2.5 billion will be released later on. (Total $7.5 billion)

- EV models will double by 2024.

- Pentagon to stockpile rare earths (includes lithium).

- Mississippi snags a $500 million Nissan EV plant.

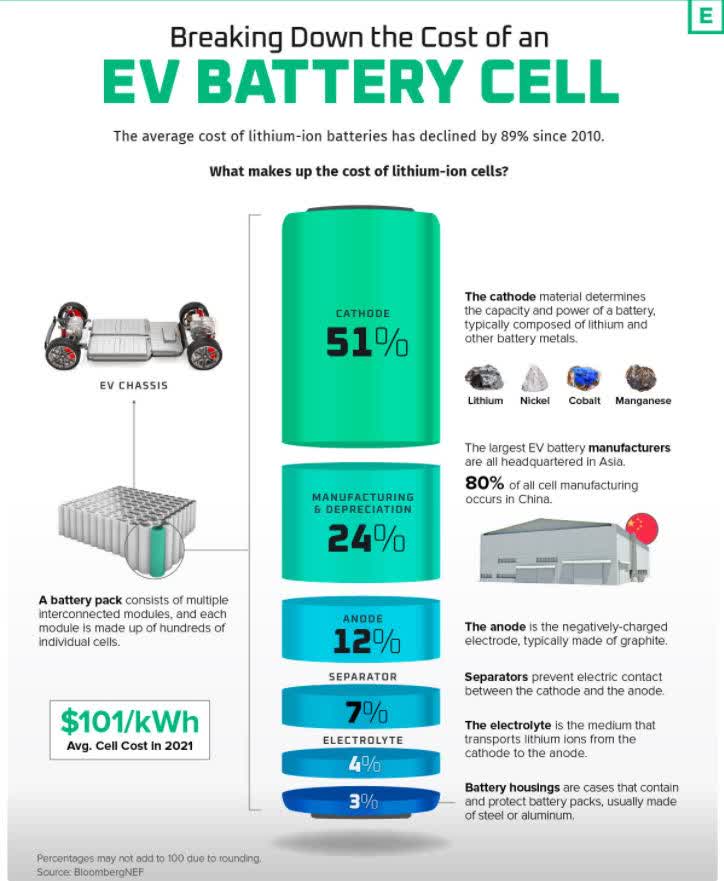

A Side Note

Last, as a side note, I’m including the following graphic below. I found the breakdown to be rather interesting. Note the cathode (lithium) make up at 51% as opposed to Anode (graphite) at 12%.

Battery material makeup (BloombergNEF)

Conclusion

HeliosX Lithium (in my opinion) is one of the more intriguing wild card lithium plays. Granted 2022-2023 looks like the company focus is going to be on developing a project via drilling and PEA studies. I suspect along the way we will see controlling partners move forward with projects via funding. Realize these projects will take years to fully pan out if ever.

Given the low market cap, I am building out quite the position in this gamble. Make no mistake: This is a gamble after all. The company is clearly capital constrained, but on the flip side they have partners that own 75% of one of the Nevada projects and 51% of the South American project. This puts the burden of development (and control of the project) upon the majority interest partner. With deep partnerships and management that understands engineering, along with the capital markets, I think this is worth my hard earned money. This company is a gamble. Yet given lithium prices, demand, and the various partnerships I am willing to incur extreme risk as the risk to reward makes sense.

Kudos

I would like to thank Uncle Rico for pointing me down the right path concerning the gas lines. Finding this data took me quite a while to hunt down and a second friend confirmed the data. It was very appreciated from both of you. I’m sure the readers will appreciate it as well. This article has frankly taken me weeks if not months of research. It will not appear that way when you the reader ponder it though. Yet it is a labor of love.

Caveat Lector – Let the Reader Beware

This article is not financial advice. I am biased and I think the company will be successful. This does not mean that my assessment will actually come true. Consult a financial advisor for guidance. Those with risk aversion need to avoid this stock as the risk level is extreme given the limited capital.

Be the first to comment