SrdjanPav/E+ via Getty Images

Haleon plc (NYSE:HLN) is a leader in consumer healthcare products through a well-recognized brand portfolio that includes “Advil”, “Theraflu”, “Robitussin”, “Excedrin”, “Centrum”, “TUMS”, and “Sensodyne” among others. Shares began trading as an independent company in July following the completion of its spin-off from GSK plc (GSK) while Pfizer Inc (PFE) is also a minority shareholder.

The stock as a pure play on this segment that captures global exposure to trends in climbing demand for oral health, and over-the-counter medications with a multi-channel distribution strategy. Haleon is profitable with an expectation that recurring free cash flow will translate into regular dividend initiation by next year and annual increases going forward. HLN has sold off in recent weeks and we are bullish here with a sense that the stock is undervalued and well-positioned to climb higher.

source: company IR

GSK-Haleon Spin-Off

Haleon went through an evolution over the past decade, originally as a unit within Novartis AG (NVS) before it was acquired by Glaxo Smith Klein in 2018. Another milestone came in 2019 when GSK formed a joint venture with Pfizer to combine their consumer healthcare segments. Over the years, the group exited certain categories related to skincare and other non-core products. GSK chose to spinoff Haleon to better focus on its vaccine business.

With the transaction, GSK shareholders received one share in the new company for each share owned. Following the deal, GSK shareholders controlled approximately 54.5% of the new Haleon directly while the corporate entity maintained a 13.5% stake. Separately, Pfizer now holds approximately 32% of HLN although it is expected they will exit the position per a statement on page 75 of the registration filing.

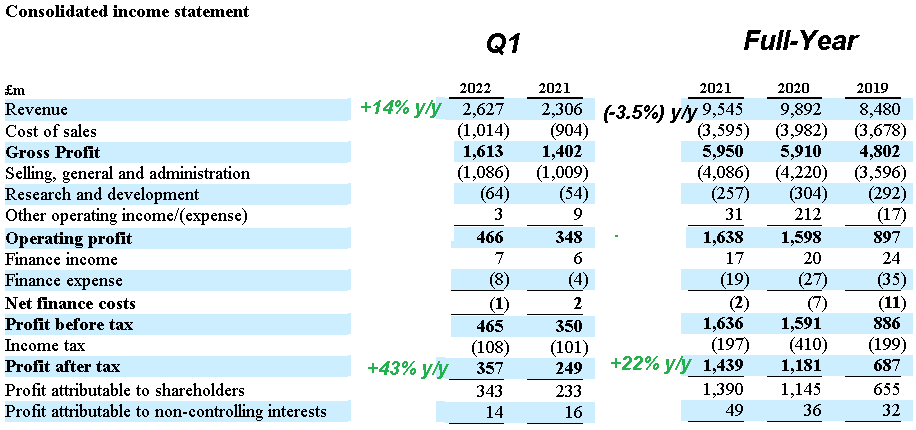

HLN Key Metrics

The company with headquarters in the United Kingdom uses the British Pound as its functional currency. Ahead of the spinoff, the company noted GBP 9.5 billion in sales for 2021 which was a decline of 3.5% year-over-year. That said, the context considers that 2020 was a blowout for over-the-counter medications during the height of the pandemic driving a 17% increase in sales with consumers looking for fever-reducing drugs and cold remedies. By this measure, 2021 revenue was still up 13% from the 2019 pre-pandemic benchmark.

source: company IR

The more impressive trend has been the firming profitability, with the 2021 profit after tax up 22% from 2020. The result has been driven by climbing margins based on pricing initiatives and the sales mix, along with a decline in SG&A as a percentage of revenue. The Q1 data was also strong with Haleon posting revenue of GBP 2.6 billion, up 14% while the profit after tax surged by 43%, propelled by a higher gross margin.

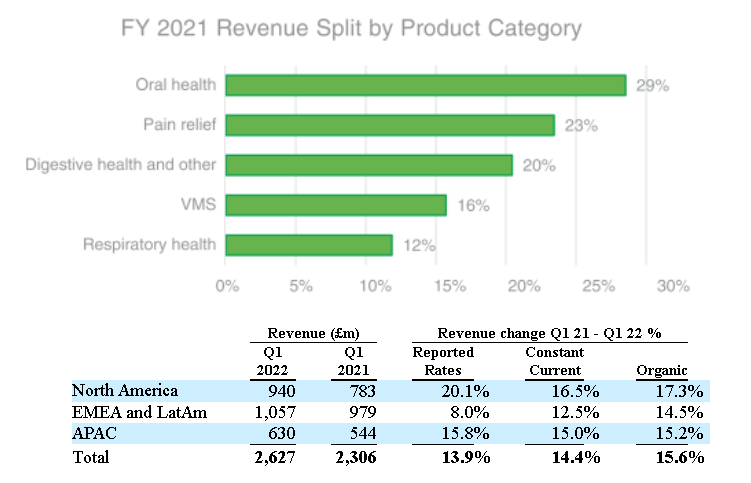

Preliminary Q2 data released in late July was highlighted by 12.9% organic revenue growth while noting e-commerce sales are now 9% of the total business with “growth in the high teens”. For the full year, management is targeting organic revenue growth between 6% to 8%.

For reference, the oral health product category which includes specialty toothpaste and mouthwash products represented 29% of the business in 2021, followed by pain relief medication at 23%, and digestive health at 20%. By region, the operation is global with North America contributing around 36% of sales while EMEA and LatAm together represent 40%.

source: company IR

The company has approximately GBP 9.4 billion or $11.1 billion in long-term debt. Considering GBP 2.4 billion in adjusted EBITDA for the fiscal year 2021, the leverage ratio is currently around 4x. While this level is elevated, the significant cash flow generation keeps the liquidity position stable.

Within Haleon’s guidance, management wants the net debt to EBITDA leverage ratio to trend under 3x by the end of 2024. Over the medium term, the forecast is for organic annual sales growth of 4% to 6% “ahead of the market” driven by momentum in oral health and increasing penetration of high-growth emerging markets. We mentioned the future dividend. While no amounts have been confirmed, statements suggest an initial payment in 2023 based on the second half of 2022 financial results at the lower end of a 30% to 50% payout ratio.

source: company IR

Is HLN Undervalued?

There’s a lot to like about Haleon with its flagship products holding top spots in terms of market share globally. High-level themes of an aging global population boosting demand for these types of personal healthcare categories along with an emerging middle class in developing countries purchasing more packaged consumer products highlight the long-term bullish case for the stock.

We already mentioned several of the “power brands” like Advil and the list is extensive with everyday items consumers count on like “ChapStick” and even “Nicorette gum” as an FDA-approved medicine to help people quit smoking. It’s fair to say that Haleon immediately enters the top tier of consumer staple blue chip companies through its portfolio.

source: company IR

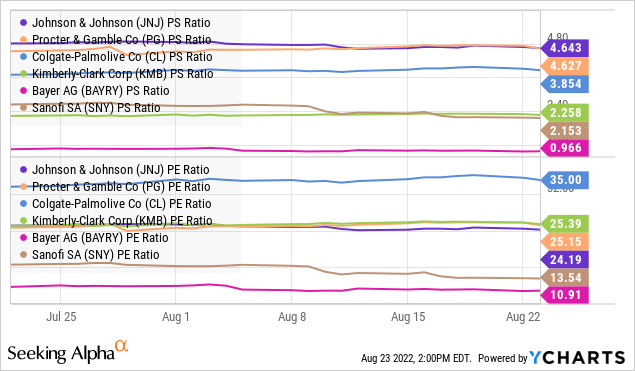

What we like about Haleon is that its relatively unique as a large cap pure-play on consumer “retail” healthcare while most of its major peers have a broader profile in pharmaceuticals or household staples. We can place Johnson & Johnson (JNJ), Procter & Gamble Co (PG), Colgate Palmolive Co (CL), Kimberly Clark Corp (KMB), Sanofi (SNY) along with Bayer AG (OTCPK:BAYZF) in this group. Each of these companies offers competing products in specific categories, but also have key differences given various operating strategies and category exposure.

What we find is that based on some basic valuation metrics, HLN appears undervalued next to the “consumer staples” leaders. HLN with a market cap of approximately $29.2 billion and $13.0 billion in revenue over the past year, is trading at a price-to-sales multiple of 2.2x. This is well below stocks like JNJ and PG that are closer to 5x but similar to KMB and SNY at 2x. Approximating a P/E ratio for the stock at around 18x based on earnings over the past year, HLN also sits discounted to consumer staple names like JNJ and KMB closer to 25x but at a premium to the more “pharma” stocks like Bayer and Sanofi averaging 12x. We believe HLN has room to converge higher.

A key point here is that shares of HLN are off around 20% from its debut price. One explanation we offer is that some shareholders receiving the stock into their brokerage account may have simply sold off the position, either to quickly realize some liquidity or based on confusion as to what Haleon is. The setup here creates an opportunity to pick up the stock that is simply beaten down. Of course, we’ll need the broader market sentiment and momentum in equities to cooperate, but HLN can outperform to the upside with a view that macro conditions can improve going forward.

Final Thoughts

We’re bullish on HLN and expect to see it rebound back to its debut price of around $7.30 representing at least 20% upside from the current level. We sense that as more investors become aware of the company’s corporate profile and product portfolio covering market-leading brands, shares have room to command a higher valuation multiple.

We can look forward to HLN’s Q2 earnings report set to be released on September 19th. This will be the first report as an independent publicly traded company and provide management with the opportunity to update on current market conditions and forward guidance. The operating margin and growth trends by region will be key monitoring points.

Be the first to comment