400tmax

Introduction: Why is Alphabet Stock Up?

Alphabet Inc. (NASDAQ:GOOG) (NASDAQ:GOOGL) reported Q2 2022 results after markets closed on Tuesday (July 26). Shares rose 5% in after-market trading, but remain 27% below their 52-week high and just 8% above their 52-week low:

|

Librarian Capital’s GOOGL Rating History vs. Share Price (Last 1 Year)  Source: Seeking Alpha (26-Jul-22). |

(Alphabet has two classes of shares, A and C, with the same economic rights and similar prices; in this article we refer to Class C share prices only).

We initiated our Buy rating on Alphabet in January 2021. Despite their 23.6% year-to-date decline, Alphabet shares are currently up 16.4% since our initiation.

Q2 results support our investment case. Alphabet revenues grew by 16% in local currencies in Q2, after growing 57% last year, demonstrating Alphabet’s resilience in an uncertain world. EBIT margin fell, in part due to elevated margins in 2021 and with hiring now being slowed. There are near-term headwinds, but they are manageable. We believe Alphabet can continue to grow earnings at double-digits annually on average over time, and the stock is trading at just 17.7x 2021 EPS. Our revised forecasts show a total return of 165% (31.2% annualised by 2025 year-end). Buy.

Alphabet Buy Case Recap

We believe Alphabet can deliver a low-teens EPS CAGR for the foreseeable. This includes a low-teens revenue growth driven by multiple businesses:

- Search & Other growing at mid-single-digits or higher, with the advertising sector growing at GDP or faster, and Google continuing to gain share thanks to its competitive advantages, including its technology and network effect

- YouTube Ads growing at strong double-digits; this is a relatively new product growing at 30%+ a year in recent years, thanks to still-rising user consumption and continuing improvements in ad technology

- Network Member Properties growing at mid-single-digits, driven by similar drivers as those of Search & Other

- Google Cloud growing at strong double-digits, based on increasing demand for cloud computing and Google Cloud’s differentiated strategy and ability to leverage Alphabet’s unique advantages

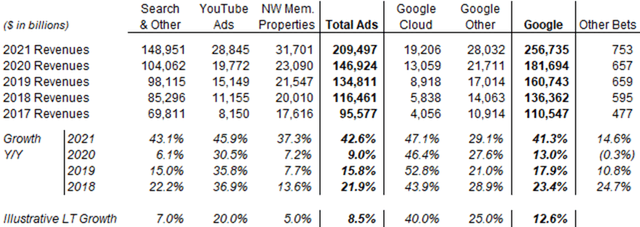

These revenue growth assumptions are likely conservative, being significantly lower than Alphabet’s track record to date:

|

Alphabet Revenues & Revenue Growth by Segment (2017-21)  Source: Alphabet company filings. |

We expect EBIT to grow slightly faster than revenues, thanks to both economies of scale and operational leverage in Alphabet’s platform. We also expect buybacks to reduce the share count by approx. 2% each year. The overall result is a long-term low-teens EPS growth.

Alphabet’s current P&L likely understates its profitability, as the company remains in investment mode; losses at Google Cloud and Other Bets alone are equivalent to approx. 10% of group EBIT (as of Q2 2022). The latter also mean standard metrics like P/E tend to overstate Alphabet’s valuation.

Q2 2022 results again showed double-digit revenue growth, despite an exceptionally strong prior-year quarter.

Revenue Growth at Double-Digits in Q2

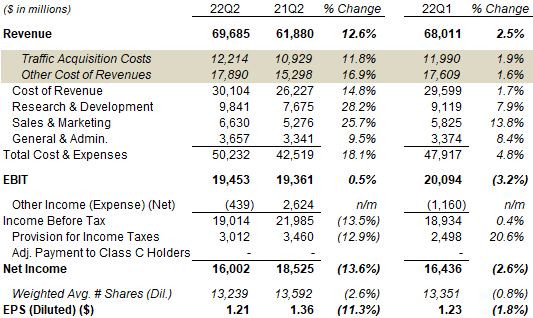

In Q2 2022, Alphabet revenues grew 12.6% year-on-year (16% in local currencies), after an exceptionally strong prior-year quarter when they grew 61.6% year-on-year (57% in local currencies):

|

Alphabet Group P&L (Q2 2022 s. Prior Periods)  Source: Alphabet company filings. |

Revenue growth was broad-based geographically, at 16% in the U.S., 18% in EMEA, 11% in APAC and 28% in Other Americas (all figures in local currencies).

EBIT grew 0.5% year-on-year, as costs and expenses grew faster than revenues. The strengthening USD represented an additional headwind for EBIT as Alphabet’s cost base is weighted towards the U.S.

Within costs and expenses, Traffic Acquisition Costs grew 11.8%, slightly slower than revenues. Other Cost of Revenues grew 16.9%, with the biggest factor being data centers and other operations. Research & Development and Sales & Marketing costs both grew faster than revenues, due to headcount growth and increased spending on ads and promotions. General & Administrative costs grew less than revenues, in part due to lower litigation costs.

Other Expense was $439m, compared to an Other Income of $2.6bn in the prior year, largely due to losses on debt securities ($790m) and equity investments ($251m), compared to gains last year (of $111m and $2.77bn, respectively).

Net Income fell 13.6% year-on-year in Q2, largely due to the Other Expense. EPS fell 11.3%, helped by the share count being 2.6% lower after buybacks.

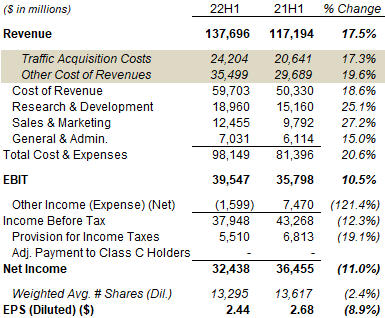

Across H1 2022, revenues grew 17.5% year-on-year, EBIT grew 10.5%, Net Income fell 11.0% and EPS fell 8.9%:

|

Alphabet Group P&L (H1 2022 s. Prior Periods)  Source: Alphabet company filings. |

As the decline in Net Income was largely due to mark-to-market losses on debt securities and equity investments, we believe H1 EBIT growth of 10.5% represented a better measurement of underlying earnings growth.

Alphabet’s results also demonstrated its resilience in a high-inflation scenario. Revenues grew far ahead of inflation, likely helped by the natural power of its auction-based ad pricing system. Much of its expense growth was due to not salary increases but a headcount expansion (up 21% year-on-year to 174k), with the latter intended as an investment and now in the process of being slowed (more below). We expect earnings to continue to grow ahead of GDP.

Revenue Growth Again Broad-Based

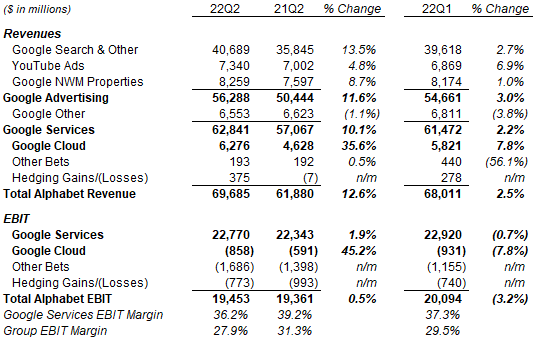

Alphabet’s revenue growth was again broad-based in Q2, though lower due to currency headwinds and an exceptionally strong prior-year comparable:

|

Alphabet Revenue & EBIT by Segment (Q2 2022 vs. Prior Periods)  Source: Alphabet company filings. |

Google Search & Other revenues grew 13.5% year-on-year in Q2 (compared to 68.1% last year), driven by Travel and Retail. Travel benefited from strong user interest heading into the summer. In Retail, even with shoppers returning to physical stores, retailers have continued to build their digital presence to drive both online and offline sales.

YouTube Ads revenues grew just 4.8%, after an “uniquely strong” 83.7% growth last year. “Time spent on YouTube globally has continued to grow”. Short-form video consumption is increasing across multiple platforms, including YouTube, and Alphabet has seen encouraging early results in monetising its Shorts format. However, revenues did decelerate quarter-on-quarter, which “primarily reflects pullbacks in spend by some advertisers”.

Google Network Member Properties revenue grew 8.7% year-on-year (compared to 60.4% last year), driven by the AdSense product. Here too revenues decelerated quarter-on-quarter because of pullbacks by some advertisers.

Google Other revenues fell 1.1% year-on-year, “primarily“ due to lower revenues from the Play store after Alphabet reduced its commissions on subscriptions from 30% to 15% at the start of 2022. (This followed a similar reduction in commissions on apps at the start of July 2021.)

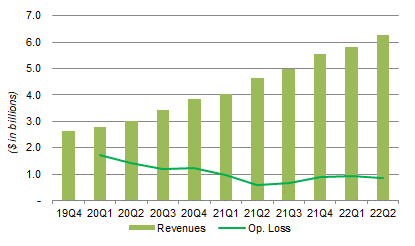

Google Cloud revenues grew 35.6% year-on-year in Q2, compared to 43.8% in Q1 and 53.9% in the prior-year quarter, continuing its trajectory of strong revenue growth with limited operating losses:

|

Google Cloud Revenues & EBIT by Quarter (Since Q4 2019)  Source: Alphabet company filings. |

The continuing revenue growth across Alphabet businesses, in a quarter with significant macro headwinds and uncertainties, demonstrates the essential nature of its products.

Growth Volatility from Prior-Year Comps

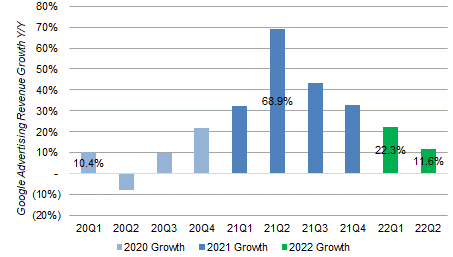

The long-term growth trend in Google Adverting revenues is clear, and recent growth rates should be viewed in the context of prior-year comparables.

As in prior quarters, year-on-year growth in Google Advertising revenues seems to be trending down:

|

Google Advertising Revenue Growth by Quarter (Since 2020)  Source: Alphabet company filings. |

However, the trajectory is in part the result of different quarters having different prior-year growth rates, with Q2 2022 being the last quarter that has a prior-year comparable where year-on-year growth was accelerating.

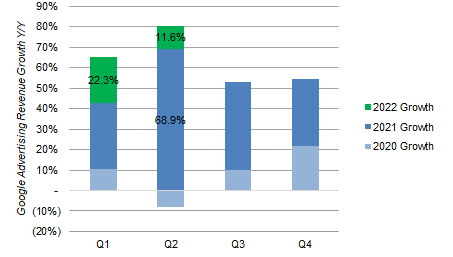

Another way of looking at things is that Google Ad revenues in Q2 2022 was 89% higher than the trough in Q2 2020, the first quarter fully impacted by COVID-19. Compared to 2019 levels, ad revenues were 73% higher in Q2, compared to 78% higher in Q1, reflecting both currency headwinds and likely a slight worsening in macro backdrop:

|

Google Advertising Revenue Growth by Quarter – Stacked (Since 2020)  Source: Alphabet company filings. |

Volatility in quarterly growth rates is inevitable and we believe investors should not focus too much on them.

Near-Term Headwinds, But Manageable

Alphabet CFO Ruth Porat highlighted continuing tough prior-year comparables, macro uncertainties and currency as near-term headwinds against revenue growth:

Going forward, the very strong revenue performance last year continues to create tough comps that will weigh on year-on-year growth rates of advertising revenues for the remainder of the year. In YouTube and Network, the pullbacks in spend by some advertisers in the second quarter reflects uncertainty about a number of factors that are challenging to disaggregate. Within other revenues in the third quarter, we expect an ongoing headwind from the fee changes and the slowdown in buyers spend that impacted results in the second quarter … Looking to the third quarter, based on strengthening of the U.S. dollar quarter-to-date, we expect an even larger headwind from foreign exchange.”

However, lapping strong prior-year comparables seems to be the key hurdle to growth, while other issues were described as “idiosyncratic” and manageable. Here is Porat talking about YouTube specifically:

The lapping of what truly were extraordinary growth rates as time will get us through the lapping … I did note that we have seen pullbacks in spend by some advertisers … we do view that as rather idiosyncratic as I said, some of it is supply chain, some of it is inventory. And so, just working through that …

There were a couple of other factors that were relevant. The war was a modest headwind to year-on-year and sequential growth. ATT (App Tracking Transparency) impact, in fact, remained relatively constant, we’ve said that for the last couple of quarters … So, we’re working through those.”

We expect any slowdown in Google Advertising revenues to be “idiosyncratic” and temporary.

EBIT Margin Decline Likely Temporary

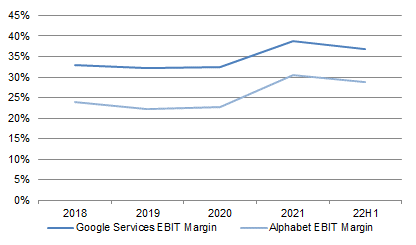

We are relatively relaxed about the EBIT margin decline in Q2, because it was in part due to elevated margins in 2021, and because hiring is now being slowed.

EBIT margin for Google Services was relatively stable in 32-33% during 2018-20, but jumped to 38.7% in 2021, in part due to timing and the pandemic delaying some investments. It fell to 36.8% in H1 2022 but remained much higher than pre-COVID levels.

|

EBIT Margins – Google Services vs. Alphabet Group (Since 2018)  Source: Alphabet company filings. |

(Group EBIT margin is less meaningful due to losses in fast-growing revenues in loss-making Google Cloud, as well as losses in Other Bets.)

Alphabet has already announced a slowdown in hiring in early July, and this was reaffirmed by management on the earnings call. However, headcount growth may not slow until 2023, due to commitments already made and the pending completion of the Mandiant acquisition by the end of the year.

While Alphabet does not have a margin target, we are comfortable that new cost control and continuing revenue growth will stabilize its EBIT margin in the near term, and that the natural operational leverage of its platform will produce an expanding margin over time.

Valuation: Is Alphabet Overvalued?

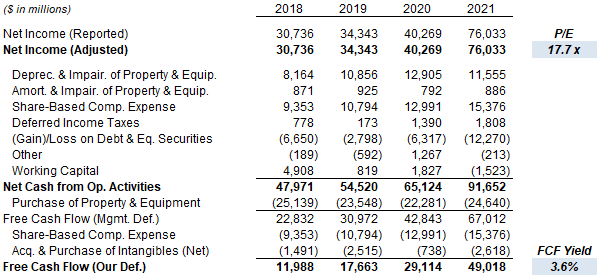

Relative to 2021 financials, Alphabet stock has a P/E of 17.7x (after adjusting out its $125bn of net cash, equivalent to 8.5% of the market capitalization) and a Free Cash Flow (“FCF”) Yield of 3.6%:

|

Alphabet Net Income & Cash Flows (Since 2018)  Source: Alphabet company filings. |

Alphabet’s “Other Bets” were reported as “non-marketable securities”, with a value of $29.5bn at Q2 2022, or 2.0% of its market capitalization.

Alphabet does not pay a dividend, but has been repurchasing its shares. Buybacks have been progressively increasing, exceeding $50bn in 2021 and $28bn in H1 2022, the latter representing 1.9% of the current market capitalization.

We continue to believe that Alphabet’s proven resilience (including during COVID-19) and its continuing double-digit EPS growth will justify a P/E of at least 35.0x; shares were trading at a 34x P/E when we initiated our coverage in January 2021. We believe Alphabet stock remains undervalued.

Where Will Alphabet Stock Be At?

We reduced our 2022 forecasts but keep other assumptions unchanged:

- For 2022, Net Income be flat (was 10% growth)

- From 2023, Net Income grows at 10% each year

- Share count falls by 2% a year

- P/E at 35x at 2025 year-end

- No dividends

The assumption of a flat Net Income is in part due to mark-to-market investment losses in “Other Income”. Alphabet EBIT was up 10.5% year-on-year in H1.

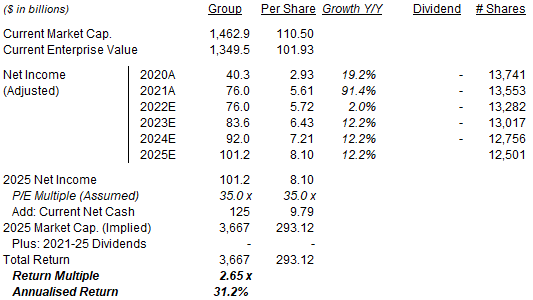

Our new 2025 EPS forecast is 9% lower than before ($8.90):

|

Illustrative Alphabet Return Forecasts  Source: Librarian Capital estimates. |

With shares at $110.50, we expect an exit price of $293 and a total return of 165% (31.2% annualized) by 2025 year-end.

Because of Alphabet’s sharp de-rating in the past few months, about two third of our forecasted return is generated by the assumed upwards P/E re-rating from 17.7x to 35x. If we were to assume a 17.7x P/E, the total return would still be 39% (9.5% annualized), roughly in line with EPS growth.

Is Alphabet Stock A Buy? Conclusion

We reiterate our Buy rating on Alphabet stock.

Be the first to comment