Michael M. Santiago

We placed a sell rating on Goldman Sachs Group’s (NYSE:GS) stock in September last year, and it is needless to say, we missed a trick as the stock has surged by nearly 20% ever since. We based our outlook on the company’s unfavorable revenue mix; however, most market participants clearly disagreed with our point of view.

Although our previous analysis has not yielded the desired result, we affirm our stance on Goldman Sachs’ stock in today’s article as we believe the company is not aligned to benefit from the current interest rate environment; here is why.

Not Aligned To Benefit From Higher Rates

Most banks outperform the broader market whenever interest rates exceed their moving averages. The theory behind it all is related to proliferating interest-bearing activities. Fundamentally speaking, higher interest rates support new debt instruments while slowing down the erosion of outstanding debt products.

Even though Goldman is a banking stock, its activities are centered on trading and dealmaking, with the latter taking place via its investment banking division. In fact, only 17.2% of Goldman Sachs’ revenue stems from interest-bearing activities.

Global interest rates are currently on the rise to curtail inflation. Additionally, credit spreads are aligned to generate significant income from the global debt markets. For example, Goldman’s net interest income grew 19% year-over-year as per its fourth-quarter financial results. However, as mentioned before, the bank is not aligned with an interest-bearing business model; thus, its broad-based revenue slumped by 16.19% year-over-year.

Sure, the bank’s interest division will likely mitigate a portion of its broad-based headwinds. But we do not see it doing enough to combat stale deals and trading environments.

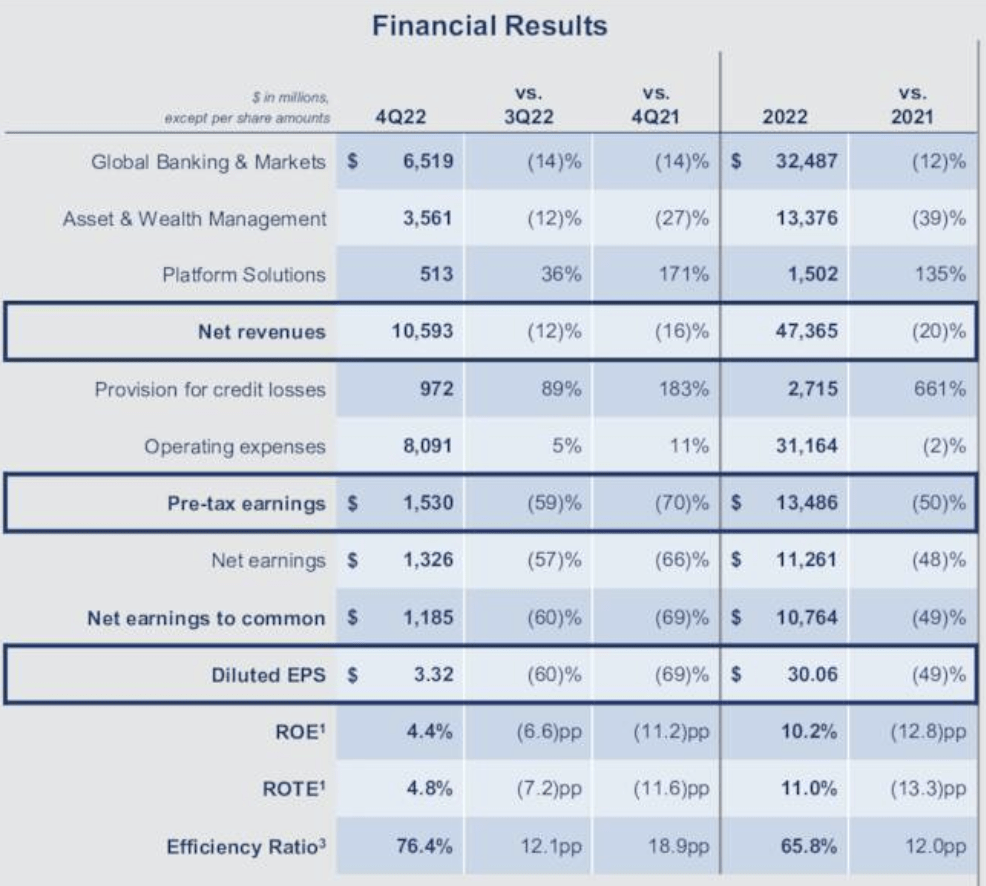

Exhibit 1 (Goldman Sachs)

As displayed in exhibit 1, Goldman’s net revenues slumped in Q4 due to lower services and trading revenues. We anticipate that the bank’s investment banking division will remain lackluster in 2023 as the deals environment is yet to recover. We base this on the fact that capital structures are unfavorable, which dilutes prospects for M&A and IPOs. In addition, based on mere opinion, most big four auditors will tell you that the deals environment is slow.

As for trading, well, this is a divided topic. Will the global financial markets recover in 2023? There is a possibility that inflationary inflection points and slower interest rate hikes will support corporate bonds and undervalued public equities. However, it remains a coin toss, and we don’t believe diversified portfolios aren’t set to recover until late this year (coincidentally with the investment banking environment).

Although most of Goldman’s prospects are underwhelming, the bank is experiencing tremendous growth in its platforms division, which is a secular growth segment. The business unit’s transaction banking revenues are up 51% year-over-year, and Goldman is actively working on enhancing platform solutions. Even though the division has illustrated robust growth, investors need to note that income statement amendments were made as provisions for credit losses increased by 1.48x year-over-year.

Lastly, there is a case that Goldman could benefit from volatile foreign exchange markets, as most banks did in 2022. The global FX sphere remains volatile, and cash transactions are in high demand. This could assist Goldman’s trading and services divisions.

Valuation & Dividends As A Counterargument

As for its valuation, Goldman Sachs is in fair value territory if we’re referring to its price-to-book value. In addition, the stock’s P/E ratio of 11.61x (GAAP) is in line with its cyclical midpoint, adding to our fair value argument.

Seeking Alpha

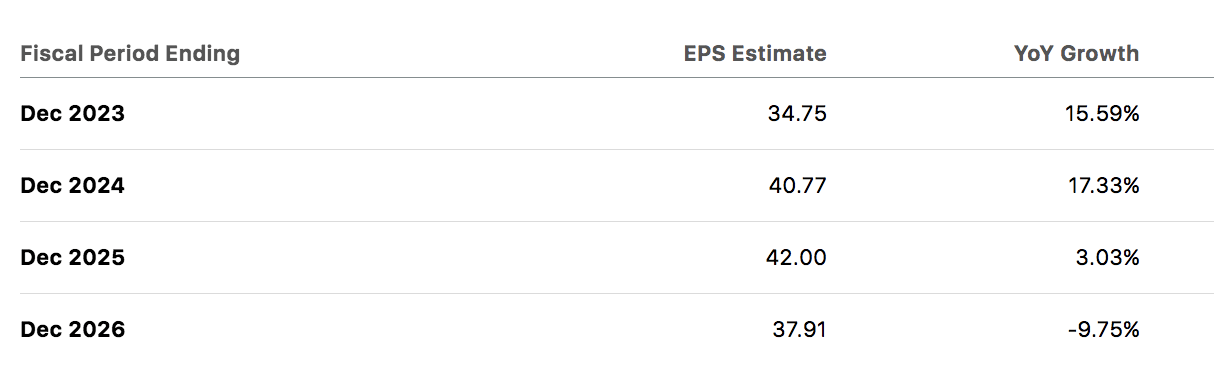

An advantage to the stock’s future valuation is Goldman’s anticipated earnings-per-share growth, which could compress its current price multiples. A census of Wall Street’s estimates suggests the bank’s EPS growth is ‘serially correlated’ to the upside, implying that residual value growth is en route.

Seeking Alpha

Furthermore, Goldman Sachs is a “best-in-class” dividend stock with a forward dividend yield of 2.86% and 11 years of successive dividend growth. Moreover, the stock’s current cash payout ratio is below its cyclical midpoint, while its dividend coverage ratio is standing strong at 3.34x. Thus, the stock could receive support from income-driven investors.

Seeking Alpha

Perhaps A Final Word

Despite its attractive valuation and dividend metrics, we remain bearish on Goldman Sachs’ stock. Our argument is based on the premise that the bank’s business model isn’t aligned to benefit from higher interest rates. In addition, we believe the deals environment will remain subdued in 2023. Thus, it is likely that analysts and investors alike are overestimating Goldman’s future earnings as they did before the company’s fourth-quarter earnings release.

Be the first to comment