BalkansCat/iStock Editorial via Getty Images

The activewear market faces moderating demand and cost pressures, hammering sales and income. Gildan Activewear, Inc. (NYSE:GIL) is no exception, given its elevated inventory levels. Still, it is a durable contender as it cushions these blows. Its core operations remain impressive as it balances revenue growth and margins. Its strategic pricing and cost-reduction strategies prove to be effective in coping with market volatility. It also maintains a decent level of liquidity. But it must take extra precautions with its cash levels and borrowings. Meanwhile, dividends keep increasing with enticing yields. Even better, the stock price remains reasonable and reflects the intrinsic value of the company.

Company Performance

It’s been almost two years since I last covered Gildan Activewear, Inc. The way I saw it, the company had promising prospects then. Fortunately, my supposition was right as GIL and the whole activewear market grew dramatically. Sales were still lower than pre-pandemic levels, but it was a massive rebound from 2020. It was understandable, given the restrictions and changing market dynamics. Some growth drivers were more on the behavioral side. These included the increased awareness of health and sports and being stuck at home for a long time. But in the last year, the picture has become quite different. Inflationary headwinds and geopolitical tension hampered the growth potential of the market. Supply chains have yet to complete their recovery, making it hard for many companies to sustain their growth.

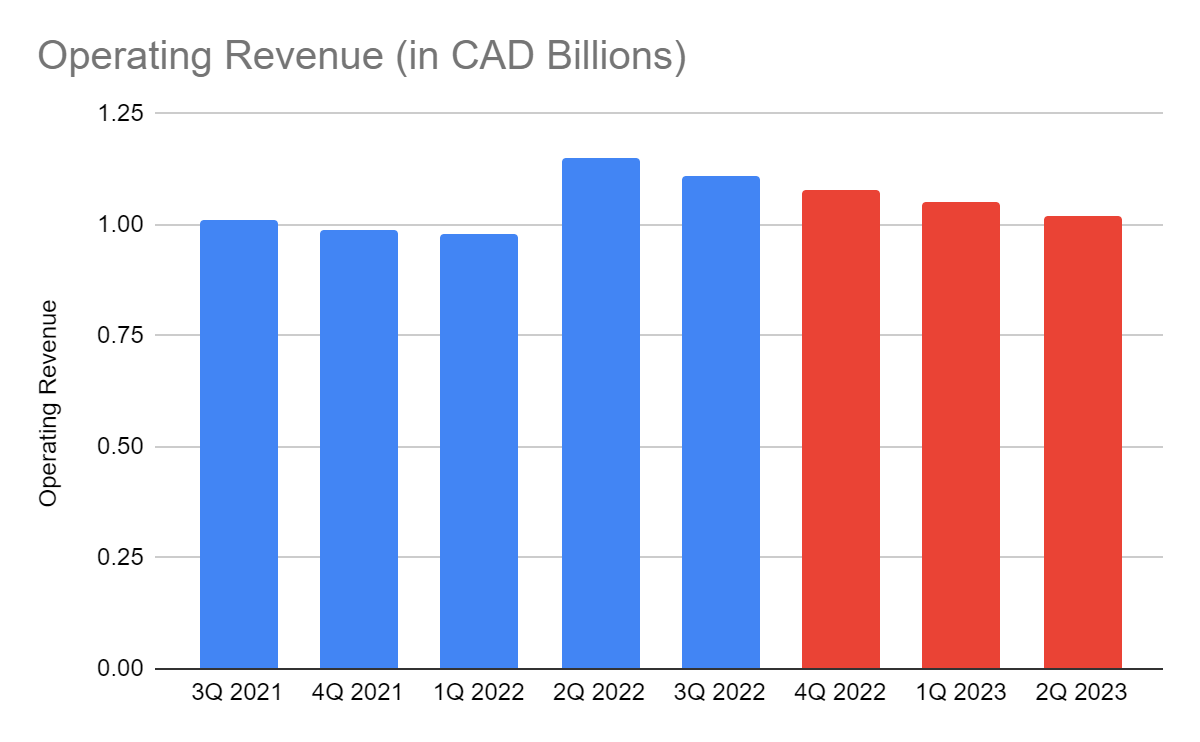

Gildan also faces challenges, but it continues to rise above them all. Its core operations remain solid despite the softening of demand and cost pressures. More importantly, its operating revenue remains relatively stable. It amounts to 1.11 billion CAD, a 10% year-over-year growth, which I find impressive. This growth amidst current market changes is attributed to different factors. First, the need to stay active, healthy, and fit continues. It is even more visible today as restrictions ease. More people are going to gyms or have their fitness routines at home as hybrid work setups persist. Second, the company sets strategic pricing, allowing it to cope with inflationary headwinds. It also helps offset the softening demand compared to 2Q 2022. Third, there is increased production and sales volume compared to 3Q 2021.

Amidst all these year-over-year improvements, it is essential to observe sequential changes and potential near-term changes. The past year was set as another excellent year for the industry. There has been an improvement in customer perceptions in line with looser pandemic restrictions. Their impact has been reflected in revenue growth. However, market challenges have become evident from 2Q to 3Q 2022, the softening market demand has become more evident. Inflation reached 9.1%, the highest in the last forty years. Thankfully for Gildan, its pricing strategy remains helpful in offsetting the impact of inflation on sales, although we can see a 4% sequential revenue decrease. This change can reflect the accruing challenges that started in 2Q. Despite the pessimism, I still find it logical since the current market also shows the normalization of demand. Right now, the cumulative revenues in the quarters amount to 3.24 billion CAD, which is about 86% and 89% of 2019 and 2021 annual revenues. I set the annual value of 2022 at 4.1 billion CAD, which is in line with the historical revenue growth. I also consider the impact of market volatility to make my projections more realistic.

Operating Revenue (MarketWatch And Author Estimation)

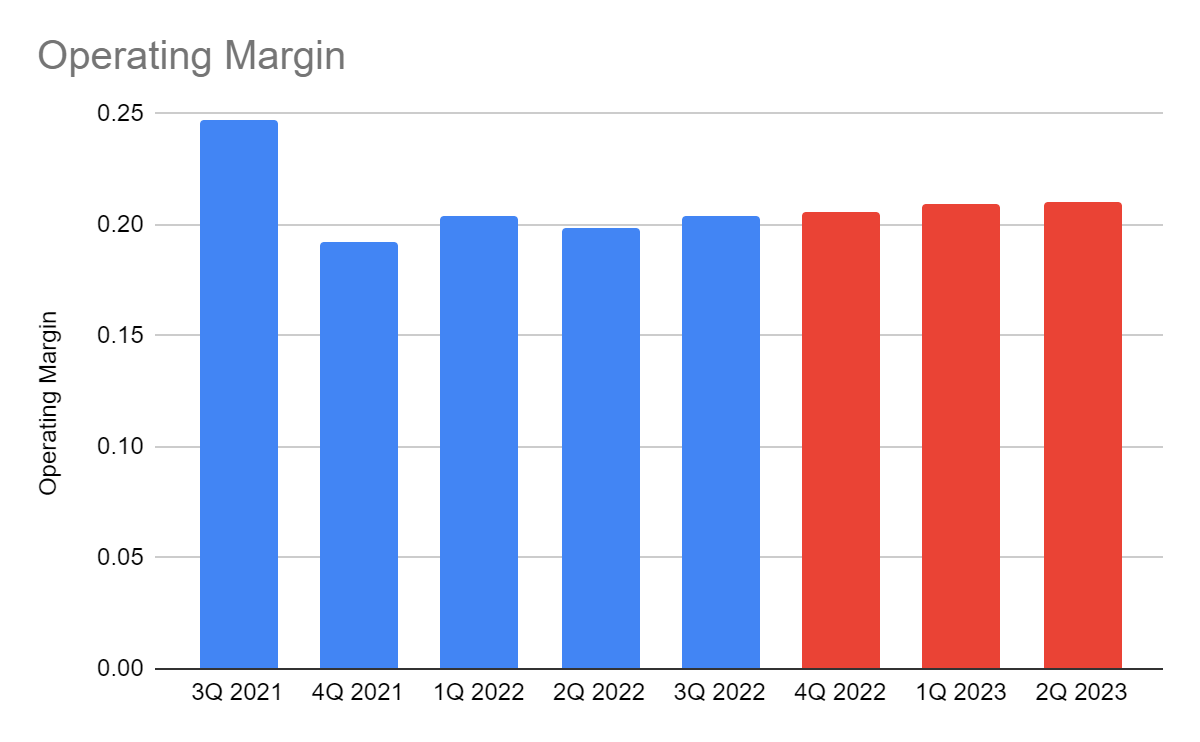

But what makes Gildan a solid company is its well-balanced revenue growth and margin stability. It works on attributes it can control and improve. It still has economies of scale, which is reflected by its operational efficiency. Costs and expenses remain manageable despite having a strong reaction to inflation. Revenue growth offsets their increase to remain viable. It is more crucial in 2022-2024 as inflation remains elevated despite the continued lull. With that, the operating margin remains high at 20.4%. Although it is lower than 3Q 2021 with 24.8%, it shows a sequential improvement from 2Q with 19.8%.

This year, I expect demand to normalize further. Near-term performance may be less exciting amidst recession fears. In a survey, about 50% of activewear and sportswear consumers plan to limit their spending or shift to cheaper items. It may take time for consumers to adjust, leading to lower purchases in the first half. Nevertheless, I expect tables to turn in the second half as the inflation lull speeds up. I also expect more stable margins as production becomes cheaper than in 2022. Having production centers in Honduras and Haiti is also an edge due to lower labor costs. And to fully unleash its potential, it must first deal with challenges related to overstocking. It has been one of its problems in the past year. Handling it properly will help it adjust its operations to maximize viability. Setting profit-maximizing prices may help it improve sales volume. For instance, it can set prices a little lower than the breakeven point of 2022. It is doable since production is cheaper and may pay off in the second half. Also, GIL has a solid customer base. It is an established brand enjoying its deep ties with other popular brands. There may be an offsetting impact between sales and costs and expenses.

Operating Margin (MarketWatch And Author Estimation)

How Gildan Activewear, Inc. May Fare This Year

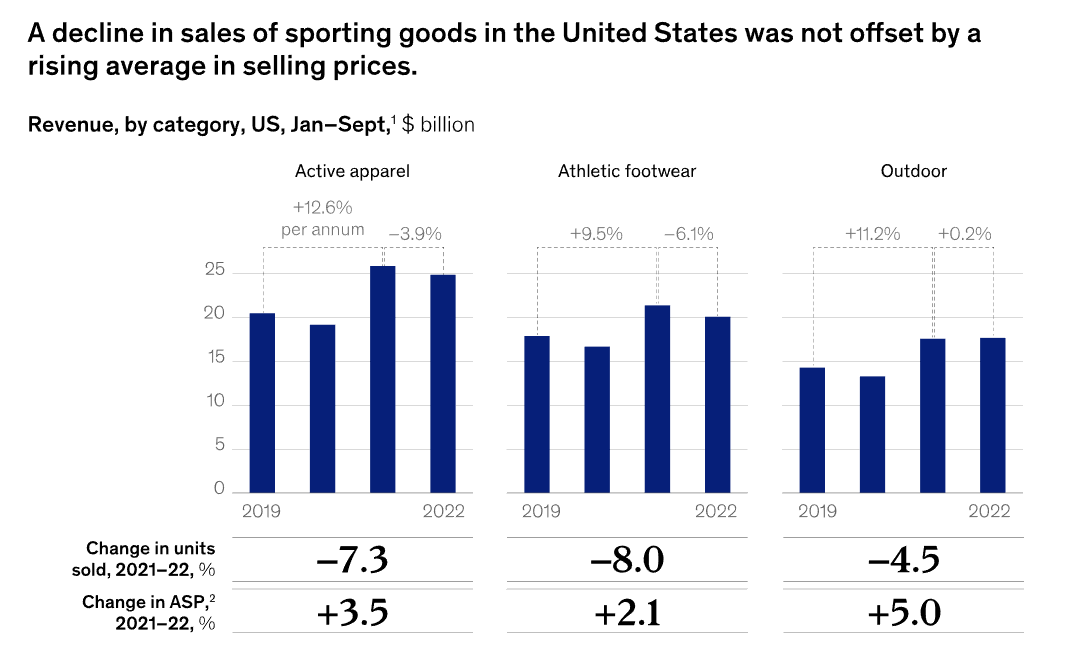

Despite the pessimism, the activewear market is still in a fortunate position, unlike many other industries. Near-term performance may be characterized by continued demand softening as the market normalizes. Even so, there are reasons to be optimistic about its medium-term performance. The primary growth drivers are the same, matched with the continued decrease in prices. The important thing is that Gildan continues to outperform the market as shown by the graph below. The market revenues are lower in 2021, which is the opposite for Gildan.

Sports Revenue (McKinsey & Company)

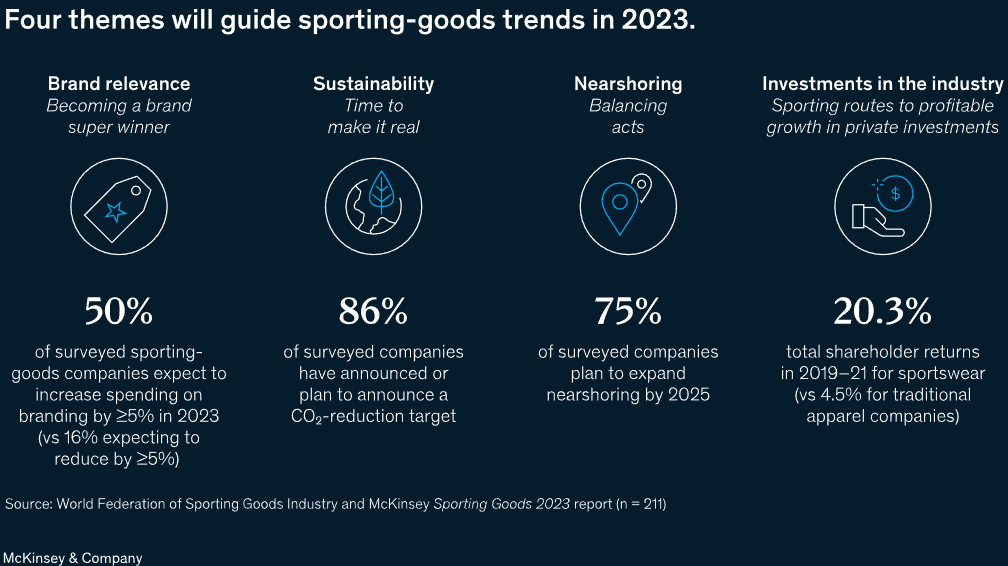

Today, the industry has four themes that will rule sporting trends in 2023. Thankfully, Gildan excels in three. Its brand relevance is reflected in its popularity and its deep ties with large brands. These include Under Armour, Gold Toe Brands, and New Balance. In sustainability, GIL keeps working on its ESG strategies, making it part of the Global 100 Most Sustainable Corporations. Lastly, it sustains its operational efficiency with its successful nearshoring in Honduras and Haiti. Lower production costs and international market presence are some of its fruits. It also allows it to compete with many Chinese companies geared toward predatory pricing.

Four Trends For Sporting Goods (McKinsey & Company)

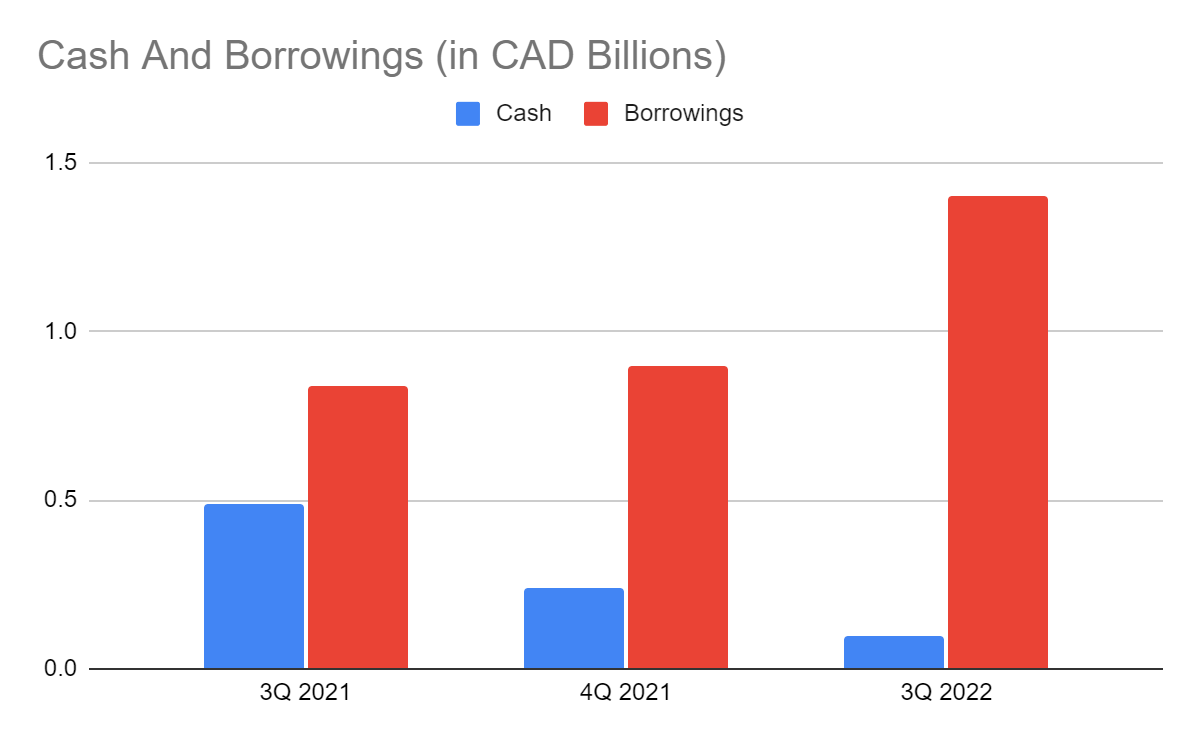

More importantly, GIL continues to sustain its operating capacity. Its financial positioning remains decent while withstanding market blows. Yet, the company must employ extra caution about its cash, inventories, and borrowings. As discussed earlier, overstocking appears to be one of its challenges. This excess inventory tends to tie up more cash as products are left unsold. It leads to cash burns and increased borrowings. It is evident in the cash and borrowings trend. We can confirm it in the cash flow statement, given the substantial increase in working capital cash outflows. In turn, it cannot cover the increased CapEx. The consolation we have now is that it still earns enough to manage cash flows and cover borrowings. The Net Debt/EBITDA ratio remains low at 1.08x. It can still balance growth with stability. It can sustain operating capacity amidst market headwinds.

Cash And Cash Equivalents And Borrowings (MarketWatch)

Stock Price Assessment

The stock price of Gildan Activewear, Inc. remains in a downtrend. It matches the softening market demand, but I find it overpessimistic. At $30.47, it is already 20% lower than its value last year. The price-earnings multiple of 9.1x and my estimated EPS of $4.1 reflects a target price of $36.76. An uptrend may also happen, given my valuation using the PTBV ratio. The current TBVPS of 6.96 leads to its PTBV of 4.4x. It is lower than the average of 4.8x. If we use the current TBVPS and the average PTBV, the target price will be $33.13. Both price metrics show a potential increase in the stock price.

Moreover, it stays a promising dividend stock with yields of 2.2%, better than the S&P 400 average of 1.54%. And even if we use the target price of $36-37, yields will be higher at 1.88%. These are all well-covered, given the dividend payout ratio of 20%.

FCFF 420,000,000 CAD

Cash 95,200,000 CAD

Borrowings 1,400,000,000 CAD

Perpetual Growth Rate 4.8%

WACC 9.2%

Common Shares Outstanding 183,793,000

Stock Price $30.47

Derived Value 44.84 CAD or $33.76

The derived value agrees with the prevalent supposition of an undervaluation. There may be a 10% upside potential in the next 12-18 months. Despite the pessimism, investors may use this as an opportunity to buy its shares at a discount.

Bottomline

Gildan Activewear, Inc. remains a solid company in a challenged market. It maintains a stable performance and sound financial positioning. It balances growth and sustainability, enabling it to cover borrowings and dividends. Also, the stock price trades at a discount, making it an entry point to make a position. The recommendation is that Gildan Activewear, Inc. is a buy.

Be the first to comment