Juan-Enrique/iStock via Getty Images

Successful deep-value investing requires investors get comfortable wading through the mud in order to seek out diamonds. Often, it is the firm that everyone else hates, with an awful balance sheet and poor analyst outlooks that beats the odds and turns around a surprise win that rewards those investors best.

One of the best value investors out there is the legendary Michael Burry (if you don’t know the name, you must have started investing yesterday). So when Burry speaks, people tend to listen closely.

In the second quarter of 2022, Burry disclosed to the world via his 13-F filings that he had opened positions in The GEO Group Inc. (NYSE:GEO), while he began to sell off all his other holdings. A flurry of analysis followed, including deep dives into his Twitter musings in order to understand his thinking.

But I’m certain most investors have, at some point, been burned by trading shares based on the recommendation of, and the recommendation alone, another person, be they a legendary investor like Michael Burry, a talking head on FOX, or perhaps a relative of friend. Trading based on recommendation alone is prone to risk. So even though a recommendation may be well-intentioned and perhaps even well-informed, it is still worth taking the time to perform your own due diligence.

Hence, we will be taking a look for ourselves at GEO, and using a peer analysis method to determine if there is indeed potential hidden value in the firm, what the financial health of the firm looks like, and attempt to find a pricing mechanism for the stock.

We will be comparing GEO to the ‘All US Stocks’ screener on Seeking Alpha, in an attempt to compare the market’s valuation of GEO to the valuations of the wider market.

(Data & prices correct as of pre-market 5th November, 2022)

(The “All US Stocks” list referred to in this article can be found on this Seeking Alpha screener)

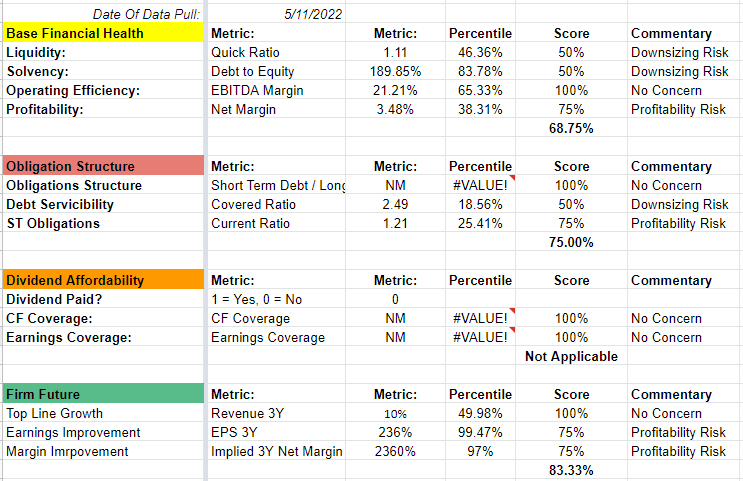

GEO’s Base Financial Health

GEO has been amassing long-term debt through bond issuances recently, and this has weighed on their balance sheet quite significantly, making GEO one of the top 20% largest debt-to-equity firms in the comparison group.

While EBITDA margins are strong, the firm’s net margins mean that scale is the source of profits for investors of GEO.

GEO’s covered ratio of 2.49 suggests that 40% of net operating income is servicing the immense debts the firm has accumulated, which represents a concern, and these are backed by a measly 1.21 covered ratio.

Lastly, while earnings outlooks are very positive, with average growth and well-above-average earnings outlooks, I note that GEO is historically prone to severe earnings surprises (GEO’s revenue estimates are historically reliable), so I have marked the EPS 3Y & implied net margin scores down slightly to account for the forecasting risk.

Author

Rounding out our financial health assessment, we score GEO a 72.71% overall financial health score, with significant debts causing most of the issues for the firm here.

Author

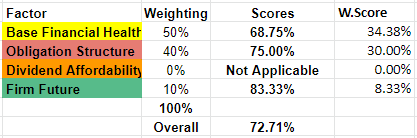

On the topic of forward-looking estimates, see below the summary of earnings surprises for GEO to illustrate the volatility of earnings for the firm.

Seeking Alpha

Assessing GEO’s Pricing Attractiveness

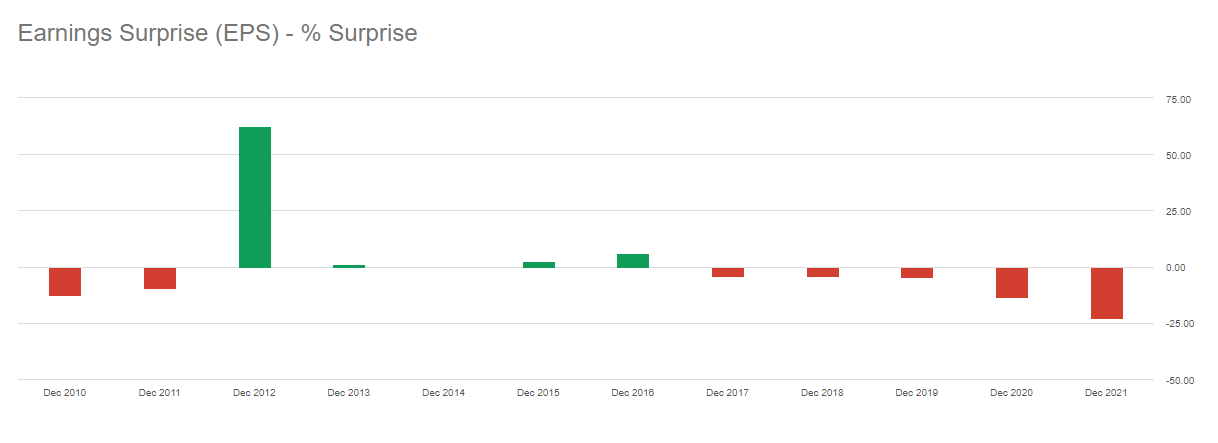

Balance sheets and financial health aside, GEO is relatively well priced compared to the market on most fronts, though GEO appears relatively fairly priced on its earnings.

Author

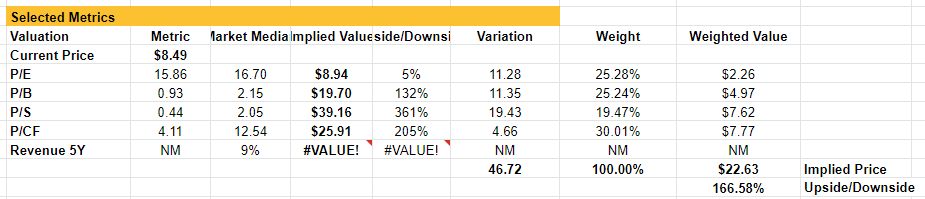

Finding An Appropriate Valuation Method For GEO

Approaching the challenge of finding a pricing mechanism for GEO, we assess and measure a broad range of standard and non-standard valuation methods in order to find the best fit for the comparison group, and therefore GEO.

Author

GEO is not well covered by analysts and forecast revenues and earnings only extend to 3 years, so we can’t rely on this as one of the most accurate pricing mechanisms for the comparison group.

But the method that remains provides us with a guidance of $22.63 / 166% fair value price based on the peer group.

Author

Risks & Headwinds

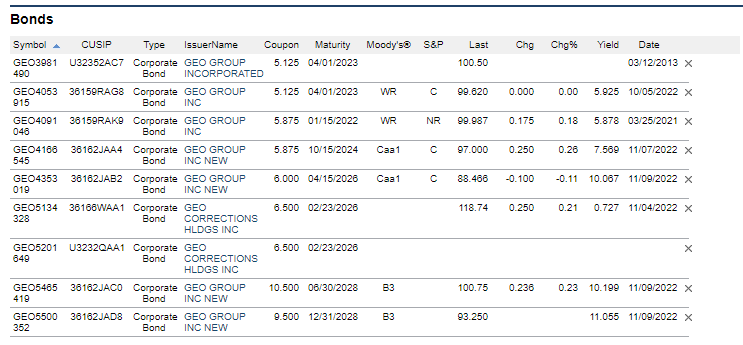

The first and most immediate risk to the firm is the debt levels that have accumulated for GEO. While the line of business the firm is engaged in is certainly capital intensive, bond traders are a reliable estimator of a firm’s financial risk.

FINRA bonds gives us an insight into the attitudes of bond traders of GEO, showing that both Moody’s and S&P have given GEO debt ‘junk bonds’ status and rates the debt as speculative.

FINRA Bonds

GEO also has an Altman Z score of 1.02, indicating that the firm is perilously close to insolvency.

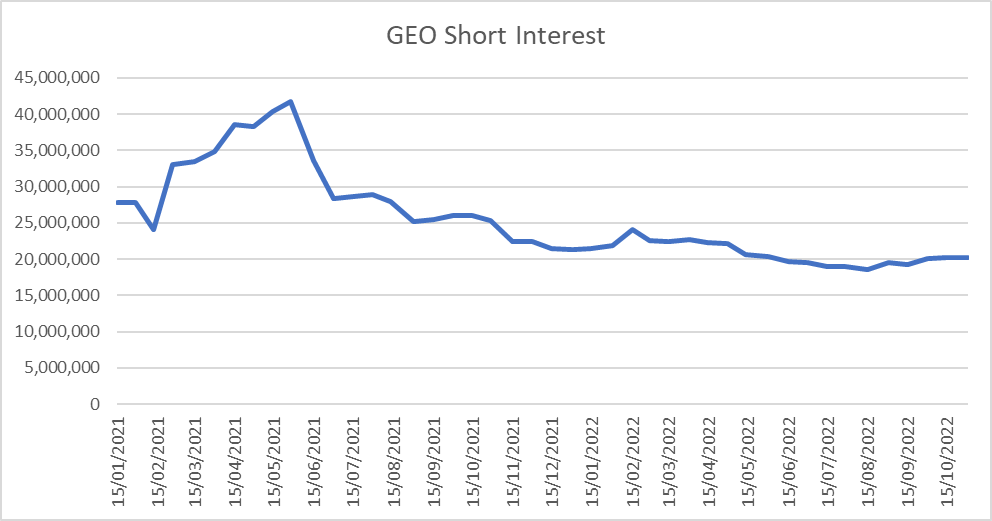

Further, over 17% of shares have been shorted, and while according to FINTEL the volume of shorts has fallen over time, the current volume is still significant.

Author

Lastly, from an ESG perspective, GEO is an ethically questionable firm given reports of forced prison labor being utilised as common practice. This is a grey-area where rights of prisoners meets the expectations of the community they have wronged in how their rehabilitation should be managed. While I hold no firm view on this worth putting in writing, I note that it is certainly worth being aware of.

Overall, if Michael Burry has waded through the mud, GEO’s value must certainly run deep, as this diamond appears very uncut.

So Is Michael Burry Right?

GEO is a tricky firm to place a rating on, given the highly leveraged balance sheet with edge-of-your-seat current ratios and debt serviceability, ‘junk bond’ status ratings by Moody’s & S&P, along with a pile-on of short sellers.

However, the firm is attractively priced compared to the wider market, and while earnings forecasts have historically been volatile, there is every chance that a positive surprise to earnings could see a positive upswing to the value of GEO.

As such, I am going to put a HOLD rating on GEO, given the risk/reward seems out of favor of buyers, but the catalysts are all in place for a positive windfall and potential short-squeeze should outlooks meet or exceed expectations.

Michael Burry is an investor with decades more experience than myself, a far more impressive track record and probably has better access to information than I do. But even he has had his losses, and unless he knows something I don’t about GEO, the investment thesis is just not there for me.

With that said, it would be irresponsible of me not to point out that this analysis is limited in its scope to just a quantitative peer analysis. While we do look at the firms financials, it does not go searching for detail and context that one might find reading earnings transcripts. Further, the analysis is of the market as a whole but does not consider the specific industry the firm operates in, and does not break down a near-peer comparison. Investors should use this analysis as a base-line for their analysis, but spend time looking at the firm’s qualitative aspects to further inform their thinking.

Author’s Note: The commentary in this article is general in nature and does not consider your personal circumstance. The opinions expressed in this article are opinions only, and data referenced is sourced from third party sources including Seeking Alpha and other publicly available sources.

I make no warranties or guarantees around any of the views expressed in this article and suggest all investors consider my writing to be for interest purposes only and not considered exhaustive investment research or advice.

Be the first to comment