RiverRockPhotos

Gold mining stocks have staged an impressive run over the past three months, outperforming even gold’s gains as is typical during precious metal bull markets. After being aggressively long over this period (see ‘GDX: The Tide Is Turning Bullish‘), I believe that the rally maybe about to reverse, particularly if we see gold prices relapse under the weight of rising real bond yields. The VanEck Vectors Junior Gold Miners ETF (NYSEARCA:GDXJ) in particular looks overstretched and overvalued.

The GDXJ ETF

The GDXJ tracks the performance of the MVIS Global Junior Gold Miners Index, a market-cap-weighted index of global gold- and silver-mining firms, focusing on small and mid-caps. The index covers global precious-metals-mining firms that generate at least 50% of their revenues from gold and silver. To ensure diversification, single stocks are capped at 8%. A sector-weighting cap factor is employed to ensure that 80% are determined as gold stocks, and silver stocks are limited to not go above 20%. The GDXJ charges an expense fee of 0.53%.

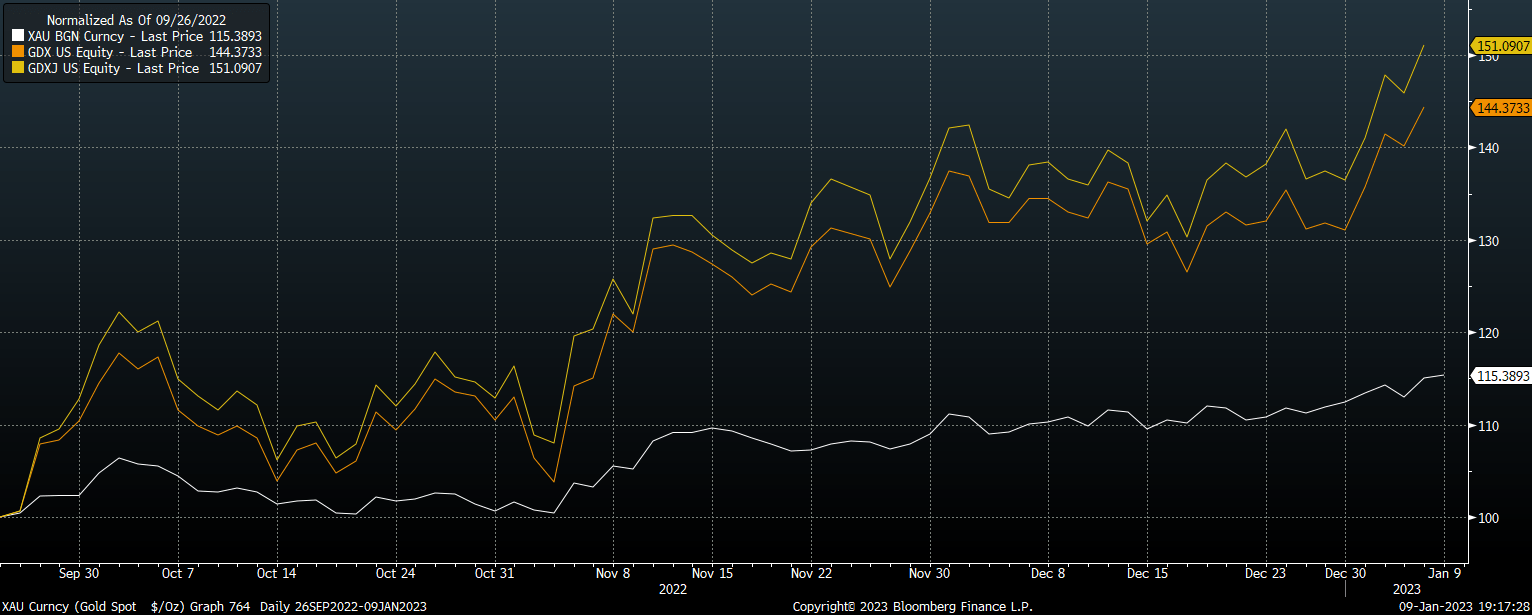

The GDXJ tends to outperform the large-cap GDX index during periods of gold strength as a small change in revenues can make a huge impact on the profits and equity values of smaller miners. This has been the case during the recent recovery as shown in the chart below. However, this also means that the GDXJ is susceptible to a potential gold price reversal.

Price Performance Since September Lows (Bloomberg)

Gold Out Of Line With Short-Term Fundamentals

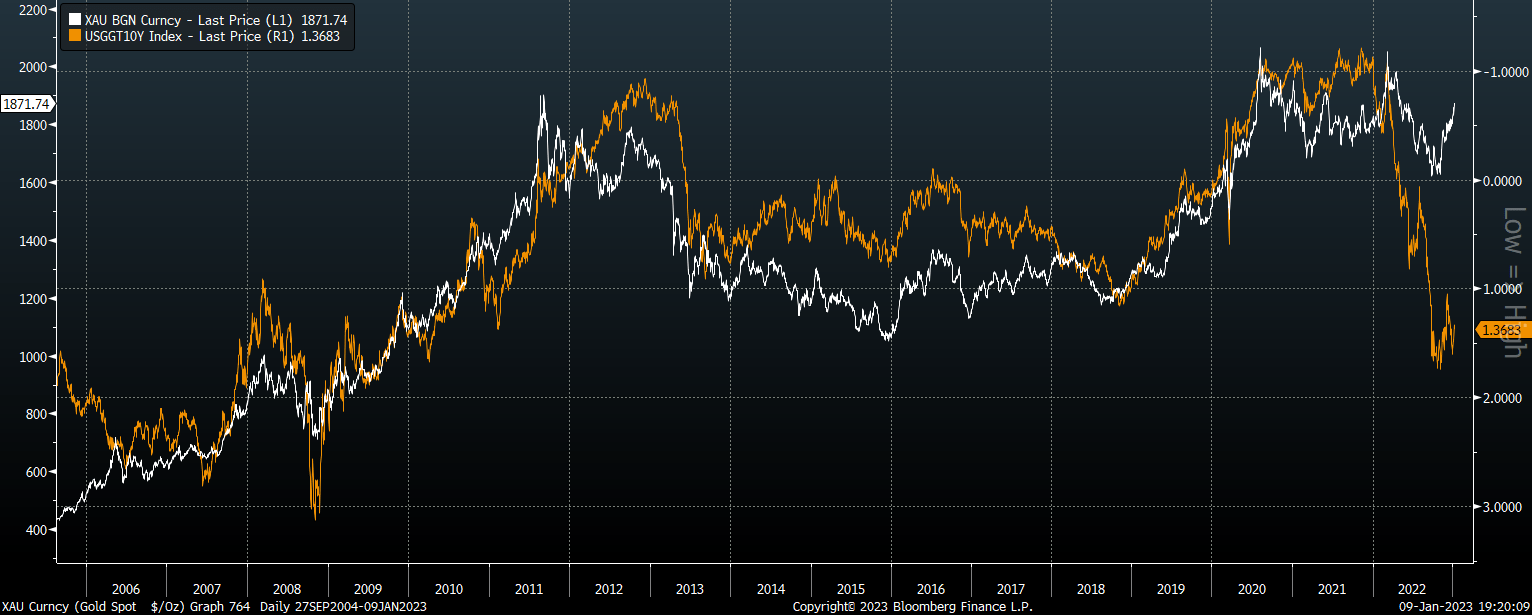

I argued last week that gold prices were looking overextended relative to their historical driver, notably real bond yields. Since then, the gap between gold prices and their fair value based on their correlation with real 10-year bond yields has widened further, suggesting gold’s rally is increasingly unsupported by the fundamentals right now.

Gold Price Vs 10-Year UST Yield (inverted) (Bloomberg)

Of course, this does not mean gold cannot continue to rally, but it does mean risks are tilted to the downside for now, and this means that risks to the GDXJ are even more heightened given its higher degree of volatility.

Ignore Claims That ‘Low GDXJ Levels’ Represent Undervaluation

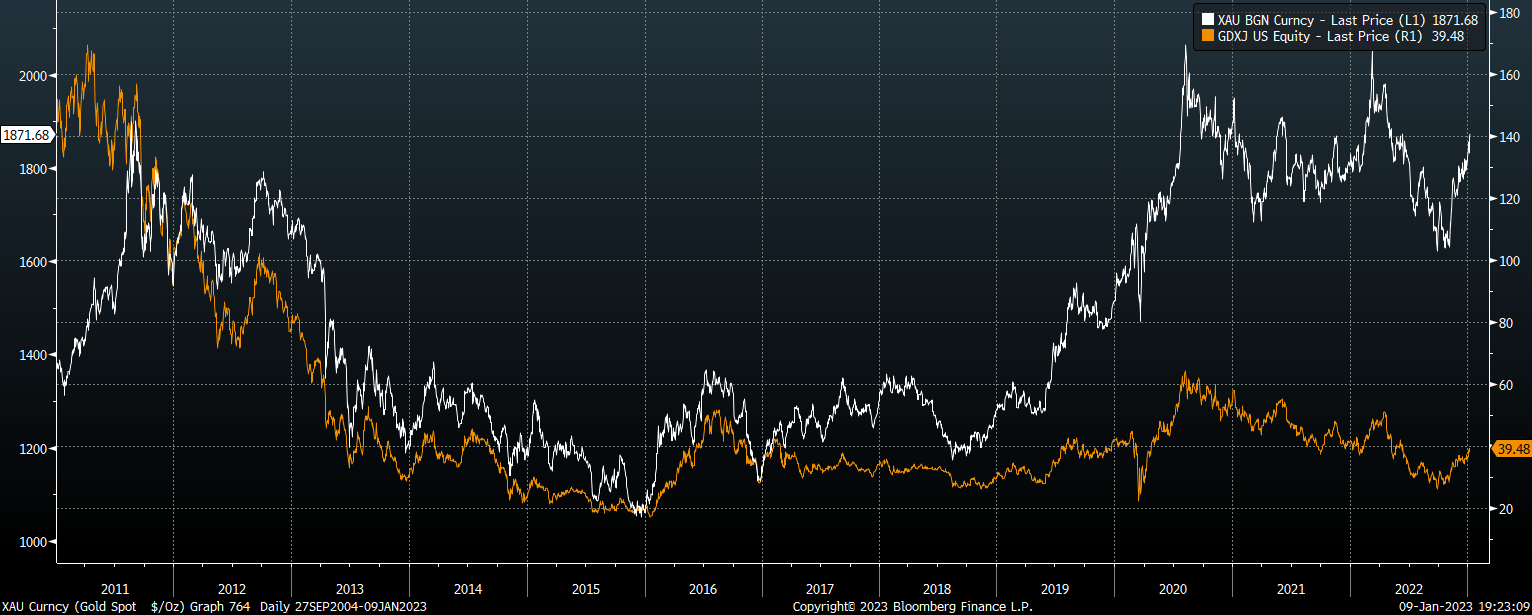

As I noted in my previous article on the GDXJ, many gold mining bulls point to the poor historical performance of the GDXJ relative to the price of gold as a reason to expect significant upside in the ETF. As the chart below shows, when gold first traded at current levels in 2011, the GDXJ traded over three times higher than it does now.

GDXJ Price Vs Gold Price (Bloomberg)

However, the GDXJ price does not take into account the increase in the market capitalization of the underlying index over this period. A surge in share issuance among the stocks in the index has seen the market capitalization of the MVIS Global Junior Gold Miners Index rise by almost 20% per year for the past decade. As a result, valuations are by no means cheap on a per share basis.

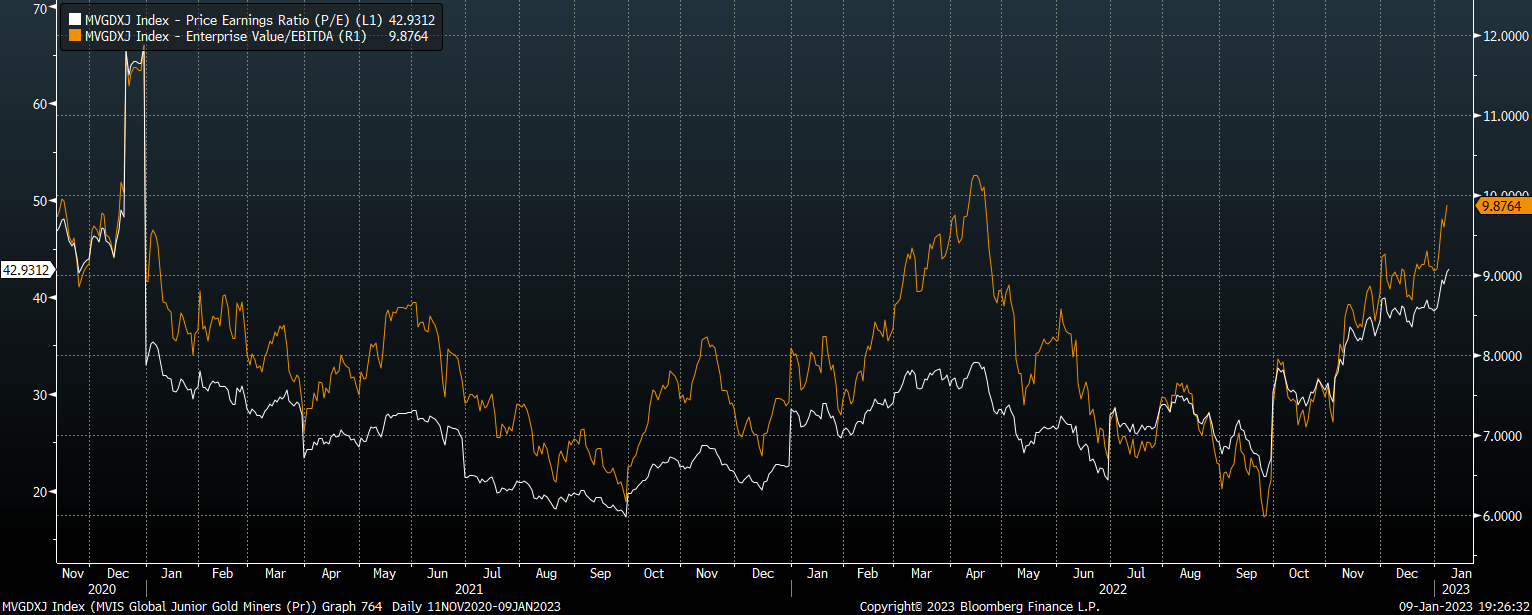

GDXJ PE And EV/EBITDA Ratios (Bloomberg)

One positive fundamental development for gold miners has been the decline in oil prices. As a key production cost, low oil prices should help to boost earnings and cashflows over the coming months, but even so, we would need much higher gold prices to justify current valuations. Investors are paying a premium highly for a speculative market sector in the hope that a rise in gold prices will see profitability improve dramatically, yet the opposite is just as likely to occur.

Summary

Junior gold miners have risen strongly over the past few months, with the GDXJ outperforming the sector as is typical of gold bull markets. With gold prices now looking overvalued relative to short-term fundamentals and GDXJ valuations still elevated, downside risks dominate at present.

Be the first to comment