DNY59/iStock via Getty Images

In mid-December, I noted that the relatively strong reaction of gold and gold mining stocks to the hawkish Fed meeting may be a sign that all the bad news is priced in. The VanEck Vectors Gold Miners ETF (NYSEARCA:GDX) appeared to be mounting a recovery until the release of the Fed minutes on Wednesday reignited concerns over accelerated Fed tightening, leading to a surge in bond yields and a decline in inflation expectations, which has kicked the legs from under the GDX recovery.

While real bond yields remain deeply negative across the entire curve out to 30 years, a shift from deeply negative to slightly negative should still be expected to undermine gold mining stocks if history is any guide. With this in mind, we could see the sector come under further pressure in the near term. However, I continue to believe that structurally loose fiscal policy will keep the long-term downtrend in real yields intact. Considering how undervalued the gold mining sector is relative to the current price of gold and the overall market, the GDX remains a strong long-term buy from a risk-reward perspective.

The GDX ETF

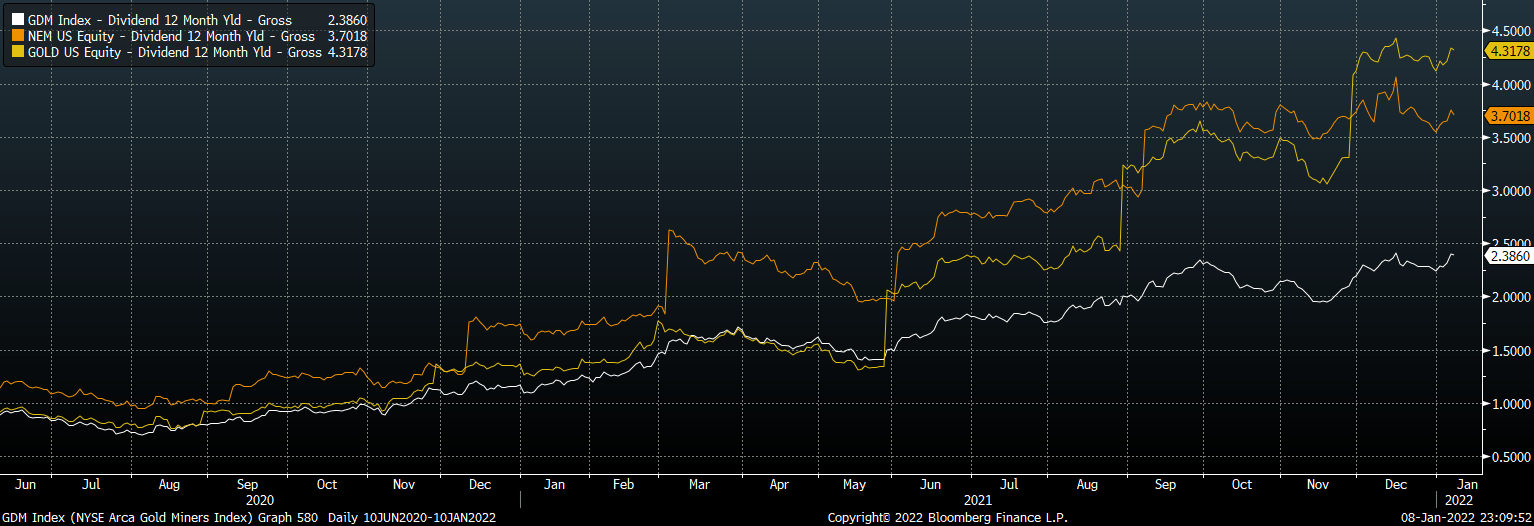

The VanEck Vectors Gold Miners ETF is the oldest, largest and most liquid gold mining ETF which tracks the performance of the NYSE Arca Gold Mining Index (GDM). Thanks to continued improvements in free cash flows, the GDX now offers a dividend yield of 1.8%, reflecting the underlying GDM’s 2.4% yield. The rise in the ETF’s dividend yield over the past year has been largely driven by the surge in payouts at Newmont and Barrick, which now offer 3.7% and 4.3%, respectively.

Dividend Yields: NYSE Arca Gold Mining Index, Newmont, and Barrick Gold

Bloomberg

The underlying index has a market capitalization of over USD279bn, larger than the alternative markets tracked by its peers such as iShares MSCI Global Gold Miners ETF (NASDAQ:RING), allowing investors more diversification. While both GDX and RING are dominated by Newmont (NYSE:NEM) and Barrick Gold (GOLD), their weighting in GDX is a combined 28% versus 36% for RING. Similarly, GDX’s top 10 holdings make up 65% of the index versus 72% for RING.

Taper Tantrum 2.0 Risks Are Overblown

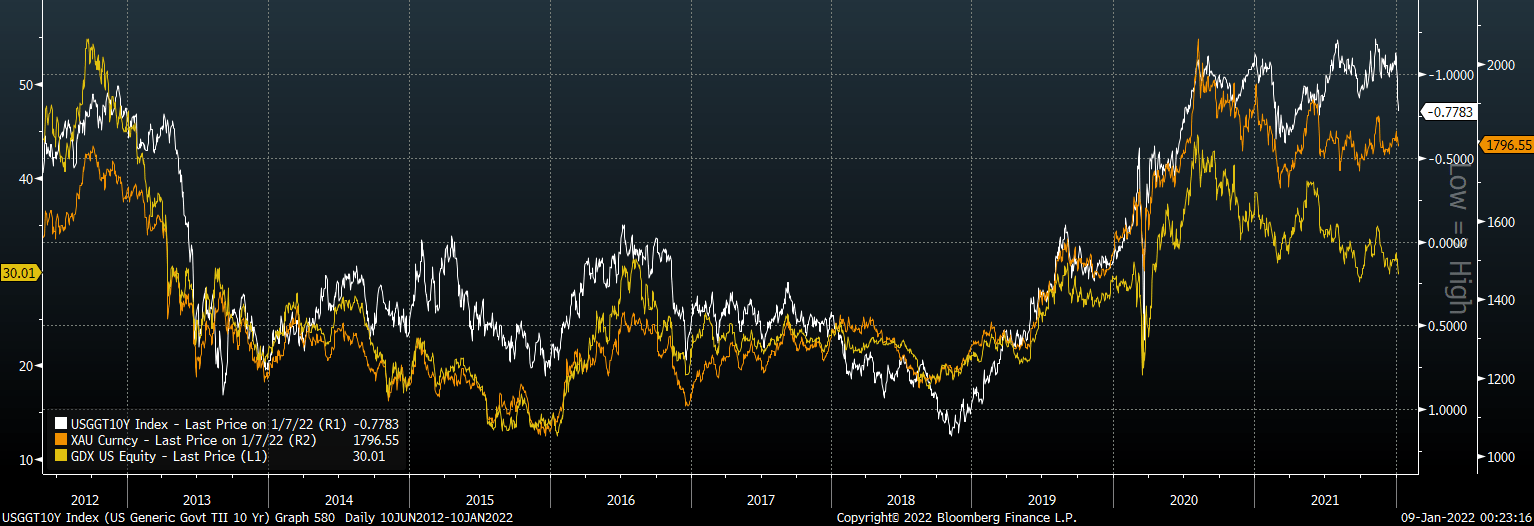

With real bond yields on the rise, every precious metal investor will likely be concerned over a repeat of the 2013 taper tantrum. A near-200bp rise in 10-year real yields from December 2012 to September 2013 contributed significantly to the 30% fall in gold prices over this period, which in turn caused the GDX to fall a staggering 60%.

U.S. 10-Year Inflation-Linked Bond Yields (inverted), XAU, and GDX ETF

Bloomberg

There are three major reasons why I do not expect to see a repeat of this period for gold mining stocks.

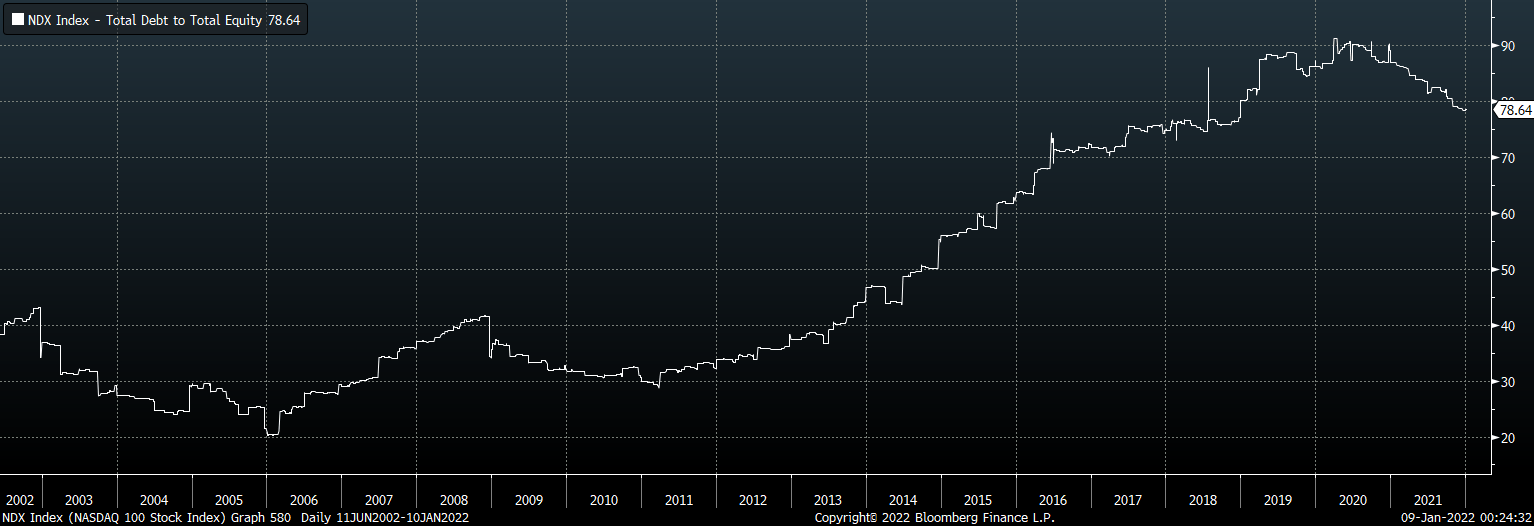

1) Real yields have less upside potential: The U.S. economy is currently saddled with much more debt when compared with the 2012-2013 period, which is likely to limit the extent to which policymakers will allow real yields to rise. On the corporate side, in 2013 the S&P 500 excluding financials had a debt-to-equity ratio of just 70% versus over 100% today, while companies listed on the Nasdaq had a ratio of 35% versus 79% today.

Nasdaq Debt-To-Equity Ratio

Bloomberg

This, together with significantly higher margin debt, helps explain why the relatively mild increase in real yields we have seen so far has undermined technology stocks to such a degree despite having no negative impact at all in 2013. Considering how concerned the Fed has become with asset prices in the recent cycle, further weakness here could be enough to bring about a more dovish tone.

On public sector side, debt was below 100% of GDP in 2013 and is now 122%, while the fiscal deficit is almost twice as wide as it was back then. Significantly higher real yields today would drive up borrowing costs and create a potential vicious cycle of more debt and even higher borrowing costs as investors anticipate wider budget deficits in the future. Of course, aggressive spending cuts and tax increases would allow real yields to rise without creating such a scenario, but it seems clear that neither politicians nor the general public are in favor of this path.

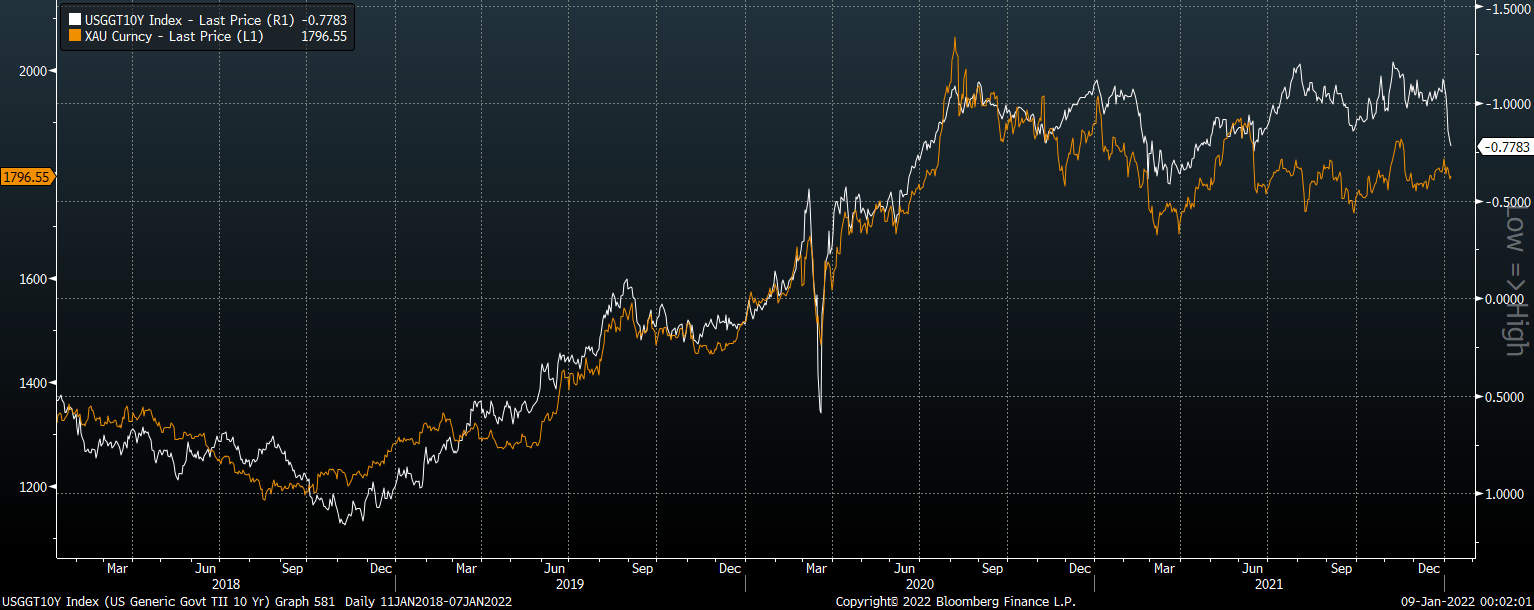

2) Gold is already cheap relative to current real yields: Even if real yields were allowed to continue rising, there is a case to be made that gold has already priced in such a move. As the chart below shows, the correlation between gold and real yields broke down over the past year to a large degree, with gold stagnating and real yields moving lower. This suggests that a rise in real yields does not pose as much of a threat to gold as it once did.

Gold Price Vs. 10-Year Inflation-Linked Bond Yield (Inverted)

Bloomberg

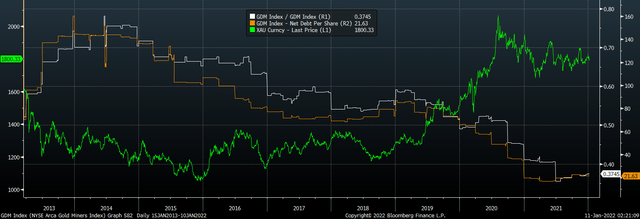

3) Mining sector balance sheets are much improved: Even if it were the case that real yields were allowed to rise significantly further and gold prices were to fall, the downside risks for gold miners are much lower than they were in 2013. In contrast to the broader equity market, the gold mining sector has significantly reduced its debt burden after being burnt by the 2013 gold crash and rate shock. This can be seen in the chart below which shows the gold price alongside the net debt per share and total debt/sales for the NYSE Arca Gold Mining Index. Prior to the 2013 gold price crash, net debt per share was 3.5x higher while total debt/sales ratio was 1.5x higher.

Gold Price, GDX Net Debt Per Share, GDX Total Debt/Sales

Bloomberg

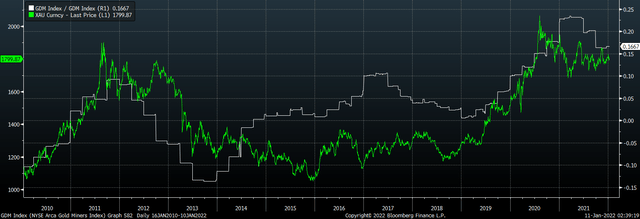

Alongside this deleveraging has been a renewed focus on free cash flow and away from all-out expansion. Prior to the 2013 gold price crash, the GDM’s free cash flow was actually negative as the chart below shows, which contrasts greatly to the picture we see today.

Gold Price Vs. GDX Free Cash Flow

Bloomberg

This article from April last year by BullionVault explains the shift in focus that has taken place since 2013. Improved balance sheets and free cash flow should allow the mining sector to navigate any gold prices declines more easily and reduce the risk of a spike in default concerns which helped drive down equity prices in 2013.

Summary

The surge in real bond yields over the past few days in response to the hawkish Fed minutes certainly pose near-term risks to gold and the GDX. However, fears of a repeat of the 2013 Taper Tantrum crash appear overblown as there is less room for real yields to rise this time around due to the Fed’s desire to support the stock market and extremely easy fiscal policy. There is also the possibility that gold’s underperformance over the past 18 months means it has already priced in the rise in real yields. Meanwhile, gold miners are much less levered than they were in 2013.

Be the first to comment