Leland Bobbe/DigitalVision via Getty Images

Shares of Gaming & Leisure Properties (NASDAQ:GLPI) massively outperformed the broader REIT index/ETF (VNQ) over the past year with a total return of 27% versus -17% for VNQ. In a turbulent macro environment, Gaming & Leisure has benefitted from contractually guaranteed cash flows under its triple net lease structure.

While I expect GLPI will continue to receive timely payments from its casino operator tenants, GLPI trades at the high end of its historical valuation range. This is in contrast to other sub-sectors of the REIT market (such as apartments, offices, etc) which are trading at the low end of their historical valuation range.

Resilient Cash Flow- Even in Downturns

GLPI has benefitted from the durability of its contractually guaranteed rental stream from regional casinos. GLPI has long (15-40 year leases) with strong casino operators including PENN Entertainment (PENN), Bally’s (BALY), Ceasars (CZR) and Boyd (BYD). At the present time all of these companies appear to be in decent financial shape. Of course casinos have a history of getting into trouble which is why GLPI makes use of master leases (described below).

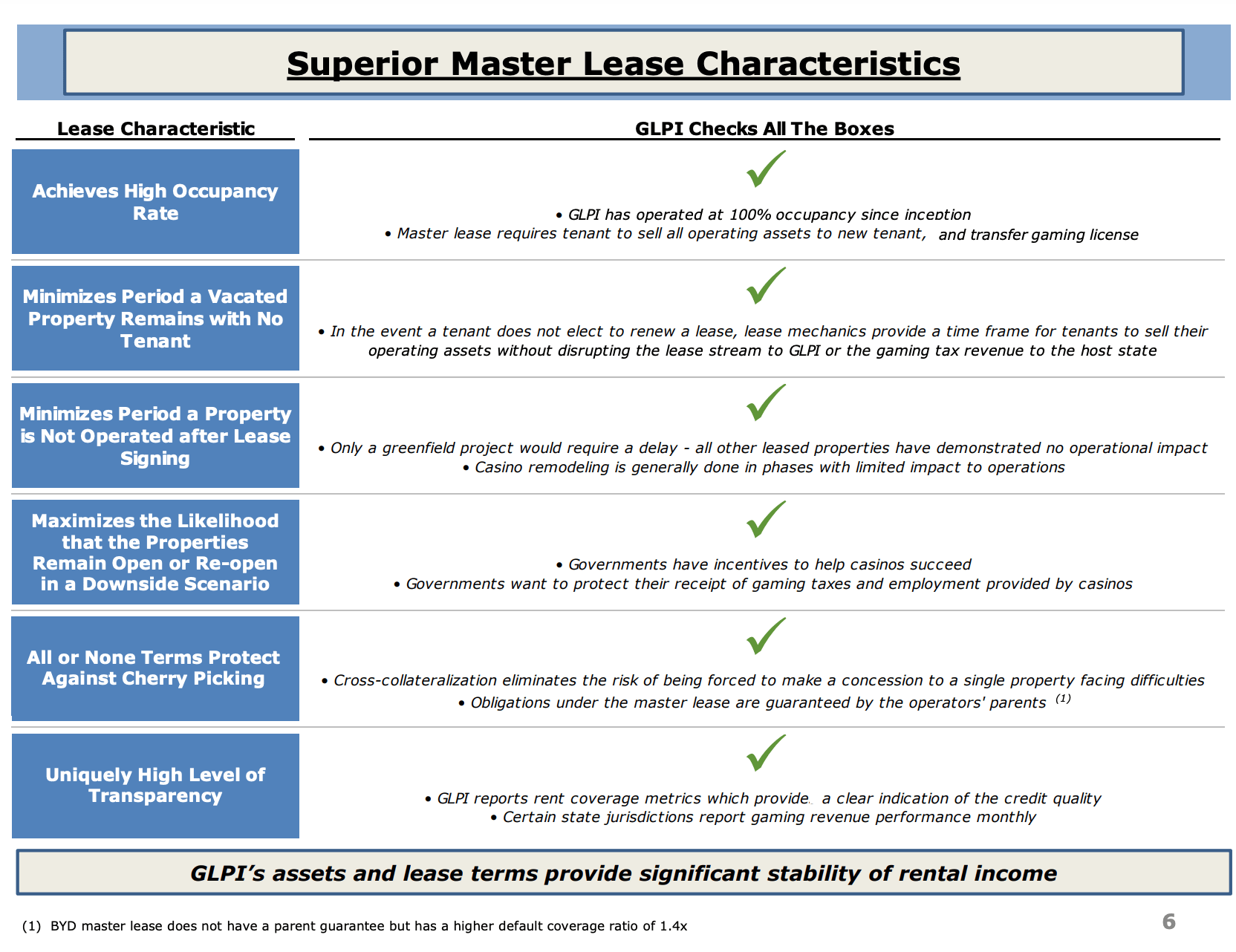

As shown below, GLPI’s leases are structured to ensure tenants make payments even if the tenant ends up in bankruptcy. The master lease structure requires that tenants make good on lease payments on all properties. From the landlord’s perspective, the purpose of a master lease is effectively to prevent the tenant from getting the leases on underperforming properties rejected in bankruptcy court.

Gaming & Leisure Master Leases (Investor Presentation)

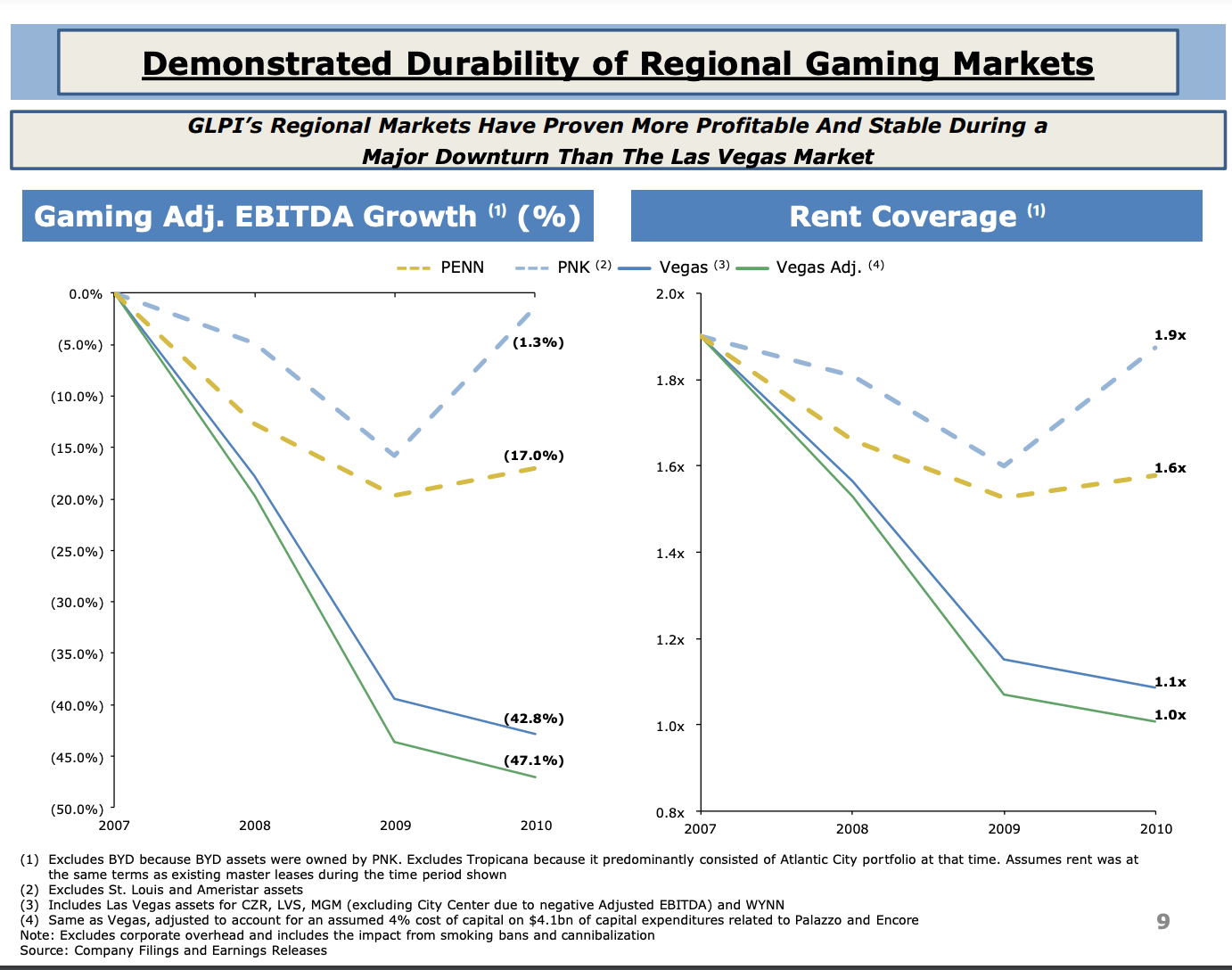

It is also worth noting that regional gaming properties (as opposed to properties on the Vegas strip) have shown to be more resilient during economic downturns. The reason for this is that relatively inexpensive local trips tend to remain in household budgets (while more expensive destination trips like Vegas may get cut). In addition Vegas properties are more dependent on corporate trade-shows and junkets (team-building) events. Lastly, while new casino resorts (or re-developed casino resorts) pop up in Vegas (increasing competition), regional casinos tend to be local monopolies.

Resilience in Past Downturns (Investor Presentation)

Growth – Organic Vs. External

The triple net lease structure makes estimating organic growth fairly straightforward for GLPI. Most of GLPI’s leases are subject to fixed escalators between 1.5-2.0%. While some of GLPI’s leases are linked to CPI, all of these leases have narrow caps and floors which effectively fix rent growth in a narrow band of 0-2% annually.

External growth comes from acquiring properties from casino operators. When GLPI is able to add properties of similar or better quality to its existing portfolio (and with similar or higher annual rent escalators) at higher cap rates than the implied cap rate at which GLPI trades, it is accretive to GLPI’s NAV (net asset value) per share. Similarly the acquisition of properties at lower AFFO multiples (higher cap rates) than its own multiple will be accretive to AFFO per share.

Over the past couple years GLPI has acquired nearly $2 billion worth of properties at cap rates ranging from 6.9-7.6%. While today GLPI trades at an implied cap rate of 6.4% (shown below) and 14.5x AFFO/multiple, at the time GLPI made these acquisitions (and issued shares/units), GLPI traded at a higher implied cap rate (7+%) and lower multiple of AFFO. As such, the value accretion to shareholders from these transactions appears to have been fairly minimal.

Given how well, GLPI’s shares have performed over the past year, the company now trades at just a 6.4% implied cap rate. To the extent that GLPI is able to acquire properties (again of similar/better quality with equivalent or better rent escalation terms) at 7%+ cap rates, it will be able to create value for shareholders through external growth.

One drawback here is that its main competitor Vici Properties (VICI) is also trading at a premium valuation (and is seeking external growth) which means that GLPI is likely to face stiff competition to purchase assets. This is in contrast to other real estate sub-sectors where competition has decreased as the cost of capital has risen (share prices have fallen).

All-in, I expect tepid (3-4%) AFFO growth for GLPI over the medium term.

Valuation

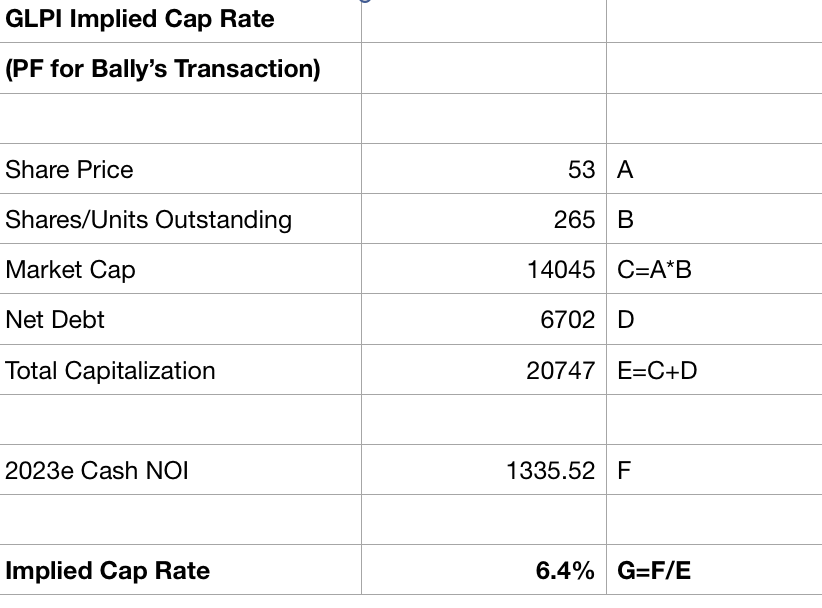

At $53/share Gaming & Leisure appears fully valued at 14.7x 2023e FFO, a 5.3% dividend yield, and an implied cap rate of 6.4% as shown below.

GLPI Implied Cap Rate (Company Filings; Author Estimates)

My cap rate calculation takes into account the most recent acquisition of properties from Bally’s (BALY) by including the NOI (and adding to debt – though we may see GLPI fund more of this deal via an equity issuance).

The 6.4% implied cap rate at which GLPI trades is at the low end (high valuation) of where the stock has traded since coming public in late 2013 (range of 6.3% to 8.2%). GLPI trades at a 15% or so premium to NAV (using a 7% cap rate which could be considered optimistic). This is in sharp contrast to other sub-sectors like apartments and offices which are trading at deep discounts to NAV and offering cap rates at the high end of their historical range (low valuation).

Conclusion

Gaming & Leisure has been a fantastic performer over the past year. While GLPI should produce consistent operating results and dividends, shares trade at a high valuation relative to history while discounts abound throughout the REIT universe. As such, I see GLPI as being relatively unattractive at $53 per share. I see much better value in the heavily discounted apartment and office REITs I’ve recently written about here on Seeking Alpha.

Be the first to comment