4FR/E+ via Getty Images

Background

Galapagos NV (NASDAQ:GLPG) is a Belgium-based commercial pharmaceutical company with multiple commercial and pre-commercial drugs under its belt. 2022 was a big year for the company, with a well-known “star executive,” Paul Stoffels starting as a CEO in April 2022. Paul Stoffels worked as a Chief Scientific Officer at Johnson & Johnson (JNJ) for 10 years.

Paul Stoffels LinkedIn (LinkedIn search)

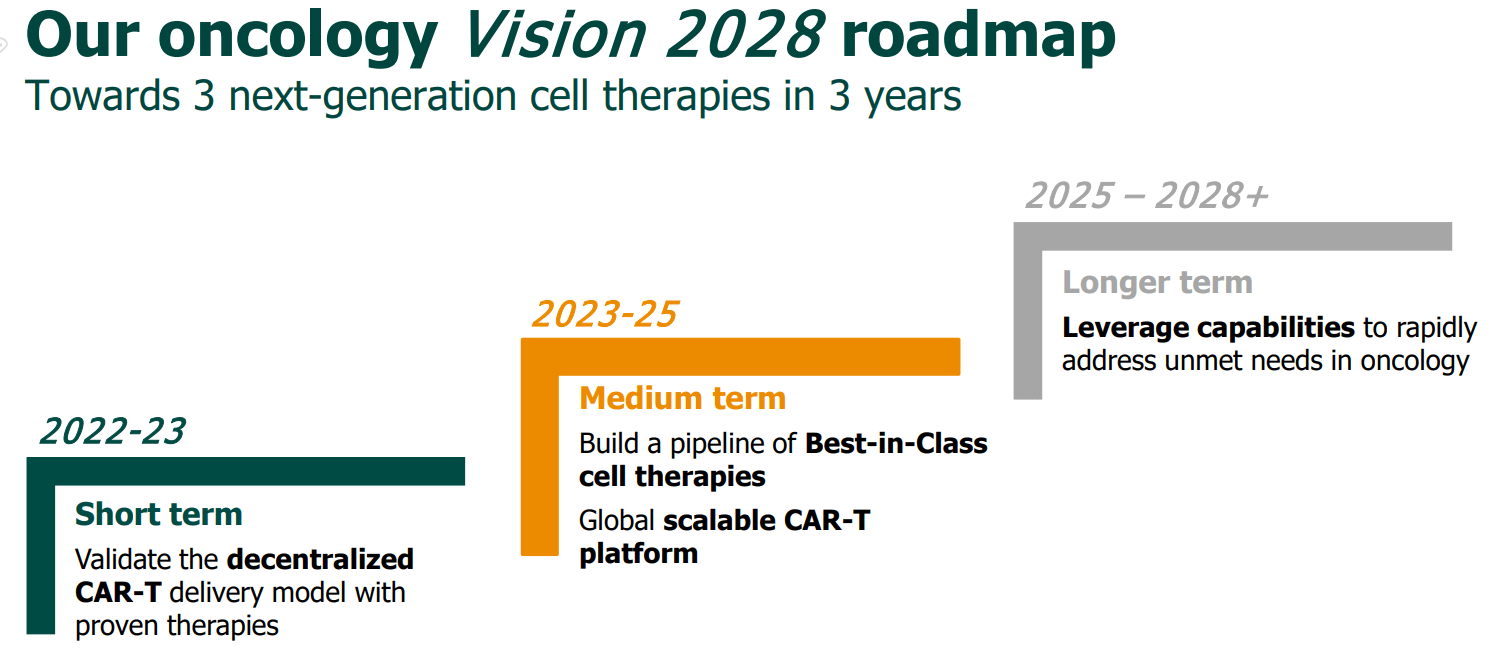

The key focus for the company is on autoimmune and fibrotic indications targeting rheumatoid arthritis, Crohn’s disease, ulcerative colitis, psoriasis, systemic lupus erythematosus, and cystic fibrosis. The company acquired early-stage CAR-T assets (CellPoint and Abound Bio transaction) last year, surprising investors. The CAR-T asset targets CD-19 or BCMA, and the strategy seems to be creating a decentralized CAR-T delivery model and further expanding into a global scalable CAR-T platform.

Galapagos Pipeline Overview (Company)

Company IR deck (Company IR deck)

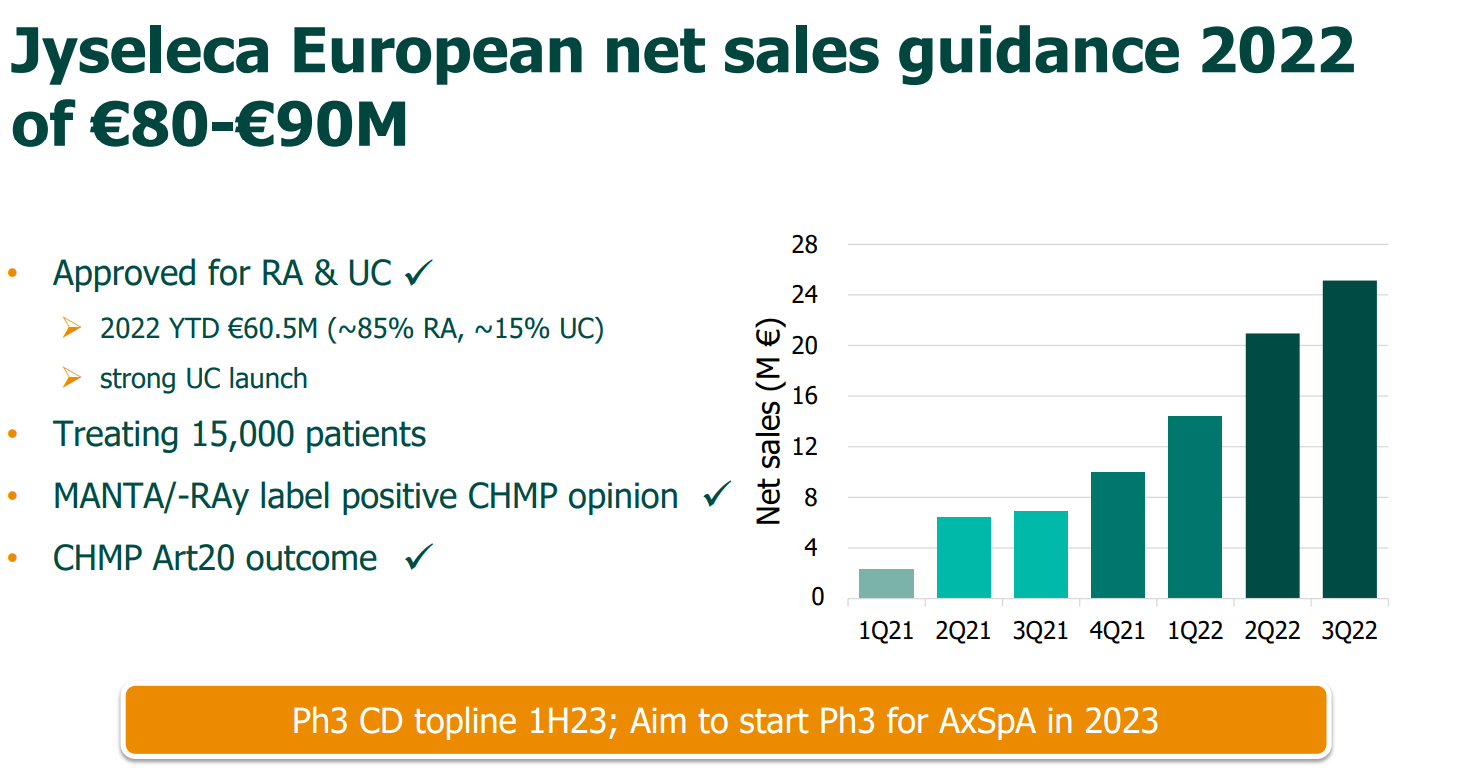

Jyseleca’s sales ramp seems better than expected during 2022

Jyseleca is marketed in Europe but not in the US for RA and UC, the company has increased the guidance twice during 2022, and we expect the sale during 2022 to reach somewhere between EUR 80-90m. Also, the company has received a positive CHMP opinion based on the MANTA/Ray trial and received a cleaner label, which can help with the sales ramp. Furthermore, the management noted that they plan to start phase 3 in AxSpA indication during 2023; if positive, additional indication can add to the current peak sale estimate of $500M.

Company IR Deck (Company IR Deck)

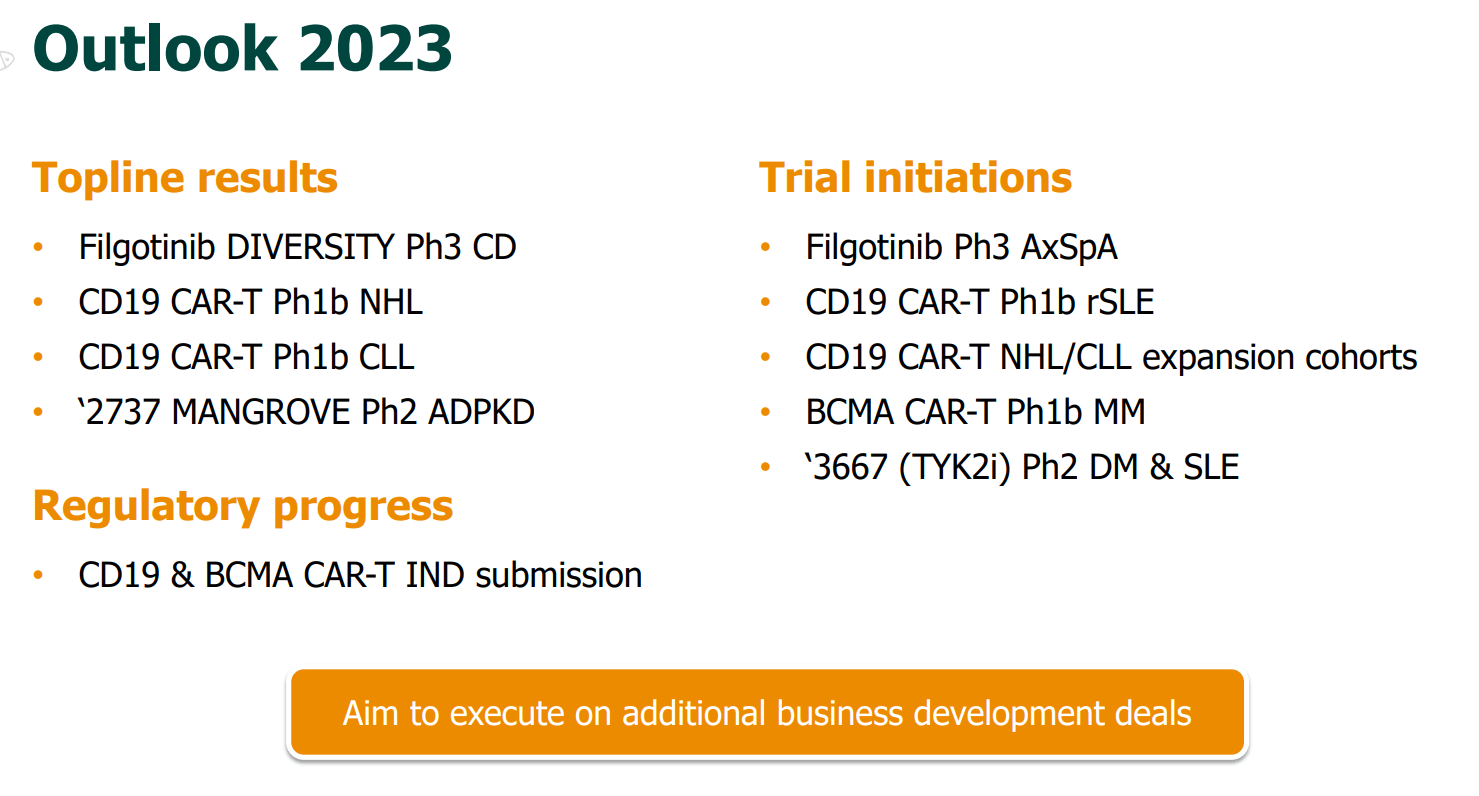

Although 2022 was a relatively quiet year for the company, unlike what some investors hoped for, during 2023, we expect several high-stake catalysts from its Jyseleca franchise as Jyseleca’s DIVERSITY Phase 3 Crohn’s trial data is expected to be released. The company noted that sales from Crohn’s disease are already included in the $500M peak sales guidance from the company; however, depending on the result of the trial, the peak sales could change, which can be a positive surprise for the stock as the market expectation around Jyseleca seems very low at the moment. The company seems to have initiated several BCMA CAR-T-related trials, targeting r/r NHL and r/r CLL, where we expect the data could come out sometime during 2023, albeit we do not see it moving the stock price as much even with the positive data due to early developmental status.

GLPG oncology Vision 2028 roadmap (GLPG oncology Vision 2028 roadmap)

Besides the clinical catalyst, our key thesis revolves around the huge cash reserve (>$4Bn) and the negative enterprise value (-$1.8Bn) of the company. As guided by the company, we expect the management team to make a major business development effort in immunology and oncology, where their focus would be replenishing their clinical pipeline and also leverage their pre-existing commercial force. The key focus of the M&A strategy seems to revolve around acquiring a) 3 cell therapies, b) 2 small molecular therapies, and c) accelerating the early-stage pipeline focusing on oncology and the company’s previous key focus areas, immunology and fibrotic indications. The company seems to be open to various different modalities such as small molecular, cell therapies, and biologics. The company plans to acquire a commercial asset base well to add besides Jyseleca in order to leverage the company’s pre-existing commercial infrastructure as well; the company hopes to add 1 cell therapy drug in multiple indications by 2028.

The key catalysts for Galapagos during 2023

Key catalyst for Galapagos (Company)

Risks

Clinical risk remains as Galapagos has multiple early-stage and late-stage clinical development ongoing. Potential unexpected competition can emerge for Jyseleca’s sales, further putting downward pressure on the expected peak sales. As the company is not yet cashflow positive, there is a potential financing risk if they exhaust all their cash reserve in M&A activity, where they may have to raise additional capital to fund their operation; if this happens, additional shares issued can dilute the value of the existing shares.

Conclusion

We initiate Galapagos with a BUY rating due to a) enormous cash reserve of >$4Bn and negative enterprise value, b) strong management track-record, Paul Stoffels, leading the company, and c) exciting BD deal potential, considering the depressed market condition and many companies desperately needing cash, we believe many great opportunities should emerge for Galapagos to acquire. However, we believe in order for the stock to move meaningfully, a late-stage or commercial asset would be needed, presuming from the lukewarm market reaction to the CAR-T acquisition back in June 2022. Another potential upside would be phase 3 data of Jyseleca coming out in 2023 and Jyseleca’s RA and UC franchise delivering better than expected earnings during 2023.

Be the first to comment