FX Week Ahead Overview:

- The last week of February brings a broad but shallow economic calendar, top heavy with ‘high’ rated events and not much else.

- The Reserve Bank of New Zealand meets for the first time in 2021, and like the other commodity currency central banks, it too may shrug off negative interest rate talk while at the same time complain about FX markets.

- Changes in retail trader positioning suggest that most USD-pairs are on mixed footing.

Starts in:

Live now:

Mar 01

( 11:03 GMT )

Recommended by Christopher Vecchio, CFA

FX Week Ahead: Strategy for Major Event Risk

For the full week ahead, please visit the DailyFX Economic Calendar.

02/23 TUESDAY | 10:00 GMT | EUR Inflation Rate (JAN)

The final January Euroarea inflation rate (CPI) report, the top item of interest for the Euro this week, is due out on Tuesday. According to Bloomberg News, the headline Euroarea inflation reading is due in at +0.9% from -0.3% (y/y), while the core reading is due in at +1.4% from +0.2% (y/y). The sharp rise can be attributed to the statistical base effect thanks to the coronavirus pandemic. With inflation expectations falling precipitously in the past few weeks – since February 3, the 5y5y inflation swap forwards have declined by -9-bps from 1.383% to 1.296% – it seems like the European Central Bank, like the Federal Reserve, will look past any uptick in price pressures.

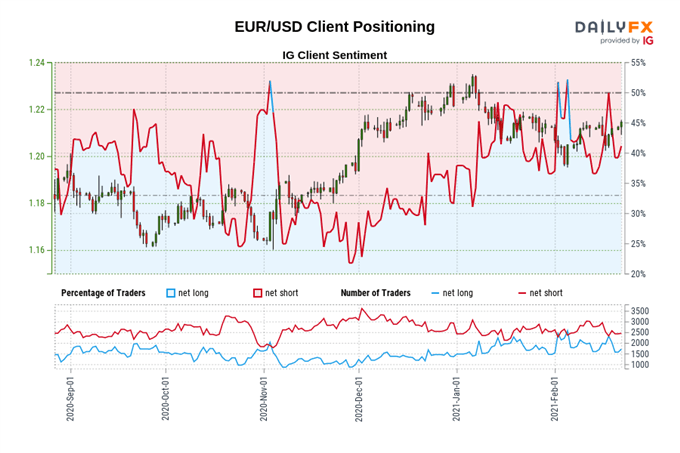

IG Client Sentiment Index: EUR/USD Rate Forecast (February 22, 2021) (Chart 1)

EUR/USD: Retail trader data shows 41.83% of traders are net-long with the ratio of traders short to long at 1.39 to 1. The number of traders net-long is 21.99% higher than yesterday and 5.73% lower from last week, while the number of traders net-short is 9.36% higher than yesterday and 12.27% lower from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-short suggests EUR/USD prices may continue to rise.

Yet traders are less net-short than yesterday and compared with last week. Recent changes in sentiment warn that the current EUR/USD price trend may soon reverse lower despite the fact traders remain net-short.

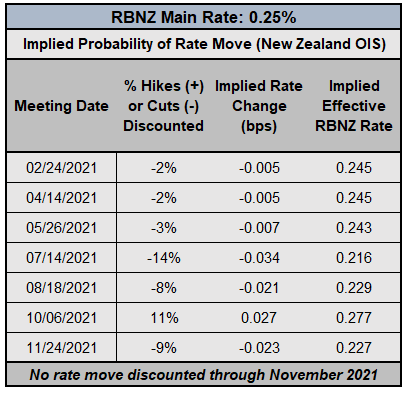

02/24 WEDNESDAY | 01:00 GMT | NZD Reserve Bank of New Zealand Rate Decision

The RBNZ will meet for the first time this year this week. Our end of 2020 expectations for the RBNZ remains valid, as it was made with the understanding that policymakers would not be meeting until the last week of February 2021: “RBNZ Governor Adrian Orr has had to rebuff a government request to include housing prices in the formal policy setting process, which while seemingly benign, suggests that the economy is experiencing a price bubble and thus would not be receptive to even lower (e.g. negative) interest rates.”

RESERVE BANK OF NEW ZEALAND INTEREST RATE EXPECTATIONS (FEBRUARY 22, 2021) (Table 1)

Accordingly, New Zealand overnight index swaps (OIS) are discounting a 3% chance of a rate cut by mid-year, and a 9% chance overall that interest rates could dip to 0% by the last policy meeting of the year. The most likely scenario is that that the main rate will remain at its current level into at least February 2022. If anything, the RBNZ is likely to follow the path set by its commodity currency central bank brethren, which has been to downplay talk of negative interest rates while simultaneously complaining about FX valuations.

02/25 THURSDAY | 12:00 GMT | MXN GDP Growth Rate (4Q’20)

The Mexican economy is highly reliant on its North American trading partners, and surging coronavirus infection rates in Canada and the United States crimped these economies, trading activity declined as the fourth quarter progressed (82% of Mexican exports go to Canada and the US, with the US accounting for 79% alone). But the data received since the first release don’t appear to have moved the needle: according to a Bloomberg News survey, the Mexican economy contracted by –4.5% (y/y) in 4Q’20, in line with the prior update. USD/MXN rates may shrug off the data as traders pay more attention to the movements in US Treasury yields (which has underpinned the USD/MXN rate rally).

02/25 THURSDAY | 13:30 GMT | USD Durable Goods Orders (JAN)

The US economy revolves around consumption trends, given that approximately 70% of GDP is accounted for by the spending habits of businesses and consumers. As such, the durable goods orders reportmake for an important barometer of the US economy. Durable goods are items with lifespans of three-years or longer – from refrigerators and washing machines to cars and airplanes. These items typically require greater capital investment or financing to secure, meaning that traders can use the report as a proxy for business’ and consumers’ financial confidence and health. The preliminary January print is expected to show a gain of +1.1% after the +0.2% gain in December. Like the January US retail sales report, the January US durable goods orders report may surprise to the upside.

02/26 FRIDAY | 13:30 GMT | USD Inflation Rate (JAN)

The January US inflation rate (PCE) report will be released this Friday, and according to a Bloomberg News survey, further stabilization in price pressures is anticipated. Headline inflation (PCE) is due in at +1.3% (y/y) unchanged, while core inflation (Core PCE) is due in at +1.4% from +1.5% (y/y). The likely impact of a base effect could drive headline inflation higher to and through +2% over the coming months; regardless, the Fed seems content to sit on its hands for the foreseeable future.

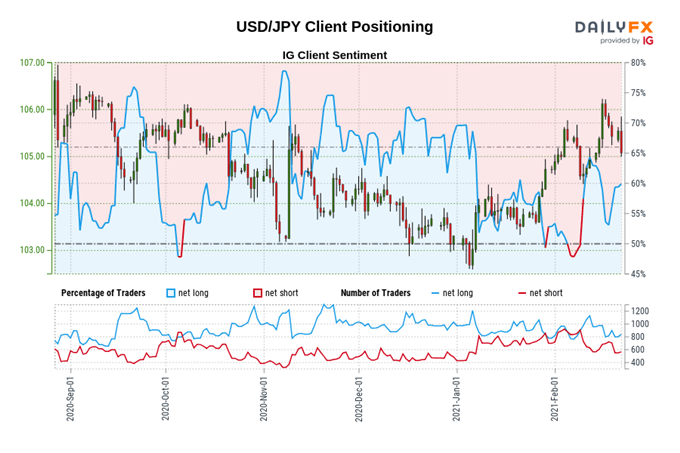

IG Client Sentiment Index: USD/JPY Rate Forecast (February 22, 2021) (Chart 2)

USD/JPY: Retail trader data shows 59.02% of traders are net-long with the ratio of traders long to short at 1.44 to 1. The number of traders net-long is 7.04% higher than yesterday and 14.13% lower from last week, while the number of traders net-short is 8.44% higher than yesterday and 6.93% lower from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-long suggests USD/JPY prices may continue to fall.

Yet traders are less net-long than yesterday and compared with last week. Recent changes in sentiment warn that the current USD/JPY price trend may soon reverse higher despite the fact traders remain net-long.

— Written by Christopher Vecchio, CFA, Senior Currency Strategist

Be the first to comment