peeterv/E+ via Getty Images

Investment Thesis

fuboTV (NYSE:FUBO) is a sports-centric streaming platform. The stock is highly shorted and for good reason too. However, I wonder if FUBO is now too crowded a short?

There are plenty of reasons to be bearish on this stock. And I highlight what investors should think about here. But in the same vein, I don’t believe it’s worthwhile to throw in the towel.

Is fuboTV, A Too Crowded Short?

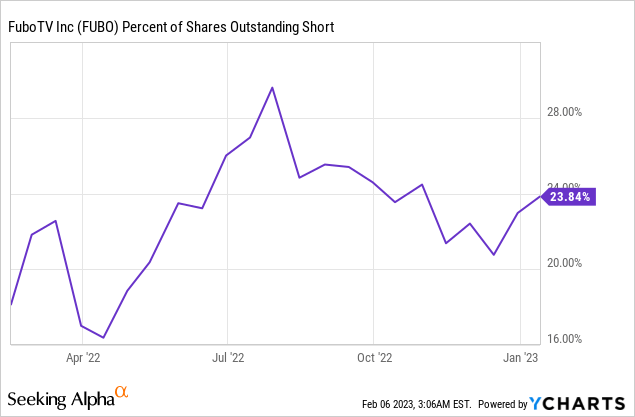

Over 20% of fuboTV’s shares are shorted. In hindsight, it made sense to be short this name, when bulls, such as myself, clamored for the stock.

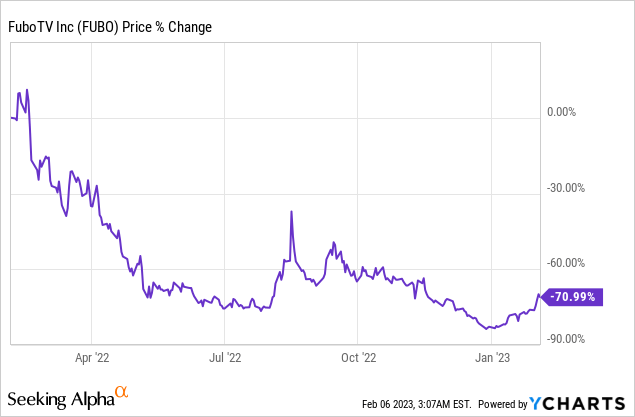

But with the share price already down 70% in the past year and more than 90% from its all-time highs, this brings into focus the key question.

Has fuboTV become too crowded a short? To be clear, there are ample reasons for this stock to be down this much. But that answer avoids the key question, is this now too crowded?

Revenue Growth Rates Fizzled Out

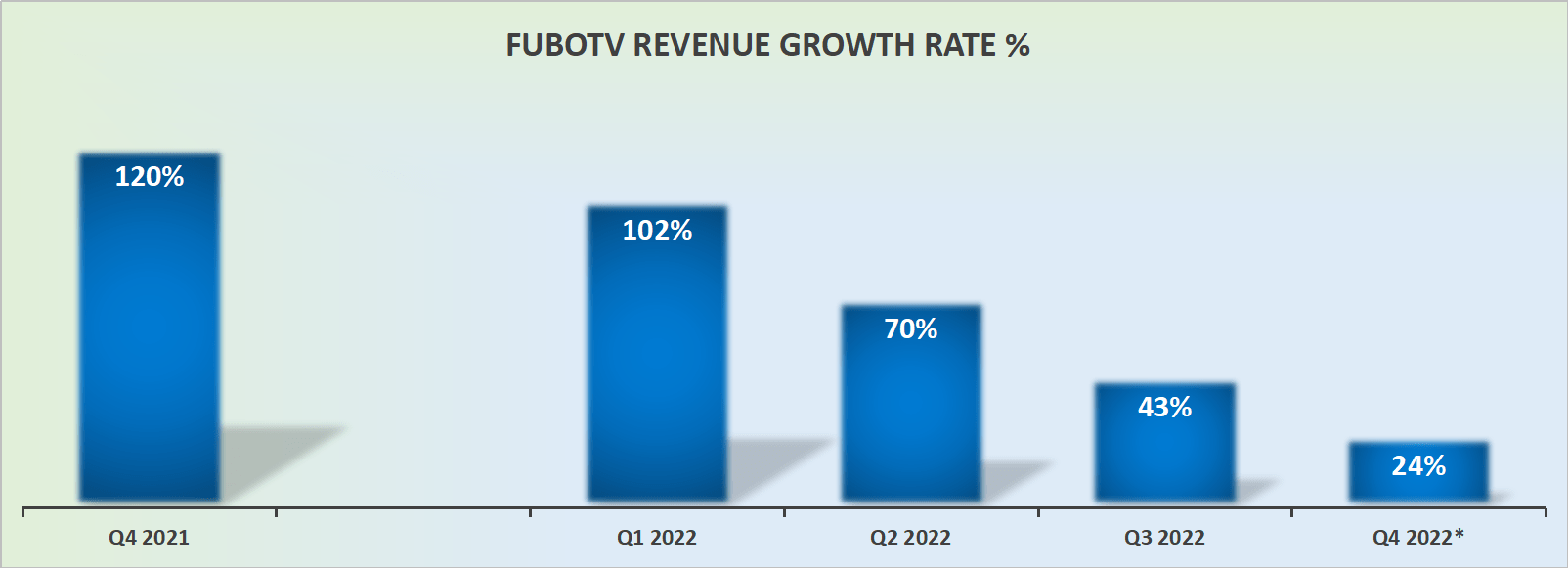

FUBO revenue growth rates

There are several considerations that give the bears ammunition. The fact that the business is seeing its revenue growth rates rapidly fizzle out is clearly consequential.

On other hand, compared to some bigger streaming and advertising platforms such as Netflix (NFLX), Snap (SNAP), and Meta (META), fuboTV is still growing meaningfully faster than any of these names.

So, even if we can all agree that fuboTV’s growth rates are decelerating, I believe that context matters too.

For instance, not only is fuboTV going against tough comparables with the prior year. but also, we shouldn’t be too quick to disregard that the environment in Q4 of 2022 is meaningfully worse than in Q4 2021. Back in 2021, the environment was much more favorable toward fuboTV’s prospects expanding.

Not only was Q4 2022 tremendously more challenging, but we also have to be frank and put forward that the early part of 2023 carries a significant amount of uncertainty.

Put simply, I don’t believe that investors should have any reason to complain about these growth rates. Consequently, having discussed FUBO’s slowing growth rates, let’s now turn to what’s ultimately the key bear case, FUBO’s profitability.

Will FUBO Convince Investors of Its Profitability Prospects?

Now we get to the core of the bear case. FuboTV is a sports-streaming subscription business.

However, despite this being at the core of what fuboTV does, its subscription business was never designed to be profitable.

That side of the business was intended to be a customer acquisition tool, to get subscribers onboard that were highly targeted and sports-fanatic, with enough household income to spend more than $70 per month on streaming sports.

That being said, what fuboTV hoped would be the profit driver had been its advertising opportunity. This was intended to be a fast-growing, highly profitable business unit. With that in mind, consider what fuboTV’s CEO David David Gandler said at a recent conference call,

I think for Q1, it’s tough to tell, because we’re only like nine days in [to Q1 2023], but when I look at the first nine days of last year versus the first nine days of this year, I am like, not so exciting.

So, this yet again reinforces the bear case. More specifically, fuboTV’s supposedly crown jewel is struggling to gain traction. And if that side of the business cannot support the whole business, investors are going to rapidly turn their focus to fuboTV’s balance sheet once again.

More specifically, fuboTV has roughly $400 million of convertible debt. Given that the business is not generating positive free cash flows unless fuboTV finds some way to convince investors that it can be profitable, it will struggle to refinance those $400 million worth of convertibles.

Given that its market cap is around $580 million, this would imply that fuboTV would be forced to dilute shareholders by 100%. Which would clearly cap investors’ potential upside.

The Bottom Line

My core argument is this, things for fuboTV are looking dire. The business’ balance sheet is highly restrictive. And on top of that, what was supposed to be the crown jewel for fuboTV, its high-margin advertising business, appears to have hit a rough patch.

All that being said, I question whether all this bad news isn’t already in the price? Put another way, what new bad news could possibly surface in the coming months that isn’t already priced into the share price?

Personally, I believe that shorts have overstayed their position. Hence, I don’t believe that this is the best time to throw in the towel.

Be the first to comment