jetcityimage/iStock Editorial via Getty Images

Momentum in the electric-vehicle business could drive stronger than expected earnings results for Ford Motor Company’s (NYSE:F) fourth quarter. The release is scheduled for February 2, 2023 (post-market).

The car brand ended FY 2022 with soaring sales in the electric vehicle (“EV”) segment, especially for the Mustang Mach-E sport utility vehicle, as consumers continue to gravitate towards Ford’s expanding EV line-up. The adjusted EBIT and free cash flow outlook for FY 2023, however, is likely going to be below FY 2022 levels due to sticky inflation and risks to economic growth. Weakening consumer spending in a high-inflation world is also a risk factor that could weigh on Ford’s guidance for FY 2023!

Positive short-term EPS trend

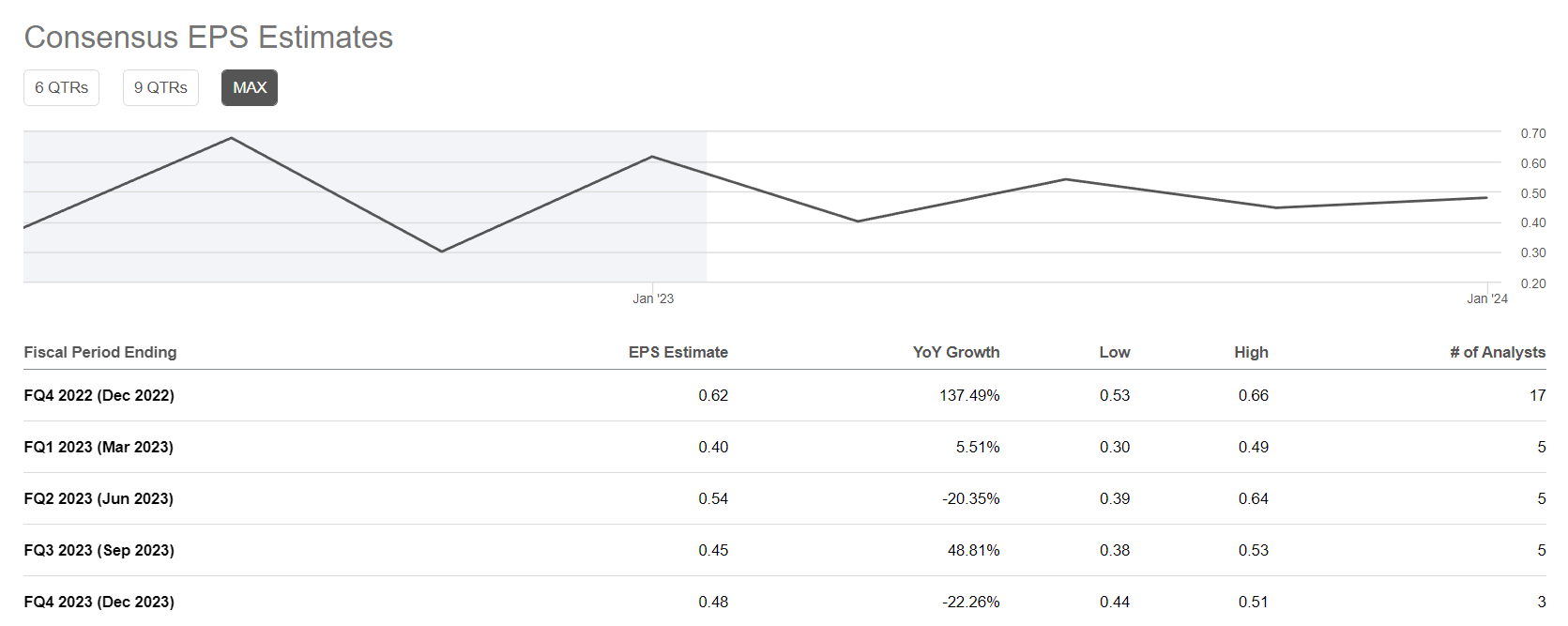

Ford is set to submit its earnings sheet in a little more than a week, and the expectation is for the car brand to have generated earnings of $1.98 in FY 2022. The average EPS prediction implies 25% growth compared to the year-earlier period. The estimated trend is positive for Ford heading into its earnings report, with FY 2022 EPS upward revisions outnumbering downward revisions by a ratio of 4:3.

For Q4’22, analysts expect $0.62 per in EPS, which translates to about 137% year-over-year growth.

Seeking Alpha

Ford’s EV sales are soaring

Ford has a good chance, I believe, to beat EPS expectations chiefly because electric vehicle sales are booming and the company has considerably improved its electric vehicle lineup through a number of new product releases in FY 2022. The car brand sold 2,359 F-150 Lightning pickup trucks in the U.S. in December, showing a month-over-month increase of 14% (the Lightning truck didn’t yet sell in the year-earlier period). By far the best-selling EV vehicle for Ford is the highly popular Mustang Mach-E SUV, of which the car brand sold 4,775 models in December, showing an increase of 103% year-over-year. The e-Transit, Ford’s electric vehicle flagship in the commercial van segment, sold 689 units in December compared to 654 units sold in November (the e-Transit also launched in FY 2022, so comparable figures for the year-earlier period are not available).

Ford sold 7,823 electric vehicles in December, showing 223% growth over the year-earlier period. Ford’s total electric vehicle sales in FY 2023 amounted to 61,575 units, showing 126% growth. EV-related revenues, according to Ford, grew at twice the rate of the overall segment.

Ford

Mark-to-market loss for EV investment

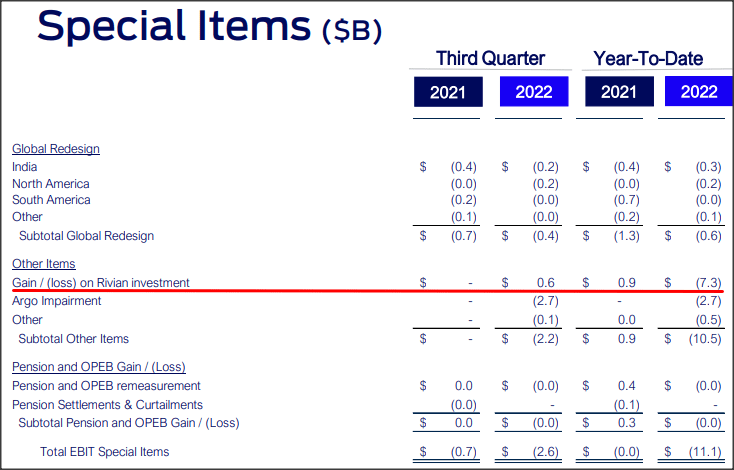

Ford made an initial $500M investment in EV start-up Rivian Automotive, Inc. (RIVN) in 2019, but Rivian has seen a steep decline in its market cap in FY 2022. Ford booked a loss of $7.3B on its investment in the EV start-up in the first three quarters of 2022, and since Rivian’s stock price declined 44% in Q4’22, Ford is set to report yet another impairment loss on its EV investment.

Ford

Everything depends on Ford’s FY 2023 outlook

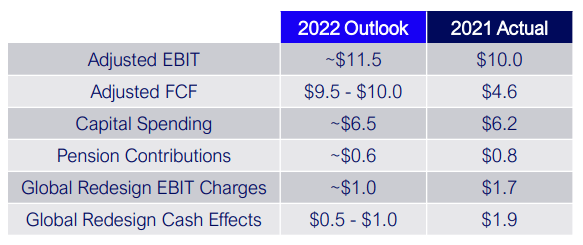

Ford has guided for adjusted EBIT of $11.5B and free cash flow of between $9.5 and $10B for its 2022 financial year. Ford drastically increased its free cash flow guidance in FY 2022 due to rising prices, a recovery in wholesale volumes, as well as strong momentum in the electric vehicle segment.

Ford

For FY 2023, I expect a sequential decline in both adjusted EBIT and free cash flow because inflation poses a serious threat not only to the level of input costs Ford is forced to absorb (which is set to weigh on margins), but also to consumer demand. With consumers remaining under pressure from rising prices and the US likely facing a recession this year, the operating environment may become much more challenged. I estimate that Ford will be able to generate $9.5B to $10.0B in adjusted EBIT and $8.0 to $9.0B in free cash flow in FY 2023.

Ford’s valuation

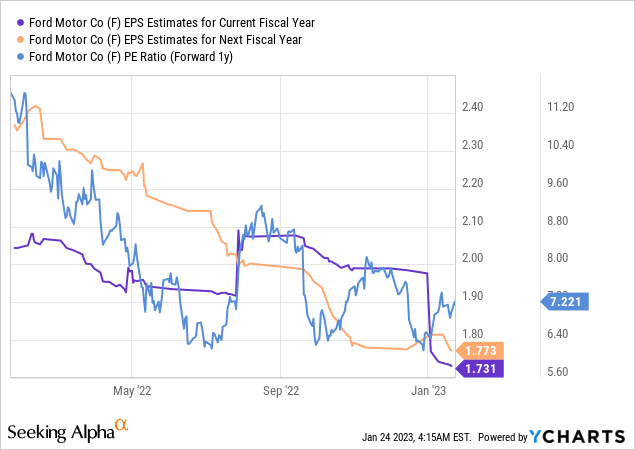

Ford’s shares are superficially cheap, based off of expected earnings for FY 2023, but the risk of a recession is, in my opinion, more severe than the market acknowledges. The earnings estimate trend for FY 2023 is negative and implies a 13% decrease in EPS compared to FY 2022. Based off of earnings, shares of Ford are valued at a P/E ratio of 7.2 X, but Ford’s earnings are highly cyclical and a decline in auto sales as well as contracting wholesale volumes have the potential to reset Ford’s P/E ratio to the up-side.

Risks with Ford

Ford is seeing strong momentum for its newest electric vehicle products such as the F-150 Lightning, the Mustang Mach-E SUV, and the E-Transit. However, electric vehicles still represent only a small portion of the car brand’s total revenues (4.4% in December). Considering that inflation poses a significant challenge to Ford’s cost base and consumer spending (which could create a demand problem for Ford), I believe the biggest commercial risk for Ford right now is a sequential drop in auto sales, with the exception of the electric vehicle segment. A weak outlook for FY 2023 may also weigh heavily on Ford’s shares in February.

Final thoughts

Ford Motor Company could crush EPS expectations for FY 2022 due to strong execution in the electric vehicle segment. However, the FY 2023 outlook could dampen investors’ excitement and the market has to expect a weaker adjusted EBIT and free cash flow outlook due to growing cyclical earnings risks for Ford. While the stock appears cheap based off of earnings, I believe investors are currently underestimating macroeconomic risks for the car brand. While I expect a robust earnings sheet for Q4’22, the earnings estimate trend for FY 2023 indicates that tougher times are ahead for Ford!

Be the first to comment