Vera Tikhonova

Ford knocks the ball out of the park

Ford Motor Company (NYSE:F) just dropped an SEC 8K detailing the outstanding sales numbers regarding electric vehicles (“EVs”) and truck sales. You can read the actual SEC *K filing here. The Seeking Alpha News team actually did a great job of highlighting the important points in a recent post as well:

Ford Motor Company (F) highlighted gains in EV market share and strong truck sales in a sales update on Thursday.

According to a company data release on Thursday, the Michigan-based auto manufacturer sold 179,279 vehicles in the month of December, up from 173,740 in December 2021. However, that figure brought full-year sales to 1.86M, short of the 1.91M sold in the prior year.

That said, the automaker was able to maintain strong truck sales and accelerate EV gains. December truck sales jumped 10.9% from the prior year to 101,649 and leapt to 653,957 sold in the full year. F series truck sales were cited as outpacing the next-closest competitor in the GM (GM) manufactured Chevrolet Silverado by more than 140,000 units.

For EVs, sales more than doubled in the full-year to 61,575 vehicles. Ford is now in second place, behind Tesla (TSLA), in terms of EV sales in the US.

Much was accomplished in 2022, with Ford increasing its share of the industry by 0.7 percentage points. Delivering on our strategy, share expansion came from broad- based growth from our SUV lineup and our all-new EVs growing at twice the rate of the overall EV segment,” he said. “With a strong retail order bank, Ford is well positioned heading into 2023.”

So Ford is gaining market share in the EV space and truck sales are up huge with the Ford F150 being the #1 selling truck for 2022 as well. Yet, sales are actually down year-over-year slightly. The company stated they doubled their EV market share as well, which is very admirable. So sales look excellent presently. Plus, the stock has recently bounced off major support.

Ford stock showing signs of a trend reversal

In my last update, I stated that I would need to see a trend reversal prior to reinvesting in the name. I currently have Ford on my watchlist.

Finviz

Looking at the current chart, the first inklings of a trend reversal seems to have begun. Although, I will need to see the stock break through major resistance at the 50-day SMA before I start getting excited. Looks good technically, but we aren’t there just yet. Ford stock is still down huge and underperforming the market substantially.

Finviz

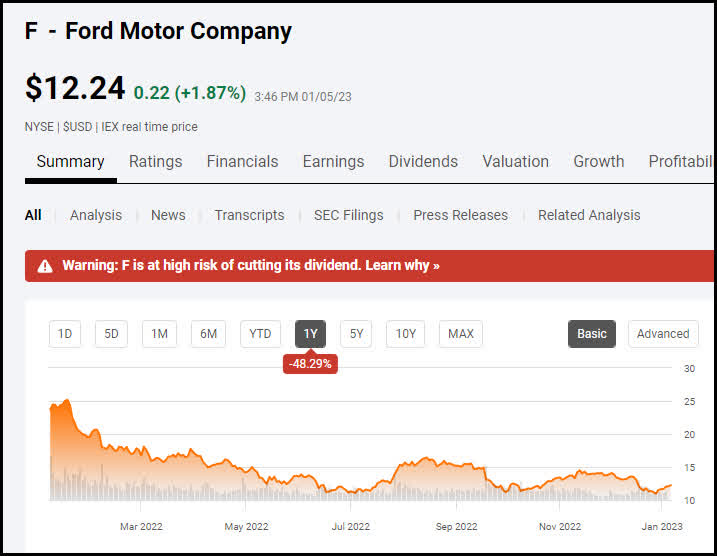

Ford down 50% on the year

The stock is down 50% on the year. So, some long-term Ford holders may be deep underwater. If I was, I would not sell out at this time. I’m not buying in yet… but wouldn’t sell out at this point if I was long, more on this later. Ford has actually began performing much better over the second half of 2022.

Seeking Alpha

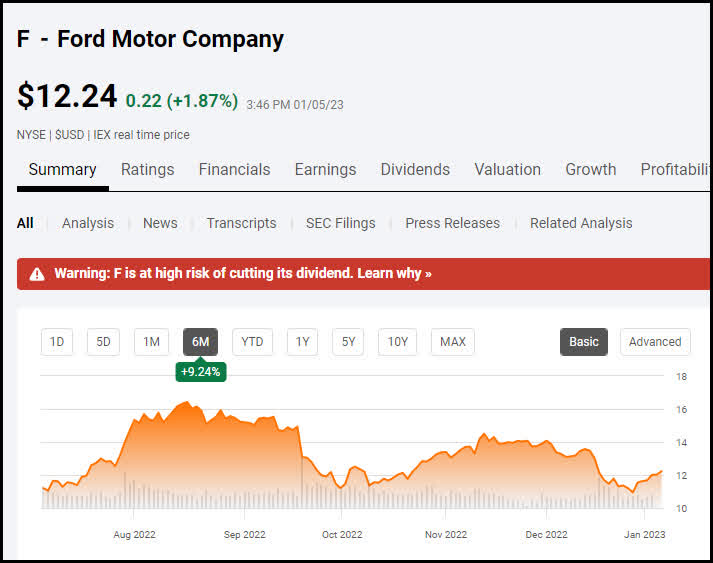

Ford up 10% over last 6 months

Ford’s stock is actually up 10% over the last 6 months. This is quite admirable based on the volatile markets we have been exposed to as of late. This is because they are showing signs of turning the company around. I love Ford CEO Jim Farley and believe he will make it happen at some point, it may just take a while longer. Seeking Alpha has a BUY rating on the stock based on the quantitative metrics as well.

Seeking Alpha

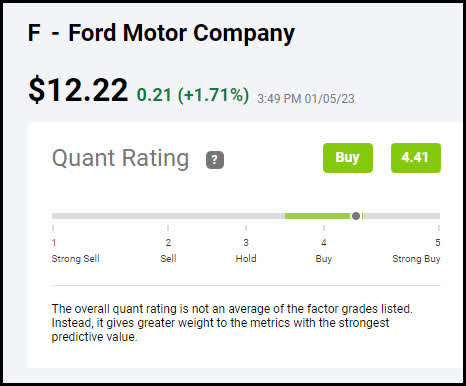

Ford scores an A – BUY – Quant rating

Seeking Alpha’s quantitative metrics tool is awesome. I don’t always agree with what it comes up with due to the fact I am somewhat of a contrarian investor and often look to buy stocks when they are in trouble, which more often than not leads to a SELL quant rating. Nonetheless, Ford scores an A. Let’s take a look at why.

Seeking Alpha

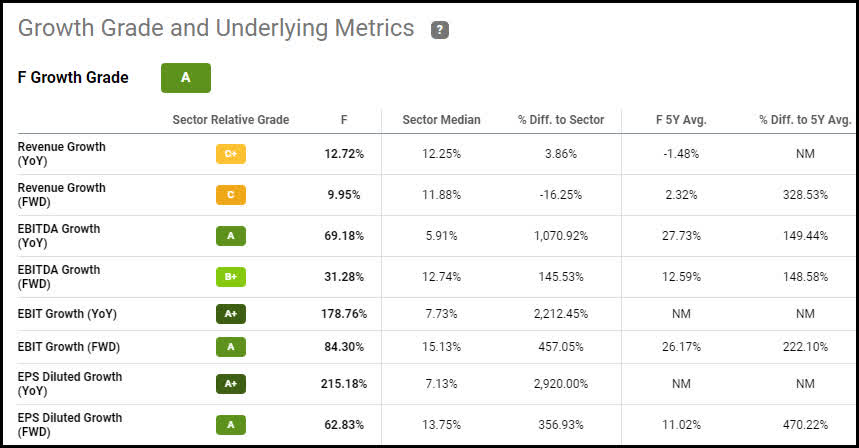

Ford’s EBITDA growth is the primary factor

EBITDA stands for “earnings before interest, taxes, depreciation and amortization.” It is the primary measuring stick when assessing a company’s financial wellbeing and ability to generate positive free cash flow.

Seeking Alpha

Ford is crushing it as far as EBITDA growth, yet is doing not so great as far as revenue growth. This is because Farley and company are in the process of pruning the company of weak selling and less profitable vehicles. So revenues are going down, yet profits are up. This is a good thing. Nevertheless, it shows the company is still in the midst of a turnaround. They haven’t reached the other side of the rainbow just yet, so to speak. Another positive for the company is the rock-bottom valuation.

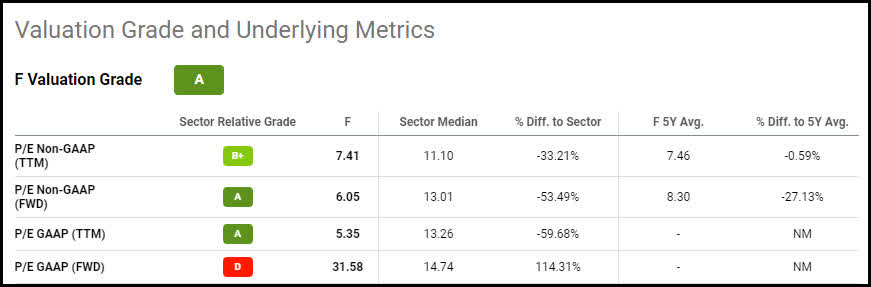

Ford is vastly undervalued

Ford is vastly undervalued on a historical and comparative basis.

Seeking Alpha

Ford shares are selling at a 53.49% discount to its peers on a forward basis and at a 23% discount to its historical 5-year average valuation. The stock is currently trading with a forward P/E ratio of 6.05 versus the five year average of 8.30. So we can check the growth and valuation boxes off. Further, the technical status is improving as well. Now, let’s turn our attention to the most important piece of the puzzle, the dividend.

Ford dividend status

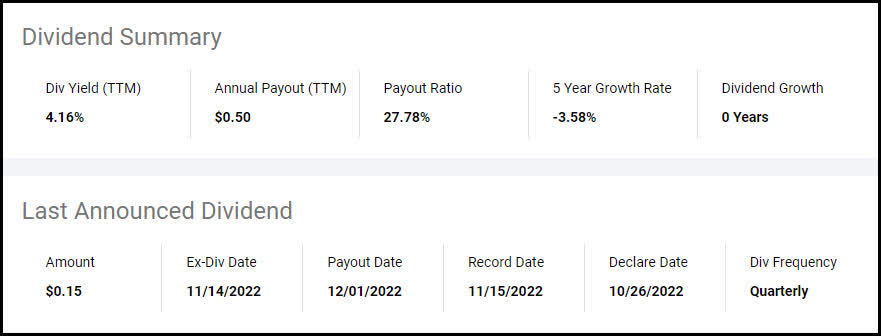

Ford currently pays a dividend with a yield of 4.16%. A few years ago, I would have jumped at the chance to lock in a 4% yield. Yet, today, you can get a risk-free 4% yield by buying a CD. So, I would need to have confidence that the dividend is well-covered, the stock has the potential for substantial upside, and is in an uptrend. What’s more, Seeking Alpha’s quantitative dividend grades aren’t so compelling, either. Let’s dive in and see what the issues are.

Seeking Alpha

Ford dividend grades

Ford’s dividend fails on the three most important metrics; safety, growth, and consistency. It scores an A on yield, though. Let’s dig deeper.

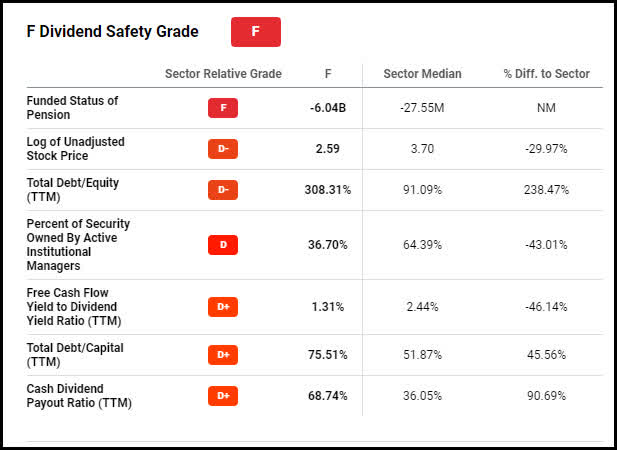

Dividend Safety F

On the dividend summary, it was showing the payout ratio as a mere 27%. That would tend to give you a warm fuzzy feeling, as if there was plenty of cash to go around. Yet, that was on a GAAP basis. When analyzing the Ford dividend payout on a cash flow basis, it comes in at 68.74%, which is high with so much uncertainty ahead. Plus they score an F for consistency.

Seeking Alpha

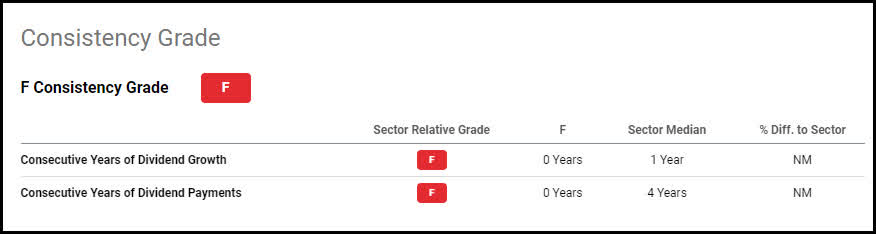

Ford dividend consistency scores an F

With the company just recently suspending the dividend, it’s easy to see why they get a poor consistency score.

Seeking Alpha

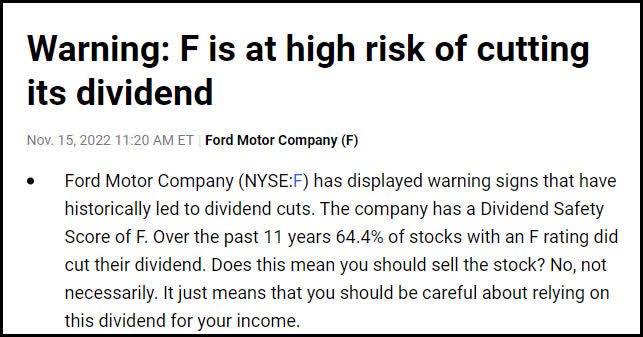

This, combined with several other factors, has led Seeking Alpha’s quant team to issue a dividend cut warning.

Seeking Alpha warns of potential dividend cut

Below is the warning released by Seeking Alpha. You can view the actual page here.

Seeking Alpha

Seeking Alpha lists off seven major factors as to why Ford may have to cut the dividend.

Seeking Alpha

Even so, I do not anticipate the company cutting the dividend. I believe that would be a killer for Ford stock, and management knows that. I think they would take out additional debt to pay the dividend if they had to at this point. So what is stopping me from jumping in the stock right now? Let’s me conclude with my explanation

Investor Takeaway

Ford is definitely making good progress and appears to be turning the ship around. Nevertheless, I need to see the stock actually break out above strong resistance at the upper level of the current downtrend channel. Furthermore, the current “recession indicating” 3 month to 10 year yield curve is inverted by 0.90.

CNBC

This is the largest spread in 22 years. I see little chance we are going to be able to get through the first half of 2023 without having some semblance of a recession. This will cause people to hold off on making new vehicles buys and other major outlays as they hunker down financially. I am still in a wait-and-see mode as far as starting a new position in Ford stock. We could see further downside if the recession comes to fruition.

Plus, it’s been a seller’s market over the past year regarding vehicles. Low supply and huge demand have given pricing power to the car dealerships. Yet, I see that as about to change. I have already noticed that there are new car and truck commercials offering discounts once again. This, coupled with a looming recession, has me in wait-and-see mode presently. Those are my thoughts on the matter. I look forward to hearing yours. Is Ford a BUY right here?

Be the first to comment