ArtistGNDphotography

Thesis

First Solar (NASDAQ:FSLR) has seen renewed investor interest due to the passage of the Inflation Reduction Act. The business is positioned well strategically and avoids some of the issues associated with silicon-based solar panels. Despite this, we believe that too much growth is priced into the stock and that shares do not look attractive at these levels.

Inflation Reduction Act

According to the White House website,

For the first time ever, the Inflation Reduction Act establishes Make it in America provisions for the use of American-made equipment for clean energy production. The law provides expanded clean energy tax credits for wind, solar, nuclear, clean hydrogen, clean fuels, and carbon capture, including bonus credits for businesses that pay workers a prevailing wage and use registered apprenticeship programs.

Fortunately for First Solar, they are one of the only domestic solar panel producers and are in a prime position to benefit from this type of government support. This made in America provision of the IRA plays right into the strategic advantage that First Solar has over their foreign competitors.

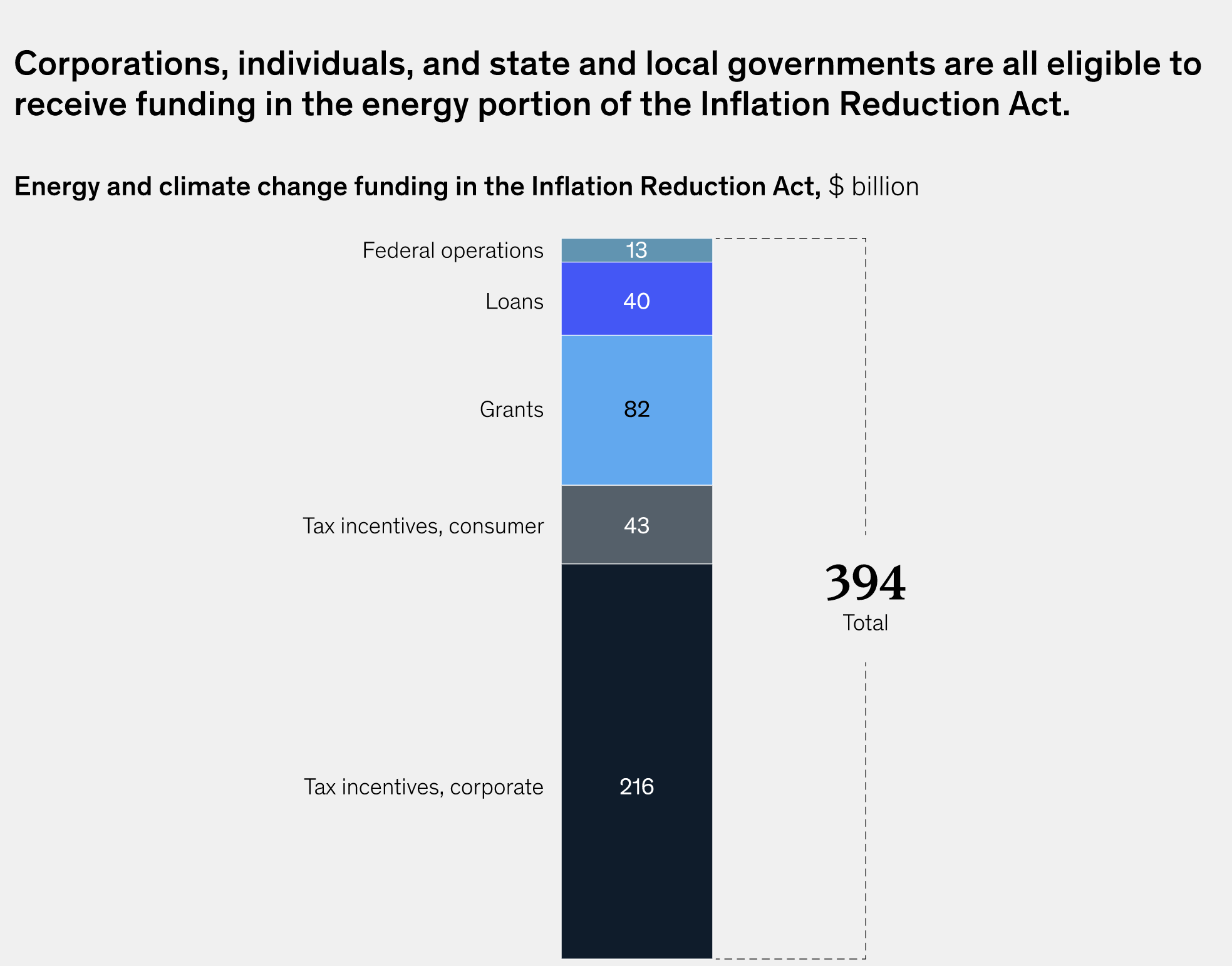

McKinsey made a visual that shows the investment incentives that the IRA provides to companies, individuals, and state and local governments.

IRA Investment Incentives (McKinsey)

These incentives will not only help First Solar, but they will also help their customers. This will likely increase the long-term demand for First Solar’s solar panels, as well as strengthen the company’s financial position.

Strategic Positioning

The two main components of First Solar’s strategic positioning are their domestic importance and the specific technologies that they use when creating their solar panels.

Domestic Importance

The made in America provision of the IRA shows how much the government wants to improve the US’s domestic manufacturing capabilities. As tensions increase between the US and China, the US is at risk of being cut off from the supply of solar panels. If domestic manufacturing capabilities do not improve, the green energy transition will result in the US going from being energy independent to being dependent on China for energy. That seems like a strategic misstep, and one that the US is trying to remedy with the IRA. Domestic manufacturing will likely be the target of future legislation, and First Solar is well positioned to benefit from government assistance. Along with assistance, the government may be willing to act as a financial backstop or buyer of last resort. In a way this makes First Solar “too important to fail”.

Cadmium Telluride (CadTel) photovoltaic (PV) technology

First Solar uses Cadmium Telluride technologies as opposed to the more popular crystalline silicon methods. On their website First Solar states:

Energy Yield Advantages

Superior Warranted Annual Degradation Rate

Modules retain >89% of original performance after 30 years

Superior Temperature Coefficient & Spectral Response

Delivers up to 4% more annual energy in hot climates and up to an additional 4% more annual energy in high humidity conditions

Superior Shading Response

Less sensitive to power loss in shaded conditions

Immunity to Cell-Cracking, LID & LeTID

No power loss from cell-cracking and no power loss from LID or LeTID mechanisms that affect c-Si modules

Environmental Advantages

Upcycles mining waste tailings to create an inherently sustainable, high-efficiency photovoltaic semiconductor

Lowest Carbon & Water Footprint

2.5x lower carbon footprint and 3x lower water footprint than c-Si panels on a lifecycle basis

Fastest Energy Payback Time

2x faster than c-Si panels

Superior Recyclability

Global recycling services can recover >90% of materials for reuse

First Solar believes that their technology is superior than their competitors (and so do I), but there are always two sides to the story. First Solar has a clearly differentiated product that buyers (Especially those based in the US) may view favorably to the competition.

Price Action

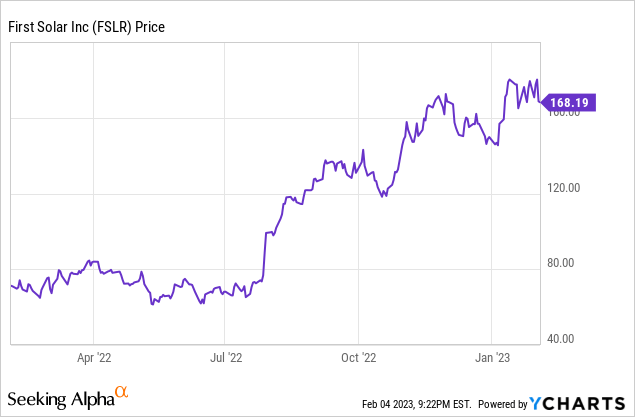

First Solar has been on a tear ever since the IRA passed. Investors have an increased appetite for green energy investments and there is considerable hype around the sector. Hype around a sector increases the risk that companies within that sector are overprices, and we believe that First Solar has too high of growth priced into the shares.

Valuation

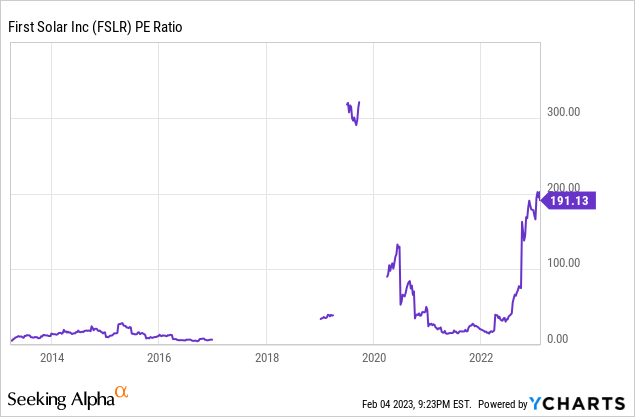

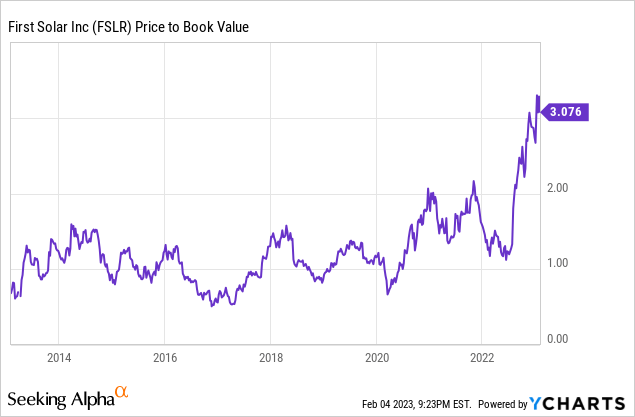

There is no question that First Solar is a well-positioned company within the solar industry. That being said, the company is pretty expensive when looking at traditional valuation metrics such as P/E and P/B ratios. Earnings can be volatile in the cyclical manufacturing sector so P/E is a questionable metric to use, however when looking at P/B it becomes clear that First Solar is trading at a decade-high valuation. This valuation may be warranted, however we believe that investors are expecting far too much growth from the company. Despite the positives surrounding the company we think investors can sit on the sidelines and wait for a better entry point.

Risks

A risk to this neutral thesis is First Solar achieving rapid earnings and revenue growth. This would validate the market’s pricing of the company and we would be wrong. I personally have liked the company for many years; however, the energy/commodity sector can be highly cyclical and at times brutal to invest in, and green energy is no different. Such enthusiasm by the market is often overdone, especially in green energy. Take a look at the stock price of First Solar back when it was trading around $300 a share in 2008 and the ensuing years of disappointment. Investments in companies that operate in volatile sectors (especially when there are low margins) should be met with caution and now seems like a time to be cautious on First Solar.

Key Takeaway

First Solar appears to be a solid company that has done well to strategically position itself within the market. That being said, investors can get ahead of themselves and price in too much future growth for a company. We believe that investors can sit on the sidelines and wait for a better entry point.

Be the first to comment