beekeepx/iStock via Getty Images

The Federal Funds rate was raised another 50 basis points on December 14, 2022, bringing the effective Federal Funds rate up to 4.33 percent.

Here is what the path of increases for the Federal Funds rate looks like for the year of 2022.

Effective Federal Funds Rate (Federal Reserve)

The trajectory of this rate is what the market and the press have been focusing on this year.

And, the path upward in the rate is quite impressive.

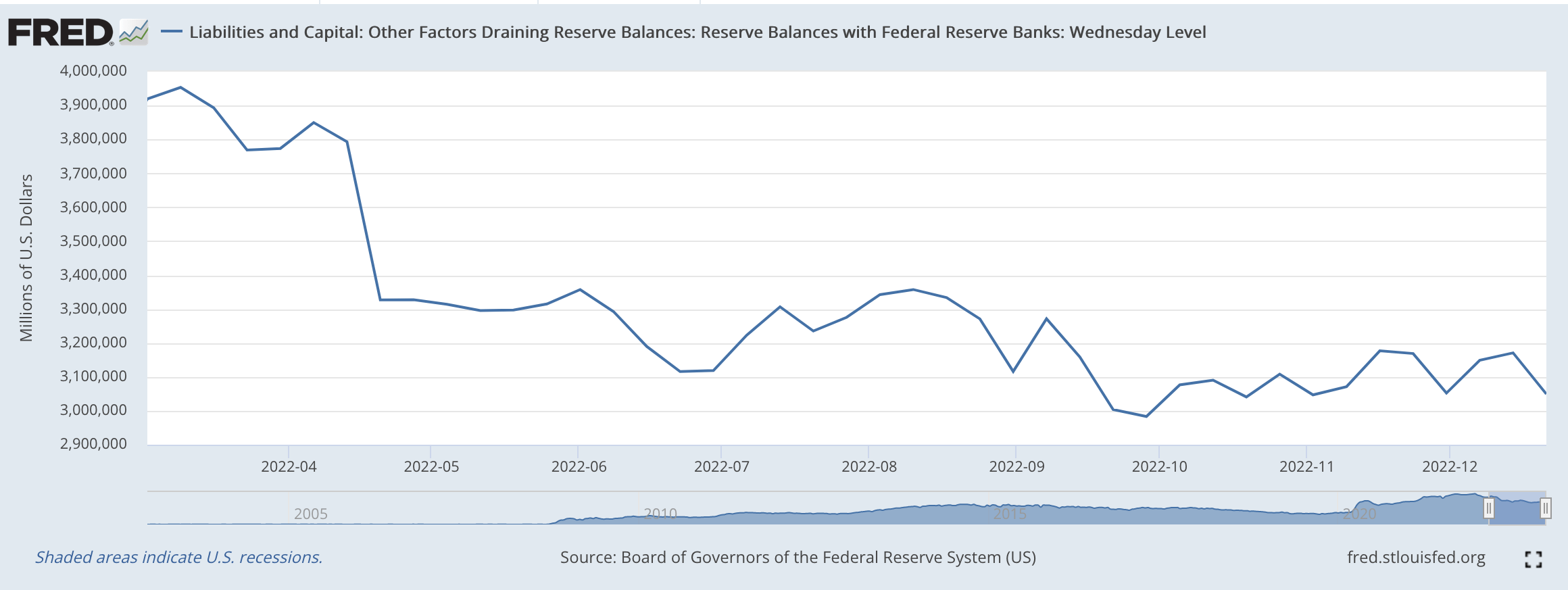

The thing I believe that the market and the press need to look at is the rise in Reserve Balances with Federal Reserve Banks from the balance sheet of the Federal Reserve, which can be observed in the Fed’s weekly H.4.1 statistical release.

Reserve Balances with Federal Reserve Banks can be used as a proxy for the excess reserves in the banking system.

If Reserve Balances decline, it is a sign that there is less liquidity in the banking system, and this factor supports the Fed’s efforts to raise the Fed’s policy rate of interest, the Federal Funds Rate.

Reserve Balances With Federal Reserve Banks (Federal Reserve)

As can be seen from the chart, the “excess reserves” of the banking system have been declining.

In fact, since March 16, 2022, Reserve Balances with Federal Reserve Banks have declined by $844.1 billion.

This is quite a sizeable amount, and the decline supports the Federal Reserve actions to tighten up its monetary policy and raise interest rates.

So far, so good.

The Crucial Policy Variable

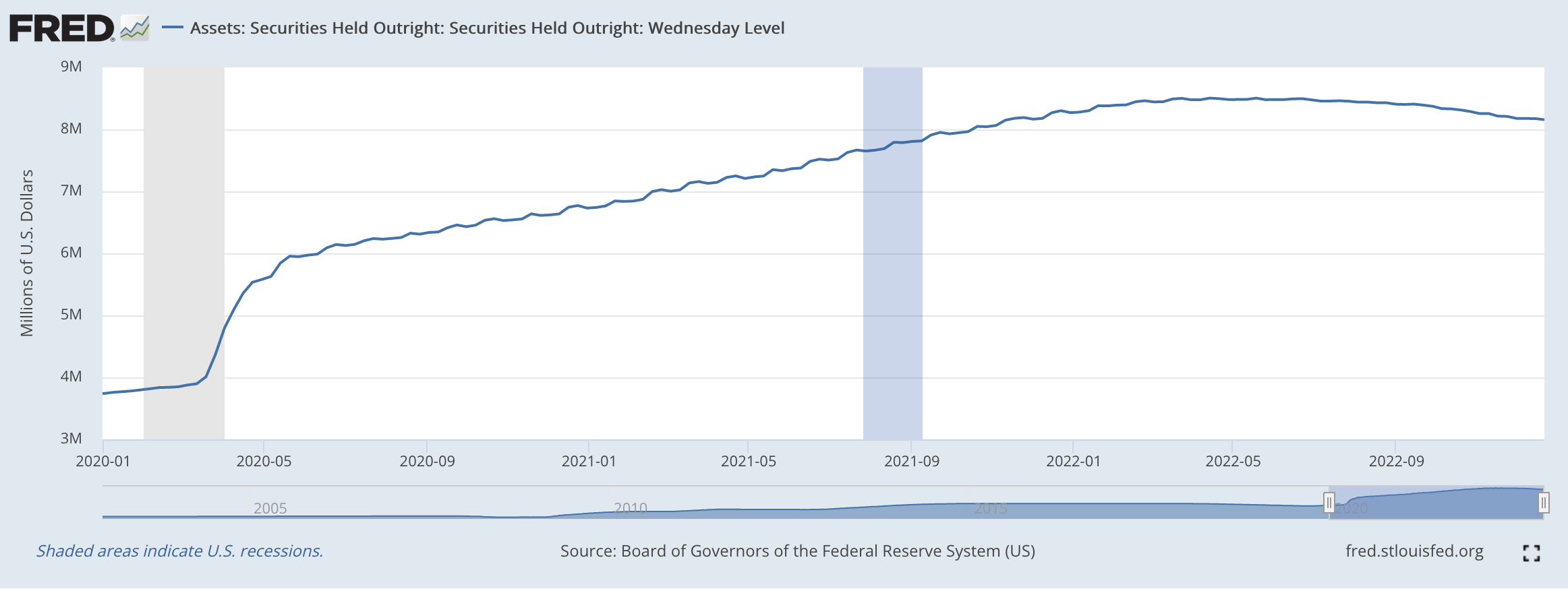

Perhaps the most important variable to watch during this current policy effort is the amount of securities the Federal Reserve holds outright on its balance sheet.

The Federal Reserve is working to achieve its goal by reducing the amount of securities that it carries on its balance sheet. The policy it is applying to achieve this is called “quantitative tightening.” The idea is for the Fed to reduce the amount of securities in its portfolio on a regular basis for an extended period of time.

When the Fed was working to stimulate the economy and prevent severe damage to occur because of the spread of the Covid-19 pandemic, the Fed engaged in “quantitative easing” where it purchased a regular amount of securities on a monthly basis to increase its securities portfolio.

In the period 2020-2021, the Fed added about $4.5 trillion in securities to its securities portfolio.

It is this volume that the Fed is trying to “eat” into in the effort to tighten up the financial system and combat the inflation that is driving across the country.

From March 16, 2022, through December 21, 2022, the Federal Reserve has overseen a reduction of its securities portfolio of $333.9 billion.

In the following chart, you can see how the reduction of the portfolio has followed a steady decline as is consistent with the program of “quantitative tightening” that the Fed is conducting.

One can also see the rising level of the securities portfolio after early 2020. Note how steady the rise is as the Fed was adding $120.0 billion to its securities portfolio almost every month in the 2020-20121 period.

Securities Held Outright (Federal Reserve)

Note that the Fed is not seeing the securities portfolio decline as quickly as it allowed the securities portfolio to increase during the buildup of the portfolio.

The point is, however, that the Fed is trying to maintain its approach to conducting monetary policy, applying “quantitative tightening” when fighting inflation and “quantitative easing” when it is attempting to stimulate the economy.

The Big Question

The big question relates to the quantity of securities that the Fed will ultimately remove from the securities portfolio.

The quantitative easing began in early 2020 and lasted until the spring of 2022.

Quantitative tightening began in the spring of 2022.

Will the Federal Reserve conduct quantitative tightening over the same amount of time that quantitative easing was applied?

Best guess?

The Fed will not keep applying quantitative tightening anywhere near as long as it applied quantitative easing in 2020-2021.

But, then, how long will the Fed apply quantitative tightening?

This is the big question.

The Federal Reserve extending quantitative easing way longer than anyone really expected it to. And, the Federal Reserve has been highly criticized for doing so.

The fact that it continued so long is given as a reason why there is way too much liquidity in the money system right now.

Many people have been surprised that the Federal Reserve has extended quantitative tightening so long. Many believed that the Fed would “pivot” from its monetary stance way before now.

So, how long till the Fed keeps up its quantitative tightening?

The feeling is that the Fed will “back off” from its tightening as soon as it feels financial markets are on the verge of a significant drop. It is generally thought that the Fed will not risk too much of a market decline, and so will change its policy stance as soon as any real danger is felt.

But does that take us into the Spring of 2023 or the fall of 2023?

Might it get us into 2024?

What the Fed will eventually do is what investors are now placing bets on.

How high-interest rates go is dependent upon how long the Fed feels it needs to stick with its quantitative tightening.

Uncertainty.

The Economy

The Federal Reserve does not seem to be that threatened by slow economic growth.

As I discussed in a recent post, the Fed’s forecast for economic growth over the next two years is a 0.5 percent rate of real growth in 2022 and another 0.5 percent rate of real growth in 2023.

The Fed does not appear to be overly concerned with a major slowing down in the growth rate of the economy.

In fact, the Fed perceives that economic growth will be less than 2.0 percent for most of the next 3-5 years.

This kind of a future, the Fed believes, will get inflation back down to the Fed’s target 2.0 percent rate of increase. This would be nice.

So, the real focus for the next year or so should be just how far the Fed is willing to go to reduce the size of its portfolio of securities.

Interest rates will do what they will during this time period.

The real battle is going to be to see just how far the Fed can reduce the size of its securities portfolio.

Let me just close by saying that the Federal government is not helping the Federal Reserve by continuing to create so much more Federal Debt that must be financed.

Be the first to comment