BeeBright

I believe every portfolio should have some space reserved for “crown jewels” that have competitive advantages and irreplaceable assets. That’s because economic uncertainty and volatility will inevitably come again, and these assets were built to withstand adversity. What’s even better is if these stocks can be acquired at reasonable valuations.

This brings me to Federal Realty Trust (NYSE:FRT) which checks off a lot of the aforementioned boxes. In this article, I highlight why FRT is a high-quality buy for sleep well at night returns at the current price, so let’s get started.

Why FRT?

Federal Realty Trust is a shopping center REIT that was founded back in 1962. It has a portfolio of high-quality shopping centers that are mostly located in densely populated areas with high average household incomes. These properties include Santana Row in San Jose, California, Pike & Rose in North Bethesda, Maryland, and Assembly Row in Somerville, Massachusetts.

At present, FRT’s portfolio consists of 105 properties in eight of America’s largest metropolitan areas, with 3,100 tenants across 25 million square feet and approximately 3,400 residential units. Notably, FRT is also a Dividend King that’s weathered through countless economic cycles and raised its dividend for 55 consecutive years. FRT’s strengths were highlighted by Morningstar in its recent analyst report:

Federal Realty Trust has strategically acquired and developed assets in submarkets with strong demand drivers, creating a portfolio with average location population density and median household income higher than any other retail REIT. As a result, Federal Realty has been able to drive strong same-store net operating income growth and average double-digit re-leasing spreads over the past two decades. Its portfolio should continue to attract shoppers and tenants and produce solid internal growth even in a challenging retail environment.

FRT continues to shine, as it produced FFO per share of $1.65 during the second quarter, beating analyst estimates by $0.16 and rising by 17% YoY from $1.41 in the prior year period. This was driven by strong rental increases, as same property operating income grew by 8.2% YoY. Also encouraging, occupancy remained strong, with 92% total occupancy and 94.1% leased, representing increases of 240 basis points and 140 bps, respectively.

These strong results led management to significantly raises its full year 2022 guidance, with guided same store NOI growth rising by 200 basis points to 5.5% to 7.0%. Also encouraging, management also raised its FFO per share guidance by 22.5 cents to $6.10 to $6.25.

Looking forward, continued strong leasing trends and FRT’s development pipeline could drive meaningful growth. This was highlighted by the CEO, Don Wood, during the recent conference call:

So you have to stand out to outperform over cycles. You do that by picking the right markets and positioning and merchandising in those markets, but you also have to reinvest to continually find the edge. Reinvesting is more important now than ever before.

It’s why we have nearly two dozen active and meaningful development projects in planning or underway totaling over $100 million this year and next which will likely yield double-digit un-levered yields over the ensuing years through higher customer traffic and rents, in line with our historically observed results following property improvement projects. That reinvestment is one of the primary reasons we can continue to push rents.

Leasing has been exceptionally strong at our newly development assets also, from the completion of CocoWalk, to the office projects at Pike & Rose, to the residential over retail at Darien and to the residential and office Phase 3 at Assembly Row each of these additions have exceeded our post-COVID expectations in terms of lease-up pace. In the case of the residential product at Assembly that’s exceeded in both pace and rental rate.

Meanwhile, FRT is just one of a handful of REITs with an A- credit rating, and its balance sheet remains solid, with a net debt to EBITDA ratio of 5.8x and fixed charge coverage ratio of 4.3x. Moreover, 93% of FRT’s debt is fixed rate and management continues to target a leverage ratio in the low to mid 5x range. FRT also pays a well-covered 3.9% dividend yield with a 65% payout ratio, based on the aforementioned Q2 FFO per share of $1.65.

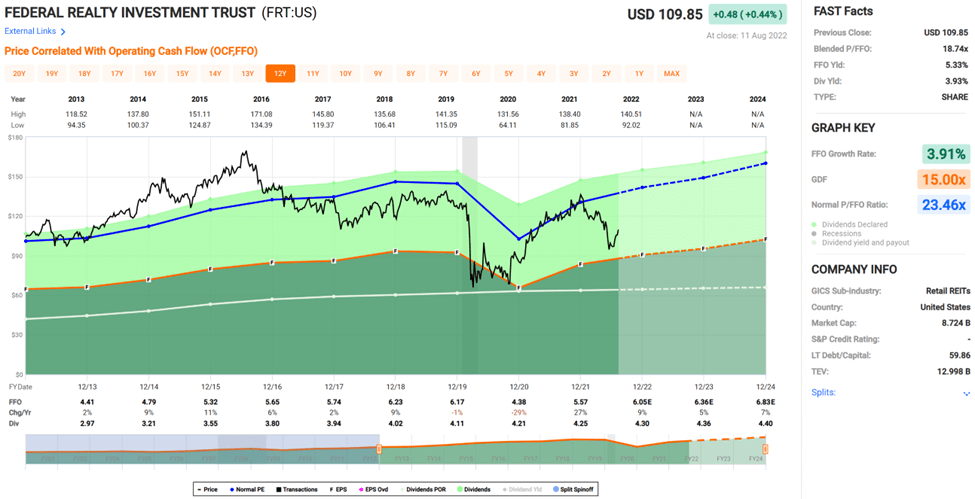

While FRT isn’t cheap, I still see value in it at the current price of $111.68 with a forward P/FFO of 18.4, sitting below its normal P/FFO of 23.5 over the past decade. Morningstar has a fair value estimate of $138 and sell side analysts have a consensus Buy rating with an average price target of $121, translating to potential double-digit total returns over the next year.

FRT Valuation (FAST Graphs)

Investor Takeaway

Overall, I believe Federal Realty is a high-quality retail REIT that is well-positioned to continue outperforming in the current environment. With its strong results, increased guidance, and solid balance sheet, I believe the outlook for FRT is bright.

While it isn’t cheap, I still see value at the current price due to the quality of the enterprise and its strong track record. With a well-covered dividend yield near 4%, FRT is a solid choice for income investors.

Be the first to comment