Central Bank Watch Overview:

All Quiet at the Eccles Building

In this edition of Central Bank Watch, we’ll review the speeches made in March by various Federal Reserve policymakers. The information drip has run dry in recent days, however, as the Fed is now in its pre-meeting communications blackout period. The FOMC next meets on Wednesday, March 17.

For more information on central banks, please visit the DailyFX Central Bank Release Calendar.

Federal Reserve Looks Past Rising Yields, Inflation Expectations

Rising US Treasury yields have dragged higher global bond yields, spooking equity markets at home and abroad. But there has been a consistent theme among Fed speakers: rising yields are a positive sign of improving economic growth prospects. Those suggesting that the Fed is ready to throw in the towel, may want to reconsider.

March 1 – Barkin (Richmond Fed president) says that shifts in Treasury yields are not trickling down to the real economy yet, noting that “at these levels of interest rates, when I talk to businesses in my district, I do not hear any sense that people are dialing back their investment.” Brainard (Fed governor) sees “prudence” in keeping restrictions on banks’ capital distributions.

March 2 – Daly (San Francisco Fed president) says that the steepening US yield curve is a “sign” of market optimism regarding the shape of the economy. Brainard (Fed governor) says that bond market moves “caught my eye,” and it will take “some time” for the Fed to achieve the necessary conditions to taper its asset purchases.

March 3 – Fed Beige Book released, showing optimism over state of economy thanks to increased vaccination efforts. Harker (Philadelphia Fed president) says that “even with some hopeful signs as virus cases fall and the economy continues to reopen, I’m concerned that, as the broader economy climbs upward, far too many workers are being left behind.”

March 4 – Powell (Fed Chair) confirms that the FOMC still sees no reason to change course, simply because of volatility in US Treasury markets, saying “We monitor a broad range of financial conditions and we think that we are a long way from our goals…I would be concerned by disorderly conditions in markets or persistent tightening in financial conditions that threatens the achievement of our goals.”

March 5 – Mester (Cleveland Fed president), commenting on US Treasury market volatility, says “the bond market is reflecting, I think, the strength that we’ve seen in some of the recent data. They’re looking ahead and they’re positive.” Bostic (Atlanta Fed president) says that he’ll “be comfortable letting the economy run hot,” in part because “it’s difficult to tease out a real signal of underlying inflation.” Kaskhari (Minneapolis Fed president) says “we’re not seeing much movement in real yields. Most of the movement is in that inflation expectations, or inflation compensation…The recent movements that we’ve seen in the Treasury market — both the TIPS market and the nominal market — suggest that our framework is delivering what we wanted it to deliver.”

Federal Reserve Interest Rate Expectations (March 9, 2021) (Table 1)

Accordingly, after a week of Fed officials downplaying inflation fears and suggesting that rising US Treasury yields reflect economic optimism, interest rate expectations remain firmly anchored: Fed funds futures are pricing in a 93% chance of no change in Fed rates through January 2022. The bottom line: don’t expect the Fed to do anything along the interest rate channel anytime soon.

Instead, the FOMC may opt for a simpler solution to prevent a further backing up of yields: extending the supplementary leverage ratio (SLR) requirement for banks, which have been exempted from counting Treasuries and reserves against their capital as a percentage of total assets for the past year during the pandemic. If the SLR requirement rolls off, US banks would be forced to increase their capital holdings and/or reduce their Treasury holdings, and a wave of Treasury selling could push yields higher again.

Simply announcing an extension to the SLR requirement at the March 17 FOMC meeting may remove a potential factor for more volatility in US yields in the near-term.

Recommended by Christopher Vecchio, CFA

Get Your Free USD Forecast

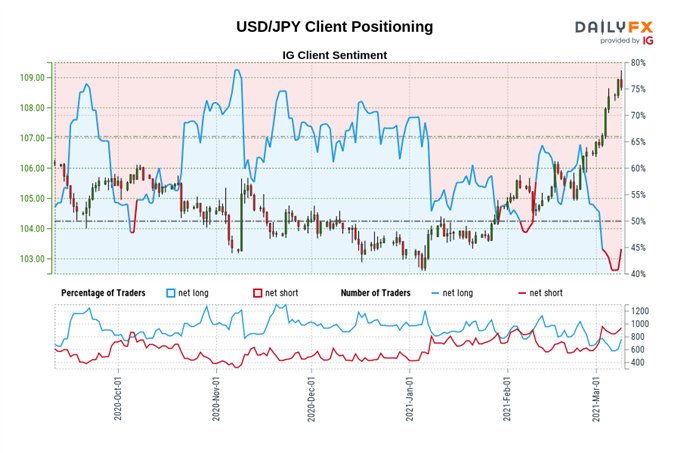

IG Client Sentiment Index: USD/JPY Rate Forecast (March 9, 2021) (Chart 1)

USD/JPY: Retail trader data shows 39.24% of traders are net-long with the ratio of traders short to long at 1.55 to 1. The number of traders net-long is 11.58% lower than yesterday and 7.91% lower from last week, while the number of traders net-short is 16.03% higher than yesterday and 20.37% higher from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-short suggests USD/JPY prices may continue to rise.

Traders are further net-short than yesterday and last week, and the combination of current sentiment and recent changes gives us a stronger USD/JPY-bullish contrarian trading bias.

Read more: FX Week Ahead – Top 5 Events: US Inflation; BOC & ECB Rate Decisions; UK GDP; Canada Jobs

— Written by Christopher Vecchio, CFA, Senior Currency Strategist

Be the first to comment