helloabc

Farfetch (NYSE:FTCH) is one of those stocks where I really can’t quite make up my mind. A former e-commerce high-flyer, the stock has fallen 90% over the past two years as the bubble in tech/e-commerce stocks has burst and the current macro/geopolitical environment has proven unfavorable. Moreover, financial targets revealed at the company’s December Investor Day were uninspiring – calling into question the ultimate potential of Farfetch’s leading luxury e-commerce business.

Having said all of that, there are many things to like about the company – it has cultivated strong relationships with many of the world’s leading luxury brands. While Farfetch remains unprofitable, it should have the financial resources necessary to survive the current rough patch. Moreover, with a market cap of just $2 billion, Farfetch trades at an EV/sales ratio well below 1x which is low for a leading marketplace business (there are plenty of caveats here as I will discuss below).

Weighing the pros and cons, I’ve taken a very, very small position in the stock. While I lack any conviction that value will be realized for shareholders, I acknowledge that the company’s potential value is well in excess of the current market price.

What’s To Like?

There are several aspects of the Farfetch investment case I find compelling, including:

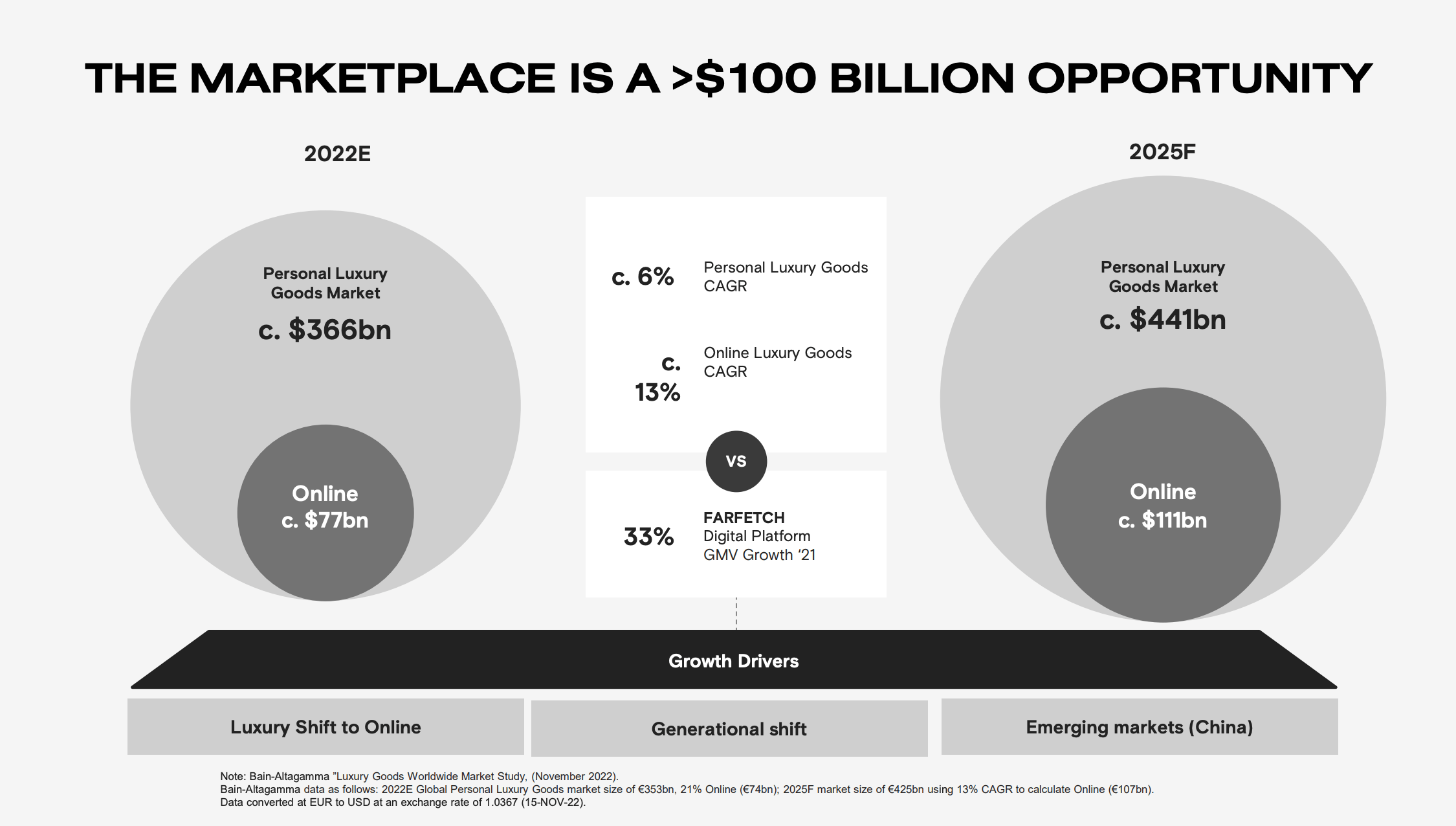

- Farfetch has a very strong position in a large (luxury goods represent $350 billion on GMV), growing industry. Farfetch.com is the largest multi-brand e-commerce marketplace. Further, Fartfech Platform Solutions is a leading provider of technology solutions to leading luxury brands. There are clear synergies between these two businesses (cross-selling of capabilities to luxury brand supplier/partners) which represents a unique competitive advantage for Farfetch. As luxury goods are increasingly sold online, Farfetch appears well positioned to benefit.

Luxury Goods Market Size & Growth Expectations (Farfetch Investor Presentation)

- Farfetch has assembled supplier partnerships with many leading luxury brands. Leading luxury conglomerates like Chanel, Richemont, Kering, all have equity stakes in Farfetch which is indicative of the long-term partnership. Luxury brands are notoriously selective in choosing third party retail partners (both e-commerce & bricks and mortar) as maintenance and enhancement of brand image is paramount in the luxury goods business. Hesitancy to broadly distribute (maintain perceived ‘scarcity value’) benefits Farfetch in the form of reduced competition. Brands available on the Farfetch marketplace include Gucci, Ferragamo, Chanel, Prada, Saint Laurent, Dolce & Gabana and more.

- While Farfetch’s watch/jewelry offering is relatively limited at present, Farfetch’s blossoming partnership with Richemont should eventually bring leading jewelry/watch brands (Van Cleef &Arples, Cartier, IWC, Baume & Mercier, etc) to its marketplace platform. A credible jewel.

- While Farfetch’s Marketplace & Platform Solutions businesses have yet to turn a profit, these are structurally attractive businesses with strong competitive positions that should ultimately produce high margins and returns on capital.

- Farfetch has gross cash/equivalents of $700 million (slight net cash position) which should help the company bridge the gap to profitability.

- Valuation -well maybe. While Farfetch is not yet profitable, it trades at ~1x 2025 estimated marketplace/platform revenue (excludes owned brands). Given the company’s leading market position, above average anticipated growth, and economically favorable characteristics of an online marketplace business I believe a private buyer of the whole business would be willing to pay double the current share price.

What are the Risks?

Most of my concerns center around management’s decision-making ability. While management has done a great job of creating brand partnerships (without which there would be no business), I fear there is a lack of focus and financial responsibility – consider:

- Farfetch’s foray into owned luxury brands via the acquisition of New Guard in 2019 seems like an unnecessary distraction.

- Similarly, the acquisition of a stake in Niemen Marcus for $200 million in 2022 further (benefits here are unclear) confuses the picture and calls into question capital allocation. Not to mention that this depletes cash resources at a time when Farfetch (which is not yet profitable) faces an economic downturn.

- While it is easy to chalk this up to hindsight bias, Farfetch traded at a stratospheric valuation in 2021 (trading north of $65 Farfetch had a $25 billion market cap at one point – trading in excess of 15x digital revenue) and clearly should have used the share price strength to further fortify its balance sheet by issuing shares. Management’s failure to issue equity during the bubble makes me question their grip on reality.

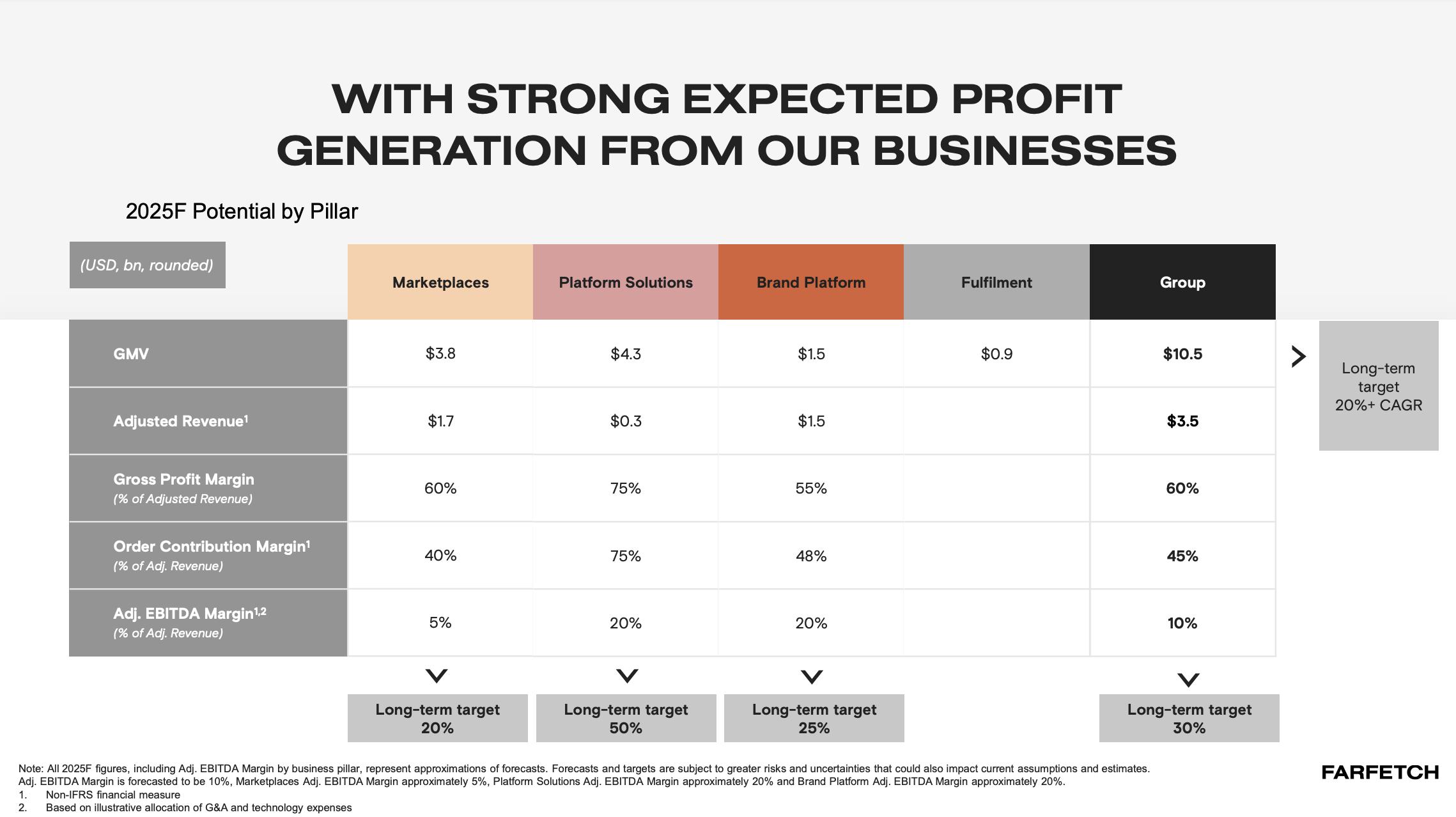

- Disappointing guidance at December Investor Day. As shown below, Farfetch guided to 2025 adjusted EBITDA margins of just 5% for its Marketplace business. While Farfetch shows a long-term target of 20% for Marketplace at this point investors are largely ignoring this guidance (for good reason in my opinion). Though I believe that 20% margins are attainable, I doubt that will occur with the present management team.

2025 Profitability Targets (Farfetch Investor Day Presentation)

Conclusion

I am enthused by Farfetch’s leading market position, brand partnerships, and growth potential. Further, I believe its marketplace and platform businesses have the potential to generate strong margins and returns on capital. However, I am concerned that this value may never be realized under the current management team. I’ve taken a very, very small position (call it a tracker position) here at $5/share based on my belief that Farfetch would command a much higher price in a sale to a new owner who could significantly improve profitability (though there is no indication the business will be sold).

Be the first to comment