felixmizioznikov/iStock Editorial via Getty Images

Exxon Mobil (XOM) is going to submit its earnings card for the fourth-quarter shortly and the petroleum company is most likely going to sail past estimates due to pricing strength in end-markets and improving free cash flow. While growth stocks are currently selling off, deep value and dividend stocks like Exxon Mobil have potential to build upon recent gains!

FY 2022 should see a continual market recovery and a restart of tourism industries

The COVID-19 pandemic shattered Exxon Mobil’s production business, but the energy firm is making a strong comeback due to a pandemic that is waning and higher market prices for petroleum that are all but set to improve earnings and free cash flow in the foreseeable future.

2021 was a recovery year for Exxon Mobil in which the firm restructured its business and repaid debt. This year, 2022, could see Exxon Mobil return to an expansionist business strategy which could be supported by continual pricing strength in end-markets and growing petroleum demand, especially from sectors that are involved in the tourism industry. I believe this because the most recent Omicron variant is not as deadly as initially feared and multiple countries could be on the brink of relaxing Coronavirus restrictions. The U.K. has said that it is going to lift all Coronavirus restrictions shortly, and there is evidence that the Omicron wave is past its peak in the U.S., too.

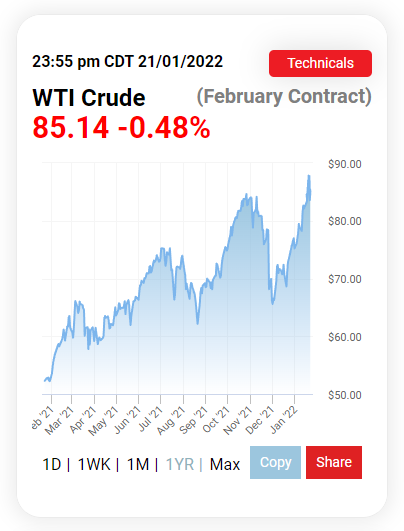

What this means is that petroleum demand could soar in 2022 as the world moves past COVID-19, and travel and hospitality industries continue on their recovery path. Prices for petroleum have recovered all throughout 2021 and are now near 1-year highs of around $85. The recovery in product pricing materially supports Exxon Mobil’s free cash flow growth.

Oilprice.com

Free cash flow recovery and refreshed estimates for Q4

Because of the strong pricing in petroleum markets in the fourth-quarter, I am refreshing my estimates for Exxon Mobil’s free cash flow. Until recently, I expected the petroleum firm to generate $8.2B in Q4’21 free cash flow which would bring total FY 2021 free cash flow to approximately $31.0B. In the third-quarter, Exxon Mobil saw a 25% increase in operating cash flow and a 30% increase in free cash flow, quarter over quarter. In the fourth-quarter, petroleum prices continued to soar, suggesting that both operating and free cash flow will be higher yet again when Exxon Mobil submits its earnings card next month. Because of the continual recovery in product prices in Q4’21, I expect Exxon Mobil to generate $13.0B in operating cash flow and $9.8B in free cash flow. Calculating with these estimates, Exxon Mobil’s FY 2021 free cash flow could be up to $32.6B. I am assuming a stable operating-cash-flow-to-free-cash-flow conversion of approximately 75%.

|

2021 |

2020 |

||||

|

$B |

Quarter 4 (Est) |

Quarter 3 |

Quarter 2 |

Quarter 1 |

Quarter 4 |

|

Cash Flow from Operating Activities |

$13.0 |

$12.1 |

$9.7 |

$9.3 |

$4.0 |

|

Proceeds from Asset Sales |

$0.0 |

$0.0 |

$0.3 |

$0.3 |

$0.8 |

|

Cash Flow from Operations and Asset Sales |

$13.0 |

$12.1 |

$9.9 |

$9.6 |

$4.8 |

|

PP&E Adds / Investments & Advances |

($3.2) |

($3.1) |

($3.0) |

($2.7) |

($4.1) |

|

Free Cash Flow |

$9.8 |

$9.0 |

$6.9 |

$6.9 |

$0.7 |

(Source: Author)

For FY 2022, I estimate that Exxon Mobil could generate between $35B and $40B in free cash flow, assuming that end-market prices remain above $80 per barrel. Based off of FY 2022 free cash flow estimates, shares of Exxon Mobil have an 8 X-9 X P-FCF ratio.

Fourth-quarter expectations

Expectations are for Exxon Mobil to deliver EPS of $1.94 and revenues of $85B for the fourth-quarter. I believe Exxon Mobil will submit EPS that will be materially better than the one expected. Exxon Mobil’s Q4’21 EPS was revised upwards 15 times in the last 90 days.

Seeking Alpha Estimates

Risks with Exxon Mobil

Exxon Mobil’s potential to grow earnings and free cash flow depends on market demand for petroleum products and pricing. The more demand for petroleum products exists, the more money Exxon Mobil is going to make on the back-end. Market factors have driven petroleum prices to negative $37 per-barrel in 2020, at the onset of the Coronavirus pandemic, but the market is in a much better constitution today than two years ago. Softening pricing in end-markets and falling demand for petroleum products indicate potential for a significant correction in Exxon Mobil’s earnings and free cash flow.

Final thoughts

Exxon Mobil is set to fly past estimates for the fourth-quarter in February, chiefly because of strengthening market pricing for petroleum products in the October to December period. For that reason, I believe Exxon Mobil is going to submit an earnings card that will be much better than expected.

I also took a second look at my free cash flow estimates. I now estimate Exxon Mobil could achieve almost $10B in free cash flow just in the fourth-quarter, with total FY 2021 free cash flow likely to exceed $32B. Based off of a P-FCF ratio of 8 X-9X , shares of Exxon Mobil are still worth buying!

Be the first to comment