Author’s note: This article was released to CEF/ETF Income Laboratory members as part of the CEF Weekly Roundup on November 15, 2022. Please check latest data before investing.

The first news to discuss is the proposed merger between Eaton Vance Tax-Managed Buy-Write Strategy Fund (NYSE:EXD) and Eaton Vance Tax-Managed Buy-Write Opportunities Fund (ETV).

From the press release:

November 09, 2022 04:05 PM Eastern Standard Time. BOSTON–(BUSINESS WIRE)–The Boards of Trustees of Eaton Vance Tax-Managed Buy-Write Strategy Fund (EXD) (the Acquired Fund) and Eaton Vance Tax-Managed Buy-Write Opportunities Fund (ETV) (the Acquiring Fund) have approved a proposal for the Acquired Fund to merge with and into the Acquiring Fund.

The proposed merger is subject to approval by Acquired Fund shareholders at a Special Meeting of Shareholders scheduled for Thursday, February 2, 2023. A proxy statement/prospectus containing information about the meeting and the proposed merger will be mailed to the Acquired Fund’s shareholders of record as of November 21, 2022. No action is needed by shareholders of the Acquiring Fund. Each Fund is a diversified closed-end management investment company sponsored and managed by Eaton Vance Management. Each Fund is listed on the New York Stock Exchange.

The Acquired Fund has the same investment objectives and substantially the same investment policies and restrictions as the Acquiring Fund. Additional information regarding the proposed merger will be contained in the proxy statement/prospectus.

The merger is currently expected to be completed in the first or second quarter of 2023, subject to required shareholder approvals and the satisfaction of applicable regulatory requirements and customary closing conditions.

If the merger is approved, each Acquired Fund shareholder will be issued common shares of the Acquiring Fund at an exchange ratio based on the Funds’ respective net asset values per share. Following the merger, the Acquiring Fund will continue to be managed in accordance with its existing investment objectives and strategies.

In this proposal, ETV, the larger of the two funds at $1.36 billion in assets, will be acquiring EXD, which is much smaller at only $91.3 million in assets. The merger was approved by the boards of both EXD and ETV, and require the approval of EXD’s shareholders (but not ETV’s shareholders). The special meeting of EXD shareholders will be held on February 2, 2023, based on holders of record on November 21, 2022.

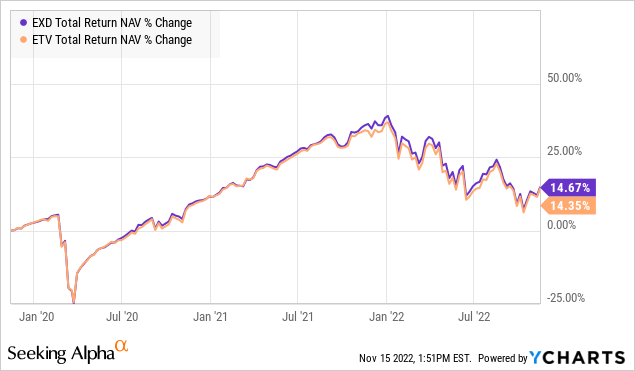

The proxy materials aren’t out yet, so we can only speculate as to the motives of the managers for the merger. One reason for the merger is to consolidate their CEF lineup, given that EXD and ETV run substantially similar strategies. The two funds are both domestic equity option income CEFs that use about a 50:50 split of the S&P 500 and NASDAQ as their benchmarks, and with nearly full option coverage of their portfolios. As a result, the two funds’ NAV profiles track each other very closely.

YCharts

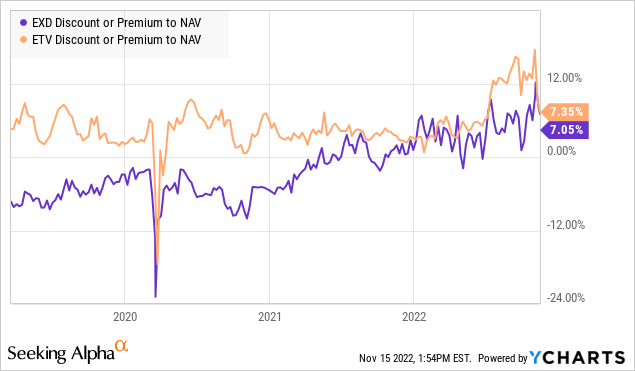

EXD hasn’t always been a clone of ETV however. Prior to February 8, 2019, EXD was known as the Eaton Vance Tax-Advantaged Bond and Option Strategies Fund and executed a very different investment strategy (that had horrible performance). As we shared at the time (public link), the strategy change for EXD provided a catalyst for EXD’s discount to narrow vs. ETV, and indeed this is what happened over the next several years.

YCharts

Hence, investors who chose EXD on our recommendation would have achieved around +20% better total return compared to ETV (+45.99% vs. +25.85%), despite the fact that their NAV returns were nearly the same (also see EXD And ETV: How To Generate Alpha Using CEFs).

YCharts

Other benefits of the merger are a potentially decreased expense ratio, because fixed expenses can become spread over a larger asset base. This is particularly relevant for EXD shareholders because of the fund’s smaller size. Although both ETV and EXD charge 1.01% in management fees, EXD’s “other expenses” come out to 0.20% compared to 0.07% for ETY, resulting in a slightly higher overall expense ratio for EXD. Simply put, it is less economical to run a smaller fund than a larger one. Finally, EXD shareholders will likely enjoy better liquidity after being incorporated into the larger ETY in the merger, resulting in narrower bid/ask spreads.

Despite the above benefits, as an EXD shareholder I will be voting NO to the merger. Why is this? The simple answer is that having ETV and EXD, being clones of each other, make an ideal swap pair for our CEF rotation strategy. Obviously, if the two funds merge into a single CEF, there will no longer be an opportunity to swap between the two funds.

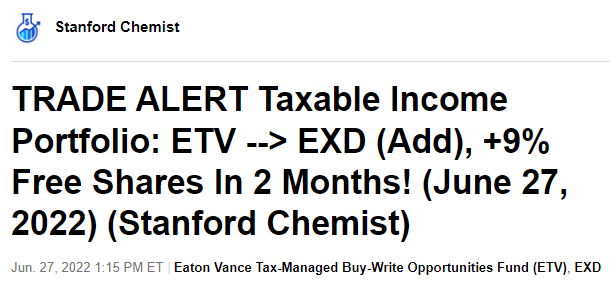

Our unique CEF rotation strategy is such a powerful method to gain alpha that it completely dwarfs the magnitude of the potential reduction of expense ratio in the merged fund. For example, we recently swapped from ETV back to EXD in our Taxable Income portfolio to gain +9% “free shares” of EXD in only 2 months. This +9% of excess alpha would require 69 years (!) of holding the merged fund to breakeven, based on an estimated 0.13% p.a. reduction of the expense ratio.

Income Lab

How did we arrive at the +0% increase of EXD shares? 2 months ago, we sold 640 shares of EXD at $11.55 ($7,392) to buy 490 shares of ETV at $15.00 ($7,350). Today, we’re selling those same 490 shares of ETV at $13.81 ($6,767) to buy 700 shares of EXD at $9.71 ($6,797). Hence, we got 60 shares of EXD “for free”, or a percentage increase of +9.4% in only 2 months! This is equivalent of nearly DRIPing 1 years’ worth of distributions from EXD for free!

Another benefit of keeping EXD separate is that the distributions from EXD have more favorable tax treatment than ETV thanks to its greater balance of tax loss carryforwards. This allows EXD to pay out a higher proportion of distributions as return of capital, which are not taxed (but reduces one’s cost basis). For example, in 2021, 100% of EXD’s distributions were classed as ROC per CEFdata. Whereas for ETV, they paid out 50.9% ROC, 42.1% in long-term gains and 7.0% in qualified dividend income. If EXD were to be merged into ETV, then the accrued loss carryforwards will be merged also. Since ETV is a much larger fund than EXD, this tax benefit will be greatly diluted when the funds are merged.

The final potential benefit that could happen for EXD shareholders as a result of the merger would be if ETV were trading at a higher premium than EXD. In that case, the merger would be beneficial to EXD shareholders (but disadvantageous for ETV shareholders). That is, the merger may present an arbitrage opportunity. However, with EXD (+6.28% premium) trading at only a fractionally lower valuation than ETV (+7.17% premium), this benefit is currently small.

As a result, I recommend that all shareholders of EXD vote no to the merger.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment