JHVEPhoto/iStock Editorial via Getty Images

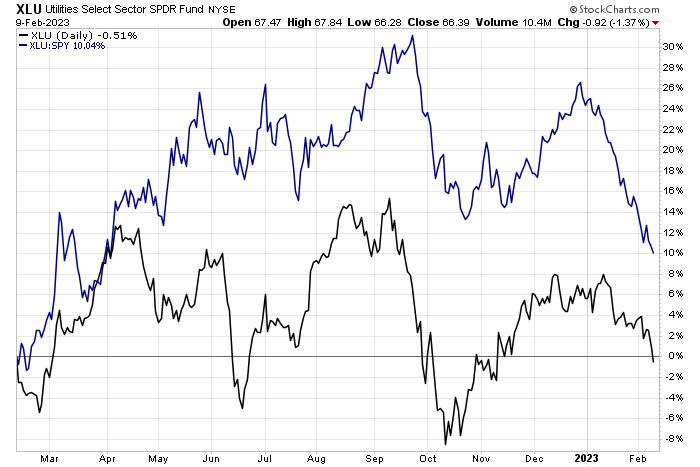

Utilities continue to slide against the broad market as rates tick back up and following an early-year bounce back in mega-cap growth shares. The Utilities Select Sector ETF (XLU) is now up just 10 percentage points on the S&P 500 (total return) over the last 52 weeks. Clearly momentum favors avoiding this risk-off sector for now.

One utility name features a valuation discount to the sector average, but are shares of Entergy poised to power ahead? Let’s dig into the valuation, options outlook, and technical situations ahead of earnings next week.

Utilities Underperform In 2023

Stockcharts.com

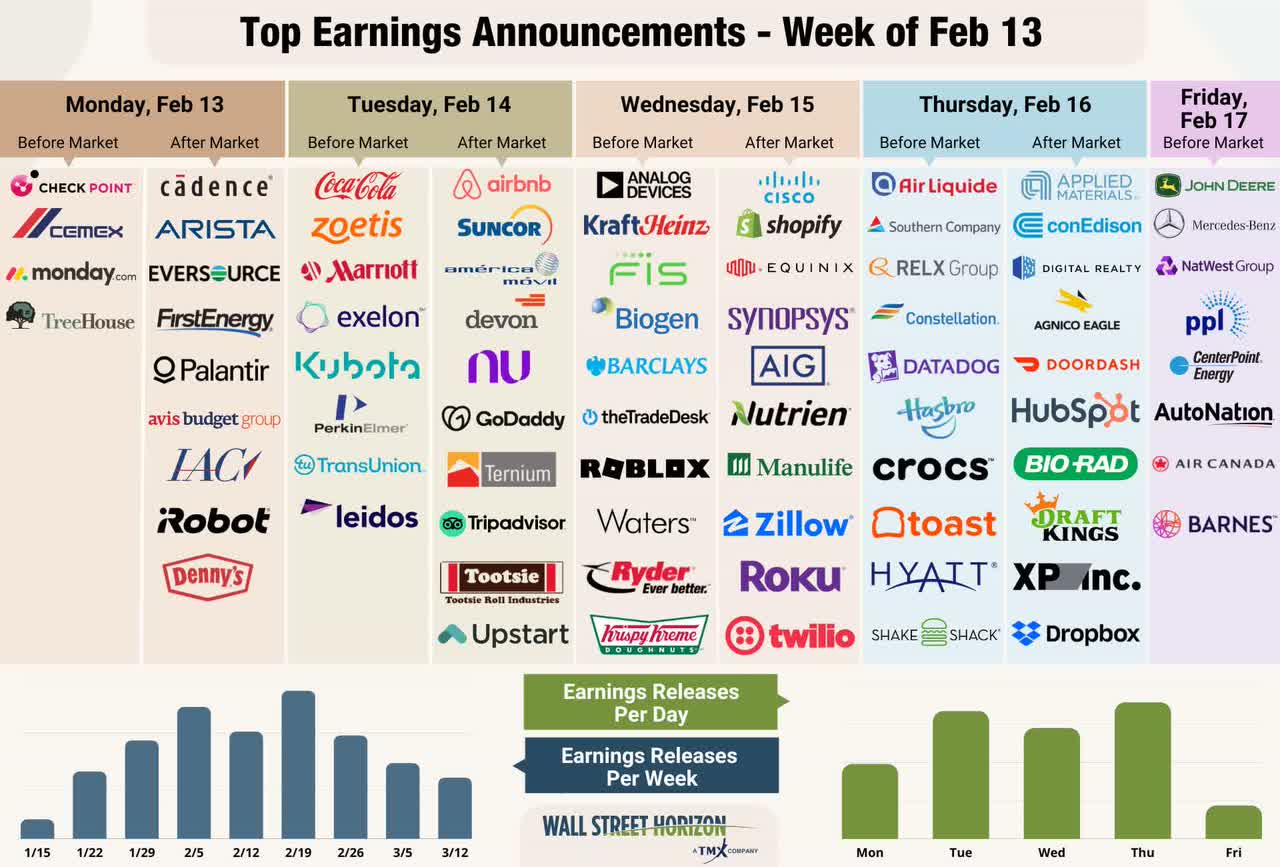

Earnings On Tap

Wall Street Horizon

According to Bank of America Global Research, Entergy Corporation (NYSE:ETR) is a holding company encompassing five regulated utilities in the Gulf States region, primarily Louisiana, Mississippi, Arkansas, Texas, and New Orleans. Entergy is one of the largest operators of regulated nuclear in the United States. There are other FERC jurisdictional assets, primarily System Energy Resources Inc (SERI).

The New Orleans-based $21.5 billion market cap Electric Utilities industry company within the Utilities sector trades at a near-market 16.8 trailing 12-month GAAP price-to-earnings ratio and pays a high 4.1% dividend yield, according to The Wall Street Journal.

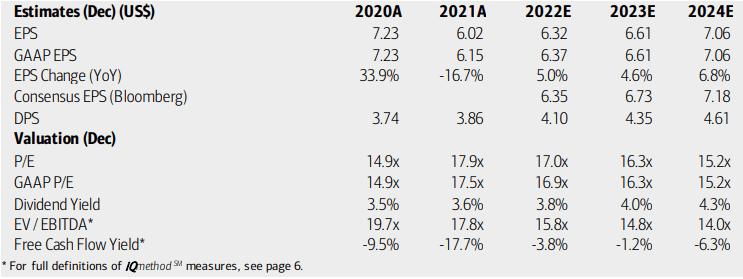

On valuation, analysts at BofA see earnings having risen slightly below the rate of inflation in 2022 but real per-share profits turn positive this year before an acceleration in 2024. The Bloomberg consensus forecast is slightly more sanguine compared to what BofA projects, too.

Dividends, meanwhile, are expected to rise steadily, leading to a higher yield if price action continues sideways. Both ETR’s operating and GAAP P/Es are at a discount to the sector median, which is good, but the EV/EBITDA ratio is high. With elevated hurricane risk and a balance sheet that has some weaknesses, there should be a valuation discount, so the earnings multiple seems fair to me.

Entergy: Earnings, Valuation, Dividend Yield Forecasts

BofA Global Research

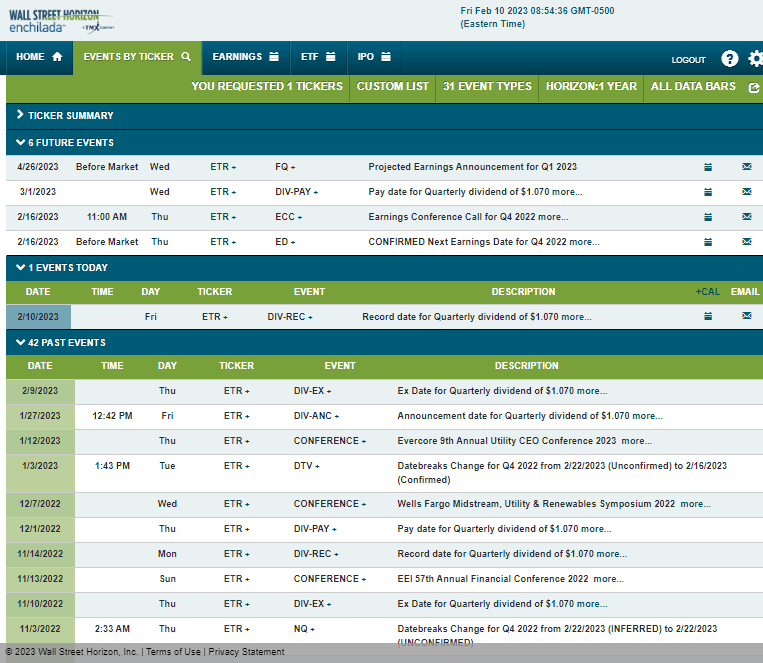

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q4 2022 earnings release before the open on Thursday, February 16 with a conference call later that morning. You can listen live here.

What’s particularly interesting about the reporting date is that Entergy confirmed it much earlier than usual. Wall Street Horizon rates it as an “A” in terms of positive potential news to be released within the report. You can learn more about the confirmation timing factor here.

The calendar is light on volatility catalysts in the near term, and we are out of hurricane season along with the coldest part of the calendar in terms of potential weather-related event risk.

Corporate Event Risk Calendar

Wall Street Horizon

The Options Angle

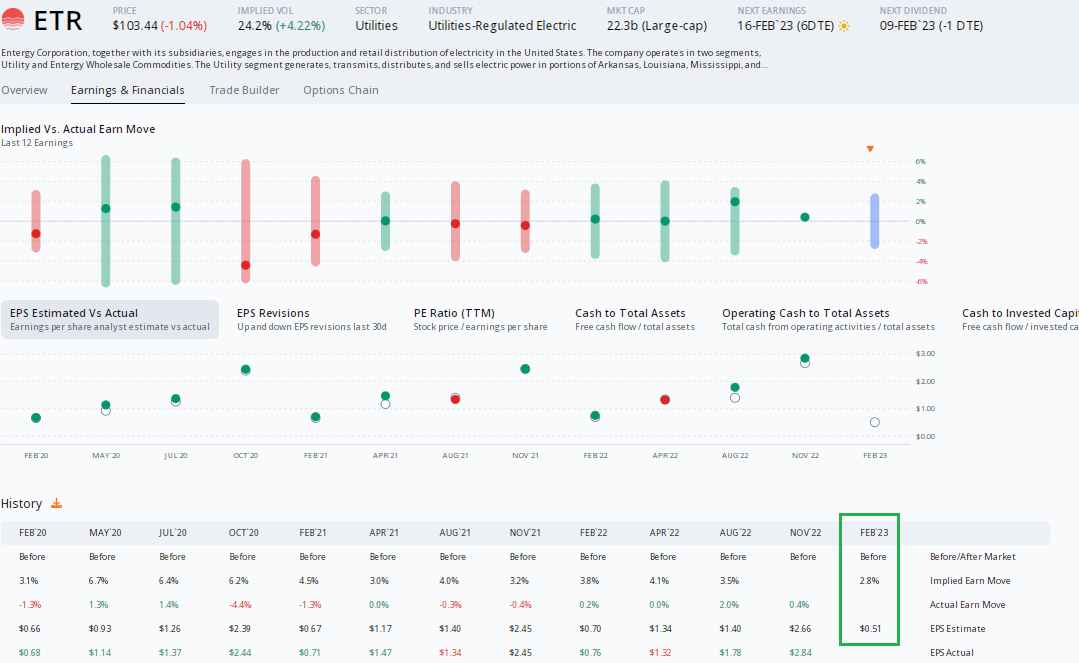

Digging into the upcoming earnings report, data from Option Research & Technology Services (ORATS) show a consensus EPS forecast of $0.51 which would be a steep 33% drop from $0.73 of per-share profits earned in the same period a year ago. Entergy has a mixed post-earnings stock price performance history with generally muted moves. The firm has topped analysts’ earnings expectations in 10 of the past 12 reports, so another earnings beat is likely.

In terms of the anticipated share price swing post-earnings this go around, the current at-the-money straddle expiring soonest after the Q4 report is priced at just 2.8% – that low figure is actually above historical moves dating back to October 2020. I’d rather play the shares here given low volatility expectations and historical moves.

ETR: Small Earnings-Related Move Priced In

ORATS

The Technical Take

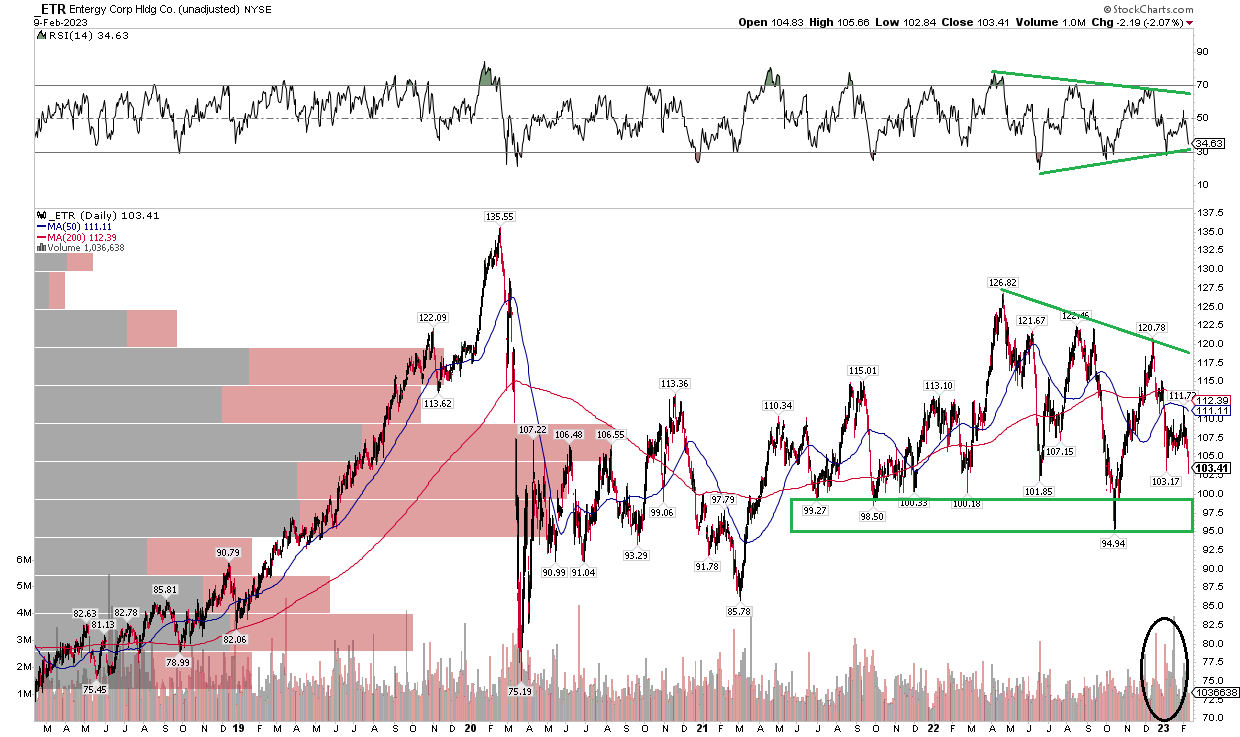

ETR is in consolidation mode. Notice in the chart below that shares should find some support in the upper $90s to low $100s as that has been an area where buyers have stepped up in the past two years. On a rally, there’s a downtrend resistance line off the 2022 multi-year high while both the 50 and 200-day moving averages are sideways.

RSI momentum is also narrowing – watch that indicator for a breakout or breakdown which could portend where the price goes. With a recent volume uptick and high volume by price going down to $95, we are currently in a battlezone that should generally be supportive.

ETR: Shares Consolidating & Approaching Key Support

Stockcharts.com

The Bottom Line

I’m a hold on ETR. The valuation appears priced right while the chart is simply sideways. Buying on a dip to the upper $90s could be a favorable risk/reward play.

Be the first to comment