undefined undefined/iStock via Getty Images

Introduction

I’ve mentioned in several articles on SA that I work as an M&A analyst covering Latin America, and I’ve written about several companies from the region, e.g. Betterware de Mexico (BWMX) here, Industrias Bachoco (IBA) here, and Cementos Pacasmayo (CPAC) here. Today, I want to talk about Chile-based soft drink maker Embotelladora Andina (NYSE:AKO.A) (NYSE:AKO.B). The company recently released its 2022 financial results and I think they were solid as net sales rose by 20.2% while the operating income increased by 24.4% in U.S. dollars. Embotelladora Andina stock is valued at just under 15x price to earnings while the dividend yield stands at well over 10% and I think it looks undervalued. Let’s review.

Overview of the business and financials

Embotelladora Andina, also known as Andina Bottling Co and Coca-Cola Andina, was founded in 1946 and focuses on the bottling and distribution of Coca-Cola (KO) products across Chile, Argentina, Brazil, and Paraguay. The company also produces bottled water, juices, iced tea, energy drinks, spirits, and wine among others.

Embotelladora Andina

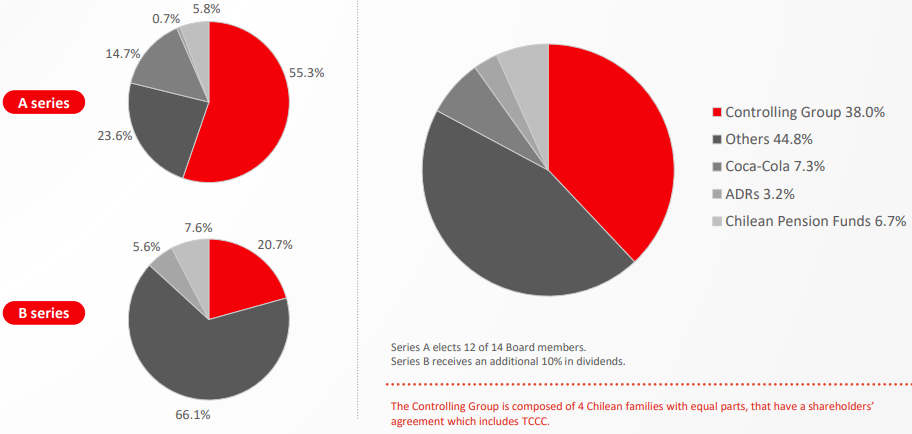

Embotelladora Andina has a total of 14 production facilities and over 90 distribution centers and employs more than 18,000 people. Looking at the shareholders list, a group of four families holds a 38% stake, Coca-Cola has 7.3%, and a total of 3.2% of the shares are listed in the USA as American Depositary Receipts (ADRs). Each ADR is equal to 6 common shares. Embotelladora Andina has two classes of stock – Series A which allows shareholders to elect 12 of the 14 board members, and Series B which give shareholders an additional 10% in dividends.

Embotelladora Andina

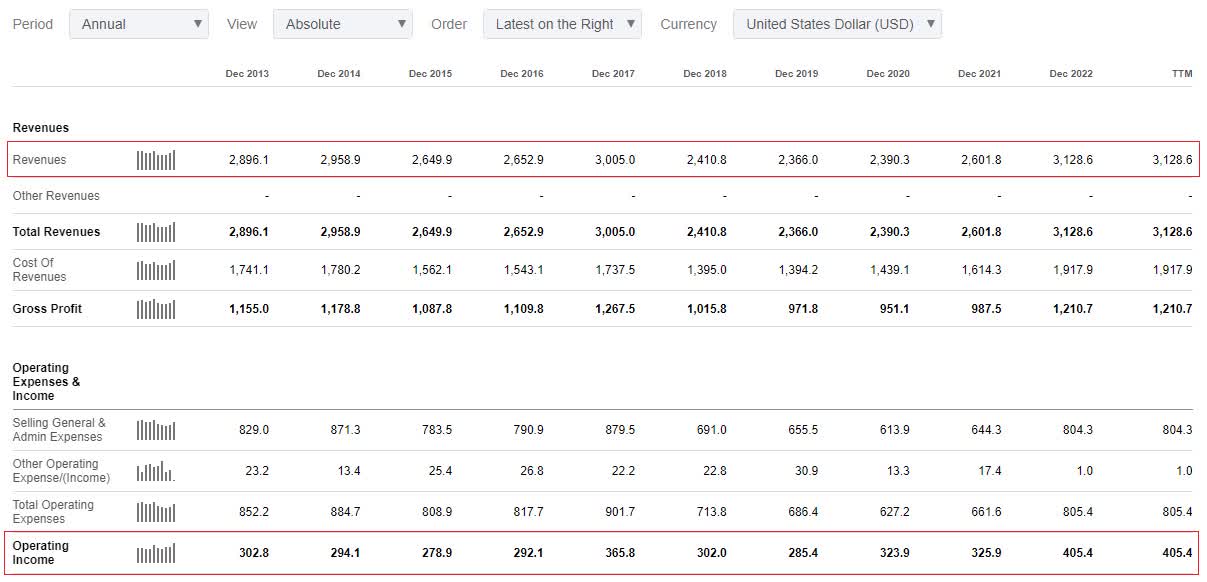

Turning our attention to the financial results of Embotelladora Andina, you can see that revenue and operating income for the past decade are all over the place and the main reason for that is the volatility of the currencies in the countries in which the company operates compared to the U.S. dollar (mainly Brazil and Argentina). The company was also affected by COVID-19 lockdowns and production is now at pre-pandemic levels. Overall, sales volumes have been increasing by around 5% year on year, mainly thanks to the addition of new products.

Seeking Alpha

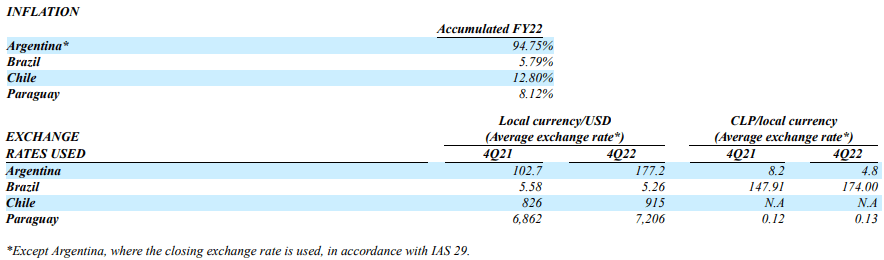

Looking at the 2022 inflation and exchange rate data, we can see that the macroeconomic environment in Argentina and to some extent Chile was challenging, but the Brazilian real was strong. This gave a boost to the revenues of Embotelladora Andina when measured in U.S. dollars and Chilean pesos.

Embotelladora Andina

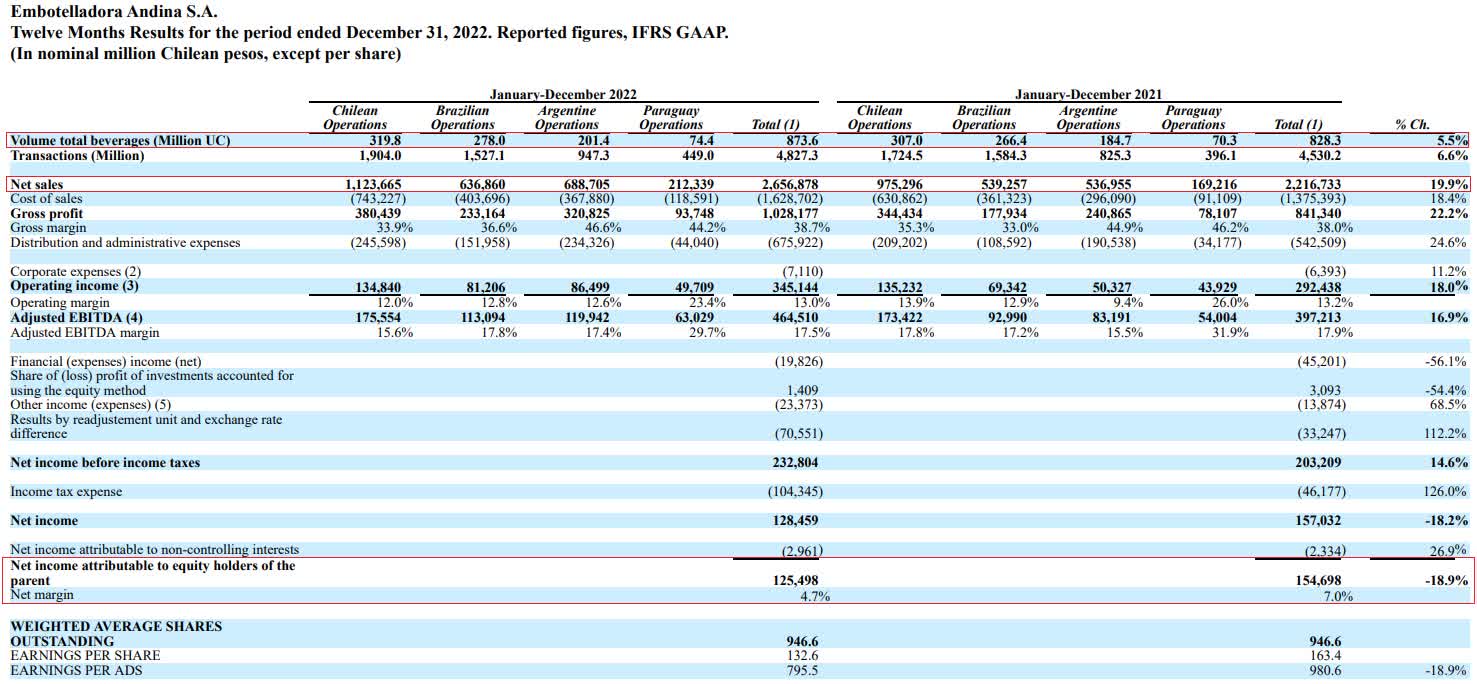

Looking at the production results, Embotelladora Andina delivered a total of 873.6 million unit cases or 4,960 million liters of beverages in 2022, which is 5.5% higher than a year earlier. All markets experienced solid growth as consumption rates across Latin America recovered following the end of COVID-19 lockdowns. Unfortunately, the net margin was put under pressure by foreign exchange losses and the net income went down by 18.9% in Chilean pesos and by 18.6% in U.S. dollars.

Embotelladora Andina

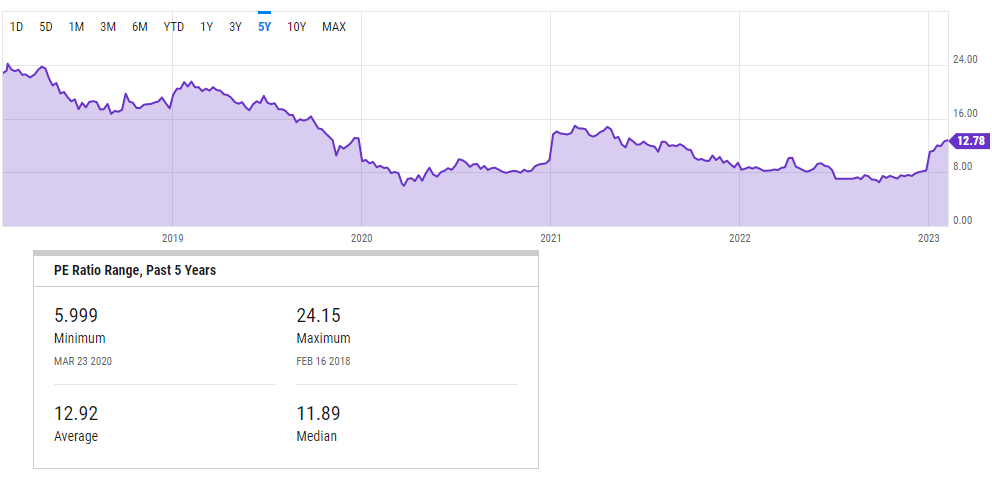

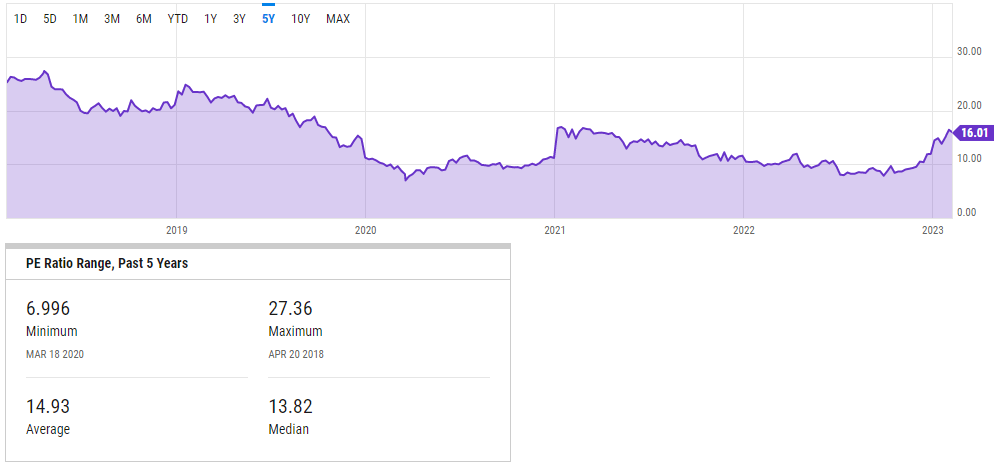

Overall, I think that it was a decent year for Embotelladora Andina, and a net income of $147.8 million sounds relatively low for a company with a market capitalization of $2.22 billion as of the time of writing. Historically, both Series A and Series B shares are currently slightly above the median for the past 5 years in terms of P/E. However, they are much lower than their 2019 levels.

Series A:

YCharts

Series B:

YCharts

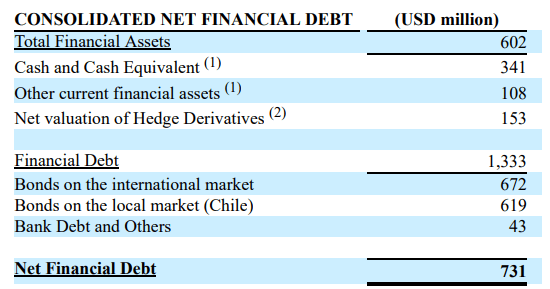

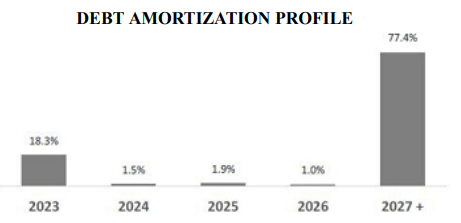

Turning our attention to the balance sheet, debt levels seem manageable, and I don’t expect the company to be affected by rising interest rates significantly for the time being as most of its debt is payable after 2026. As of December 2022, the net financial debt of Embotelladora Andina stood at $731 million and the net debt-to-EBITDA ratio was 1.3x.

Embotelladora Andina

Embotelladora Andina

Looking at the dividend situation, payments for Series A ADRs over the past year came in at $1.94 per ADR, while those for Series A ADRs stood at $2.14 per ADR. This translates into dividend yields of 15.5% and 13.7% for Series A and Series B, respectively. As you can see, Series A ADRs offer a better bang for your buck in terms of dividend yield at the moment due to the significant difference between the price of the two classes of shares. To be fair, the dividend yield on both is likely to decline in 2023 as Embotelladora Andina paid a large extraordinary dividend in April 2022. The latest quarterly dividend for the Series A ADRs was $0.22 apiece which translates into a dividend yield of 7% on an annualized basis. In my view, the dividend yield levels will remain decent over the coming years as Embotelladora Andina is mandated by Chilean law to distribute at least 30% of its net profit as dividends.

Turning our attention to the risks for the bull case, I think there are two main ones. First, several countries in Latin America have undergone significant political regime change over the past two years and we’ve witnessed mass protests across Chile, Brazil, and more recently Peru. This could lead to an outflow of investment from the region which could slow down economic growth. Second, the beverage industry is cyclical in nature and most Latin American countries are expected to register slow GDP growth in 2023. A recession could lead to lower sales in the sector this year.

Investor takeaway

Embotelladora Andina booked strong sales in 2023 and the weaker U.S. dollar since the start of 2023 could provide a boost to its financial performance this year. The company doesn’t look expensive in terms of P/E considering it was trading above 20x in 2019. In addition, the company has a solid dividend yield, and it seems that Class A ADRs offer much better value for investors at the moment. Class B ADRs currently trade at a 25.2% discount over Class A ADRs, but are entitled to only 10% higher dividends.

Be the first to comment