Blue Planet Studio

Lithium mining and refining: the key to all things mid-21st century. And on Tesla’s (TSLA) conference call, Elon Musk called lithium refining a license to print money. He’s not far from the truth. With demand ramping up and supply slow to come online, there is an enormous gap predicted that should keep prices high and margins generous for those in the lithium industry: miners and refiners.

License to Print Money

Musk’s comments on Tesla’s conference call pointed out the key difficulty in lithium supply is getting it. He is right in that there is, in fact, a lot of lithium. However, I think this comment (though largely correct), understates some of the difficulties faced in mining.

Some commodities, the pricing of lithium is insane. I would like to once again urge entrepreneurs to enter the lithium refining business. The mining is relatively easy. The refining is much harder. So, the lithium is actually a very common – sort of very – like lithium pretty much everywhere. But you have to refine the lithium into battery-grade lithium carbonate and lithium hydroxide, which has to be extremely high purity. So, it is basically like minting money right now. There is like software margins in lithium processing right now. So, I would really like to encourage, once again, entrepreneurs to enter the lithium refining business. You can’t lose. It’s a license to print money.

(Emphasis by author)

Lithium mining is not exactly a walk in the park either, between the capital needed, permits, technical surveys, construction time, transportation, and water rights. And many mining companies are very profitable, even if they don’t refine all the way to the level of lithium carbonate (such as Sigma Lithium (SGML), which plans on producing lithium concentrate, one level below carbonate or hydroxide). The reason lithium is so profitable regardless is that there is such a clear supply gap, that is only expected to widen.

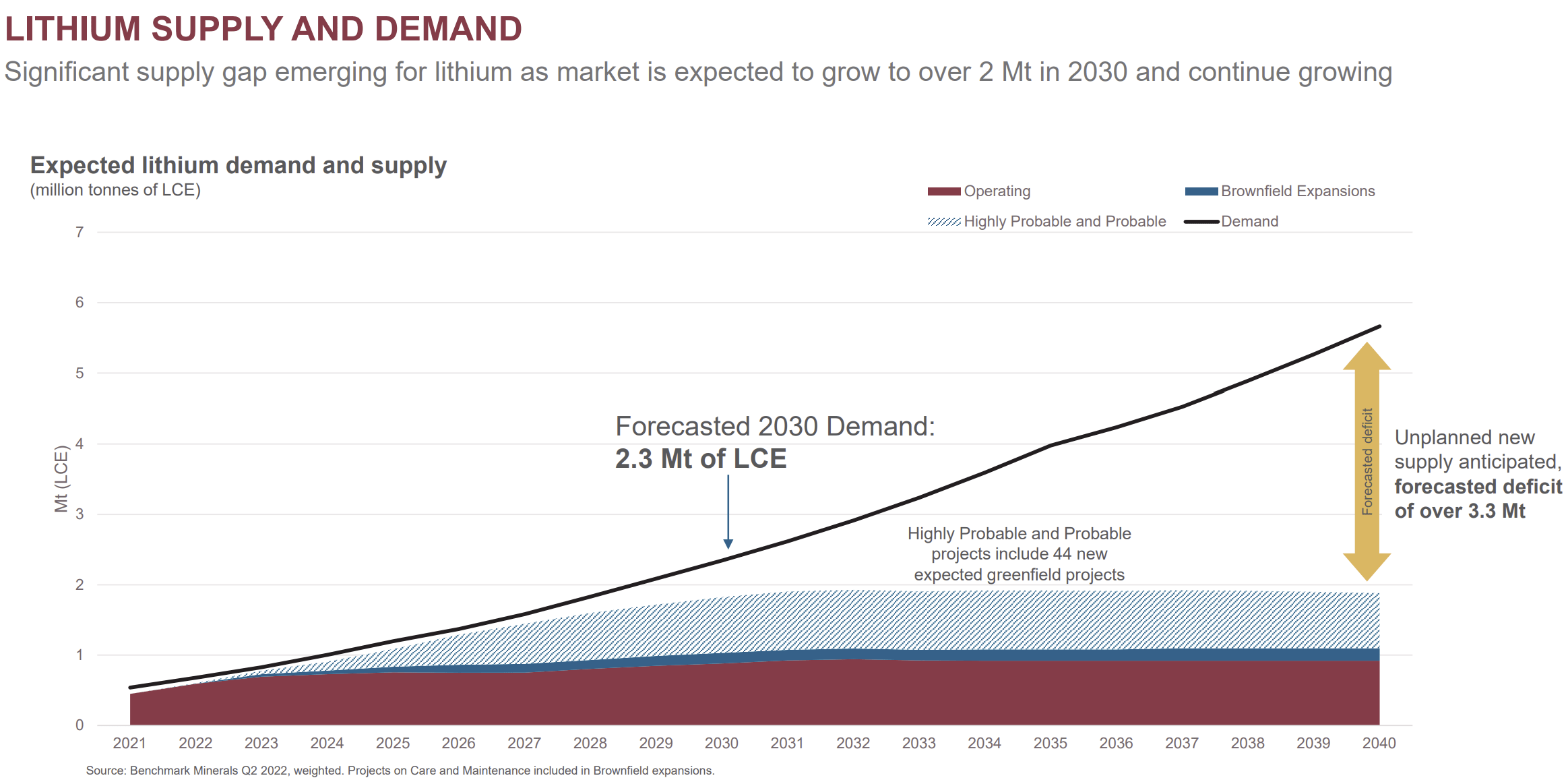

Lithium Americas July Presentation

And most companies (outside of China) that are involved in lithium refining also have a hand in the mining business. The largest new lithium development project in the United States, Thacker Pass by Lithium Americas (LAC), recently announced the official opening of its lithium technical development center before the actual mine has even begun construction. This facility began production in June and shows the company’s processing capability from the ore to refined lithium carbonate.

Additionally, Lithium Americas is now searching for a contractor to oversee the construction of the mine itself and is anticipating a final decision from the Federal court as to whether the project can proceed within the next month or two after briefings conclude on August 11. If successful, the company’s site is very well positioned to be a lithium carbonate provider to Tesla’s Nevada gigafactory and other companies on the West Coast.

This integrated extraction to lithium carbonate or hydroxide design seems to be predominant in many new projects as companies sign offtake agreements directly with the mining companies for lithium carbonate/hydroxide.

A few companies have opted for the refining-first route, securing spodumene ore and building plants to refine it into lithium hydroxide, but they are far from the majority. One such company is Piedmont Lithium (PLL), a company I previously mentioned as being more of a refiner than a producer. The company has offtake agreements with several mines for ore that it plans to turn into 30,000 tonnes per annum of lithium hydroxide (maybe more if it can build a second Canadian plant). But the reason Piedmont is turning out as a refiner is that the company has had immense difficulties getting its own mine permitted. For companies focused on refining, margins may face pressure as the raw lithium is not exactly cheap (spodumene prices have soared past $6000 per tonne in recent months) and the terms of offtake agreements for those focused on processing will be important.

And other existing lithium juggernauts are not to be counted out either, like SQM (SQM), Albemarle (ALB), and Livent (LTHM). These players are integrated and all have plans for further expansion to capitalize on growing demand.

There is also a strong case for recycling plays like Li-Cycle (LICY) to be an integral part of the lithium supply chain. As battery production ramps up, reprocessing the scraps and end-of-life batteries into new battery-grade materials will be a key source of lithium (and other metals) that is easily accessible and close to the hubs of battery production.

Tesla Isn’t Getting Into the Lithium Industry

Despite his conference call comments about the shortage of refining capacity to provide battery-grade lithium carbonate and hydroxide, Musk was fairly clear on a podcast back in early July that Tesla will not directly enter the lithium business as some have speculated:

“Well, we don’t want to go into the mining industry or the sort of refining industry because the limitation, I think, is actually more. For example, with lithium, it’s more lithium refinement than it is the actual mining. So you better take the ore that contains lithium, and you’ve got to refine it and get it to battery-grade lithium hydroxide or lithium carbonate. And it has to be extremely pure. Otherwise, you could have a breakdown in the cell.

Though Musk did add an asterisk on the conference call that suggests Tesla may yet get into the lithium business if it can’t secure enough supply:

Yes. If our suppliers don’t solve these problems, then we will.

Changing Battery Chemistry

Musk also mentioned on the conference call that he thinks that a substantial amount of batteries will be iron phosphate over the next few years:

As it was also difficult to create the anode and cathode, I think – my guess is maybe two-thirds of batteries will be iron phosphate or maybe iron phosphate with some manganese.

However, despite the way it might sound, this is still a lithium-based battery. Lithium iron phosphate batteries (LiFePO4) have been gaining in popularity as they are cheaper, safer, and last longer than lithium-ion batteries (though they can have less range in EVs).

Just this week, Ford (F) announced that it is partnering with CATL to source lithium iron phosphate batteries for some of its cheaper models. Ford also said that it has secured 70% of the batteries it needs for its goal of producing 2 million EVs by 2026. This was helped along by another deal to secure 7,000 tonnes per annum of lithium carbonate from ioneer’s (IONR) Nevada project. Though this does show Ford is working to secure its supply, a 30% gap is nothing to be trifled with and shows there is still plenty of demand out there for new lithium supply.

Takeaway

Lithium is the fuel of the future, that much is clear. Elon Musk’s emphasis on the importance of refining is also noteworthy and points out how the US especially lacks a domestic supply chain. However, access to raw lithium is also important and a prerequisite to being able to refine in the first place. Over the coming decade, I believe some of the most successful lithium plays will be low-cost integrated producers that can extract and refine lithium at the same site, such as Lithium Americas.

Be the first to comment