Torsten Asmus

Thesis

BlackRock Enhanced Government Fund (NYSE:EGF) is a fixed income closed end fund. The fund’s primary objective is current income, and it seeks to achieve said objective –

[…] by investing primarily in a portfolio of US Government securities and US Government Agency securities, including US Government mortgage-backed securities that pay interest in an attempt to generate current income, and by employing a strategy of writing (selling) call options on individual or baskets of US Government securities, US Government Agency securities or other debt securities held by the Fund in an attempt to generate gains from option premiums.

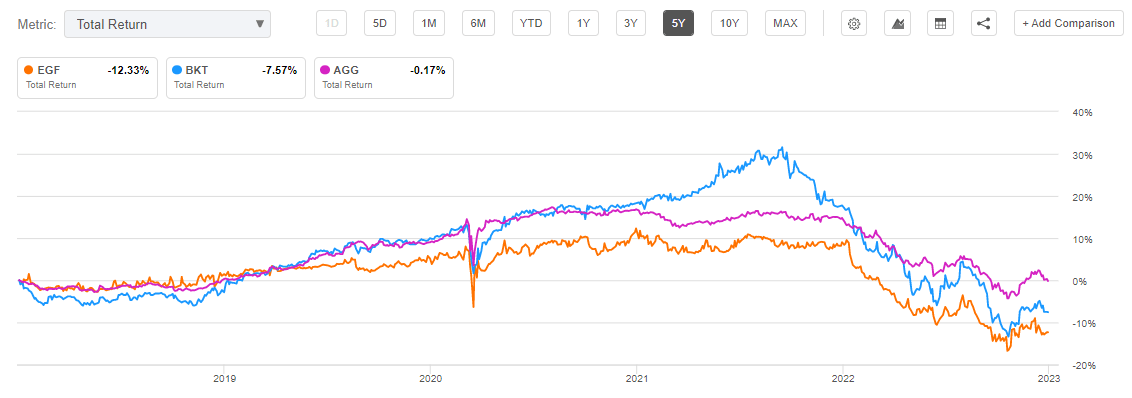

EGF is basically an Agency mortgage and Treasury CEF. What distinguishes this CEF from others in the space is the fact that it gives away some of its upside via writing call options on its underlying portfolio. This is not ideal since until 2022 bond volatility (as measured by the MOVE Index) was not high enough to justify such upside capping. Not surprisingly EGF has had a very uninspiring performance in the past 5 years, especially when compared to another similar fund from the BlackRock suite, namely BlackRock Income Trust (BKT). During this time frame EGF is down -12%, while BKT is down -7%.

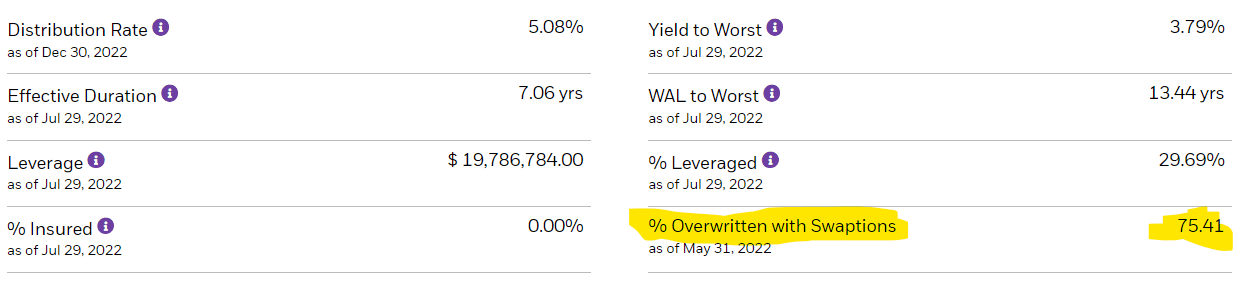

Currently, EGF is composed of 50% Agency Mortgages, 41% U.S. Treasuries and the rest split between securitized products and investment grade bonds. Think of this CEF as a 50/50 Agency Mortgages/Treasuries fund. More importantly, 75% of the portfolio is capped via written options:

Fund Details (Fund Website)

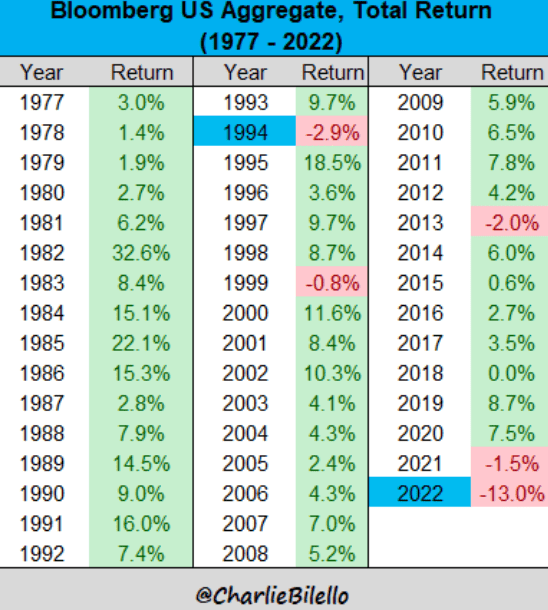

The fund has an intermediate duration of 7 years, and a leverage ratio of 30%. Last year was the worst on record for the aggregate bond market:

AGG Total Return (Charlie Bilello)

For long only funds there will be better times ahead. EGF however, has a lot of the upside capped via its written options structure. We are not big fans of this fund. The bond world used to be a very low volatility one and writing options on top to cap the upside never really yielded meaningful results.

EGF was not able to outperform in 2022 either when comparing it to BKT. When the top in rates will be in, the fund will have a limited upside given its propensity to overwrite the portfolio with options. Not protected in a bond downturn and with a capped upside, this fund is best to be avoided.

Analytics

AUM: $0.04 bil

Discount to NAV: -7%

Z-Stat: -1

Yield: 5%

St Dev: 4.4

Sharpe Ratio: -0.76

EGF Performance

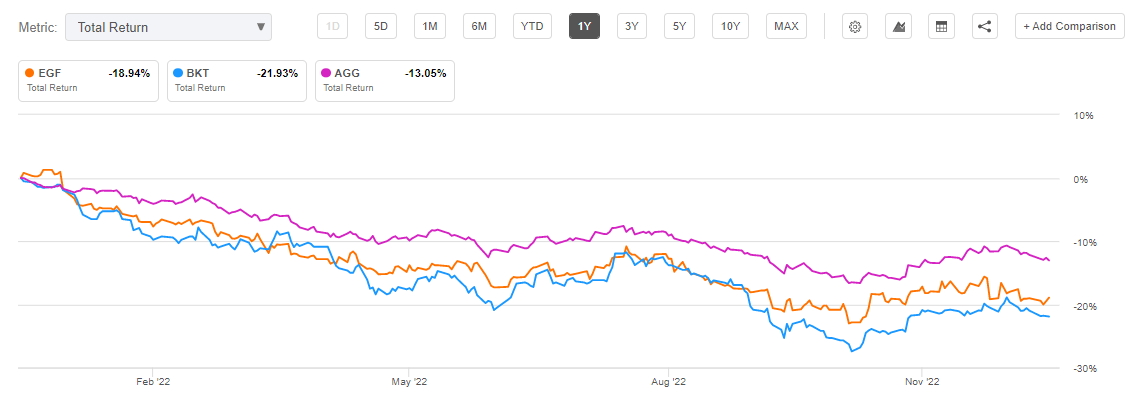

The fund was down almost -19% in 2022:

Total Return (Seeking Alpha)

We are benchmarking the CEF versus an Agency MBS CEF, namely Blackrock Income Trust, and against the iShares Core U.S. Aggregate Bond ETF (AGG), a bellwether of the bond market.

On a 5-year basis EGF disappoints:

Total Return (5Y) (Seeking Alpha)

We can see how the fund is the worst performing from the cohort, but more importantly, it never goes above a 10% total return level. This is due to the option writing strategy that caps the upside.

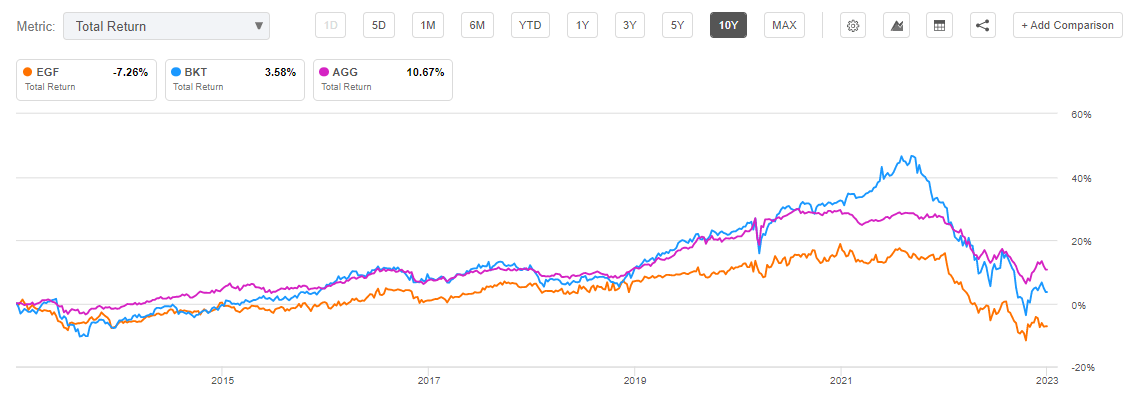

The same story is revealed by a decade-long chart:

Total Return (10Y) (Seeking Alpha)

Holdings

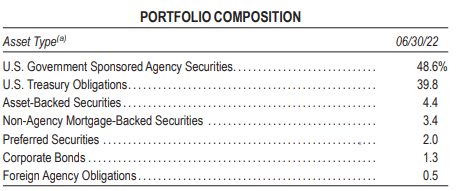

As of the latest Semi-Annual Report, the fund’s holdings are as follows:

Portfolio Composition (Semi-Annual Report)

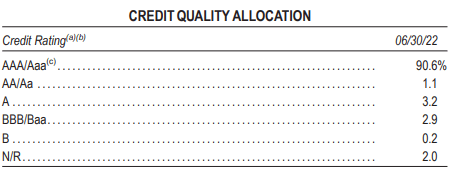

The vehicle is pretty much entirely investment grade from a ratings perspective:

Ratings (Semi-Annual Report)

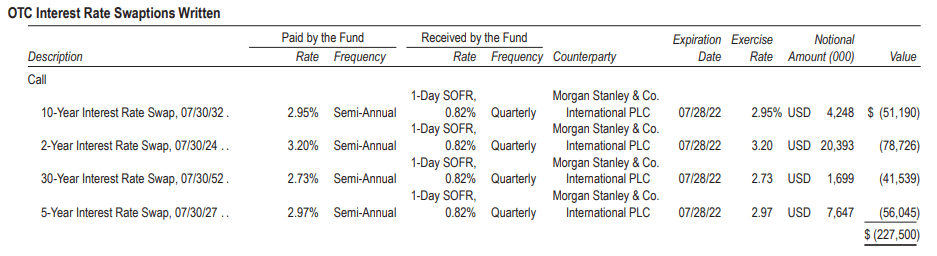

The Semi-Annual Report also contains a more detailed snapshot of the swaptions utilized at that point in time:

Swaptions (Semi-Annual Report)

Please note that as a long bond fund the vehicle receives fixed rates. To note that the capping is realized by pay fixed swaptions as seen in the above snapshot from the Semi-Annual Report.

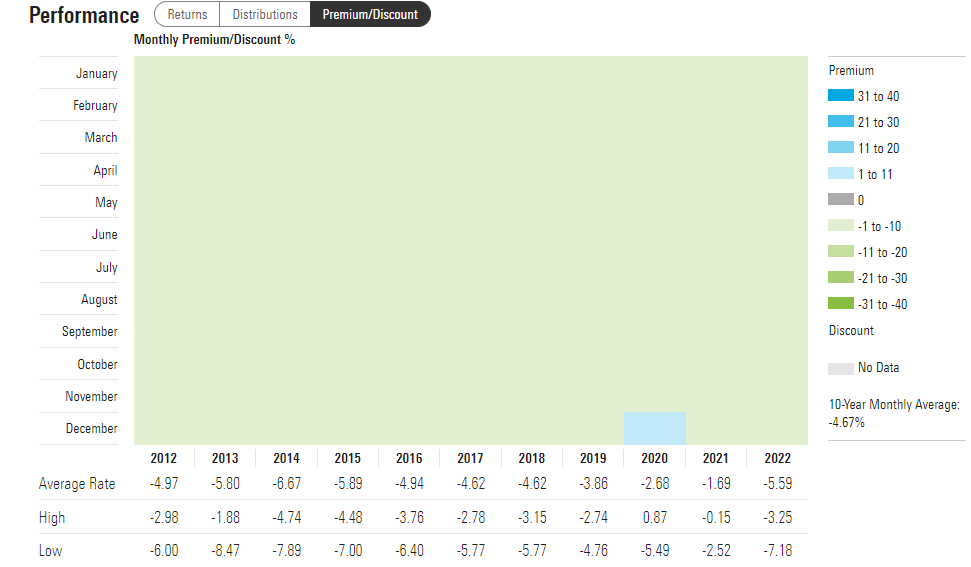

Premium / Discount to NAV

The fund has traded fairly consistently at discounts to net asset value:

Premium / Discount (Morningstar)

There is only a brief period in 2020 when we saw a premium to NAV here, but otherwise the CEF has averaged a -5% discount to NAV. We feel this is warranted given its underperformance and set-up. There is nothing here to warrant a premium to NAV.

Conclusion

EGF is a fixed income CEF. The fund has a composition that currently shakes out at 50% Agency Mortgages, 41% U.S. Treasuries and the rest split between securitized products and investment grade bonds. The structure layers a 30% leverage ratio on top and has overwritten the portfolio with swaptions. The written call option feature never really worked because volatility was too low in the bond market. The fund has not managed to outperform in 2022, being down in line with a pure Agency leveraged MBS play, namely (BKT). What is more worrying though is that the fund gives away a lot of the upside via the written call option feature. If we look at its historical performance, this feature has really dampened its performance versus pure long funds. The CEF has consistently traded at a -5% discount due to its poor returns and capped features. With peak rates coming in soon, a retail investor should move towards true long bond funds (either vanilla or leveraged) to capture the upside. We are thinking here about the likes of (EDV) where we have slapped a Buy rating here. We are not fans of EGF and we feel a retail investor is best served to avoid this name.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment