Laurence Dutton/E+ via Getty Images

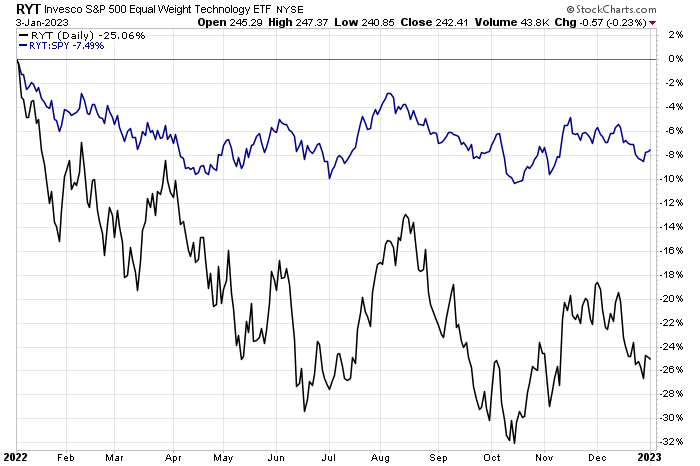

Equal-weight strategies are catching some fanfare right now. With mega-cap tech’s selloff, as seen in the Nasdaq 100’s more than 30% 2022 drop, there is growing interest in owning non-cap-weighted products. One fund you should eye is the Invesco S&P 500 Equal Weight Technology ETF (RYT). The fund dropped in the first quarter of last year versus the S&P 500, but then traded sideways. While Cathie Wood ARKK stocks have struggled, RYT has stabilized somewhat. One of its components features a low valuation, but is it a buy now? Let’s weigh the risks in DXC.

Equal-Weight Tech Steadies vs SPX

Stockcharts.com

According to Bank of America Global Research, DXC Technology (NYSE:DXC) is the world’s second-largest pure-play IT services firm, behind only Accenture, and was formed by the merger of CSC and HPE-ES. In FY2021 pro forma DXC generated around $17.7B in annual revenues. Moreover, as of F21, the company had 130k+ employees, serves clients in a wide range of verticals, and had a presence in 70+ countries.

The Virginia-based $6.1 billion market cap IT Services industry company within the Information Technology sector trades at a low 9.0 trailing 12-month GAAP price-to-earnings ratio and does not pay a dividend, according to The Wall Street Journal. DXC has been at the center of some takeover chatter from a financial suiter, which has helped the stock lately. Still, its cyclical nature and exposure to weak growth in Europe are risks. The firm beat estimates in its Q3 report back in November and it has an upcoming earnings date.

On valuation, analysts at BofA see earnings having risen sharply in 2022 but then stalling out in this coming year. EPS is then seen as reaccelerating in 2024 before steadying near +11% in 2025. The Bloomberg consensus forecast is a bit more upbeat in ‘23 and ‘24 compared to BofA.

DXC’s operating P/E is seen as falling further into the single digits while the GAAP earnings multiple is a touch higher. Being a decent growth company, the EV/EBITDA ratio is actually low compared to the market while free cash flow is high. Overall, I like the valuation and Seeking Alpha rates it with an A.

DXC: Earnings, Valuation, Free Cash Flow Forecasts

BofA Global Research

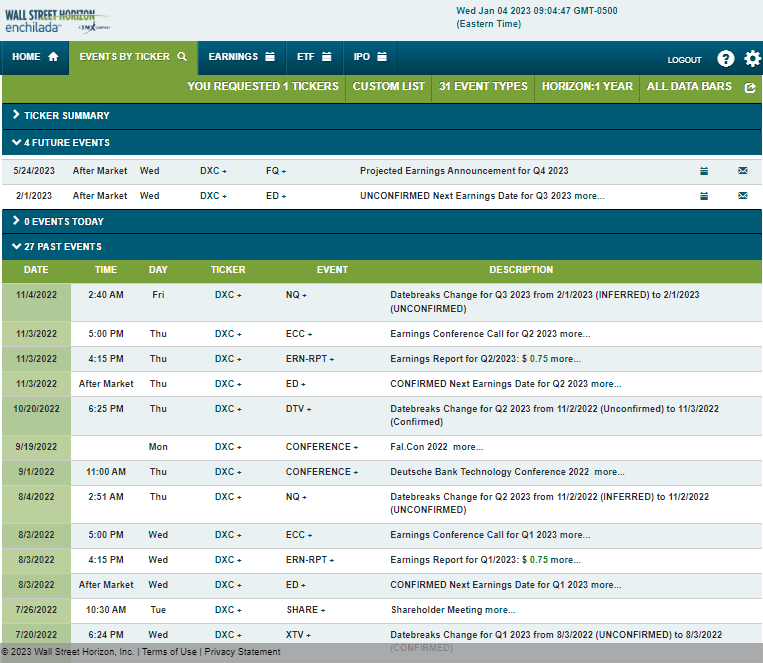

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q3 2023 earnings date of Wednesday, February 1 AMC. The calendar is light on volatility catalysts until then though.

Corporate Event Calendar

Wall Street Horizon

The Options Angle

Digging into the upcoming earnings report, data from Option Research & Technology Services (ORATS) show a consensus Q3 EPS forecast of $0.84 which would be a 9% drop from per-share profits earned in the same quarter a year ago. DXC has beaten analysts’ estimates in 10 of the previous 12 reports but has missed two of the last three. Shares have a mixed earnings reaction history with the stock generally rising or falling between +15% and –15%.

Ahead of next month’s report, the options market has priced in an 8.6% earnings-related stock swing using the at-the-money straddle that expires soonest after the reporting date. Given some big moves in recent reports, I would be long premium ahead of the Feb. 1 date.

DXC: An Earnings Decline Expected, Cheap Options Premium

ORATS

The Technical Take

DXC is stuck in a downtrend. Notice in the chart below that shares peaked above $44 back in the third quarter of 2021 and were slowly but surely cut in half by the low notched in early October this year. The stock managed to stage a rally to the falling 200-day moving average this past quarter, but sellers emerged where you’d expect. I would like to see the stock break above its downtrend resistance line currently near $30. Until that breaks with vigor, shares might have a near-term downside to the low $20s.

DXC: Stuck In A Downtrend

Stockcharts.com

The Bottom Line

I like the valuation and growth outlook for DXC, but the chart warrants caution for now. This will be one to watch in the coming quarters should it break from its downtrend or if it drifts to the lower end of the channel.

Be the first to comment