Dilok Klaisataporn

The iShares Select Dividend ETF (NASDAQ:DVY) seems like it has a fair bit to offer. Among the top holdings are stocks we already like from a value perspective. The yield is fair and we think that it is a nice, non-consensus portfolio that doesn’t just allocate to the largest cap names. The recession resilience is likely quite strong too, with latent macro problems yet to take their toll on markets. We think ETF investors could rest quite easy with DVY.

DVY Breakdown

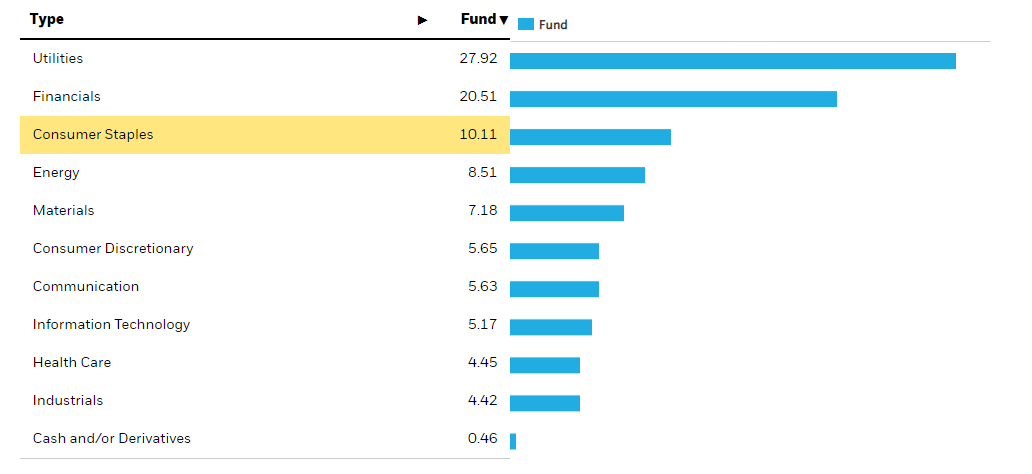

Let’s start with a sector-based breakdown.

Sector Breakdown (iShares.com)

For a US ETF, we already see something peculiar, which is the atypical allocation into things outside of IT. The majority of the ETF is in utilities, then financials and then consumer staples. These are some of the more resilient sectors for the current economic environment. The first sells a total necessity, and is sometimes compensated for operating regulated concessions with toll-like remuneration schemes. Utilities are a strong sector in a recession, and are benefiting from high prices in the commodities they sell too. The second are financials, which are benefiting either from higher insurance portfolio yields which are allocated dramatically towards short maturity bonds, or are benefiting from the greater interest income spread between lagging savings rates and higher lending rates. Finally, consumer staples are by design a sector that should see resilience.

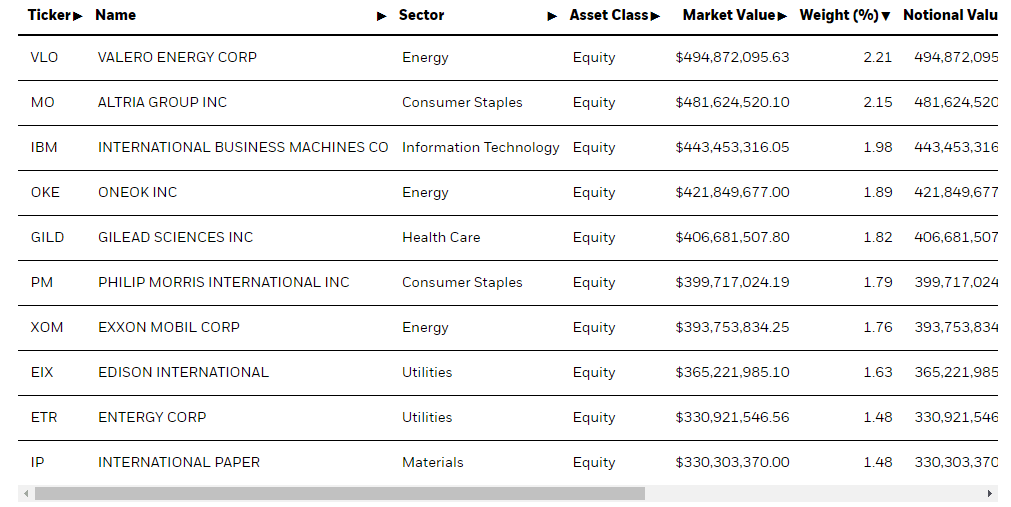

DVY Holdings (iShares.com)

While a relatively well diversified portfolio, looking at the top holdings we see some picks that account for a more relevant portion of the portfolio that we like. Valero (VLO) earns on the basis of crack-spreads, which are currently high but could fall, but do benefit from some recession resilience because run-cuts typically bring on lower crude prices, which are their feedstock, so their spreads are somewhat well protected. Moreover, there is a structural lack in refining capacity right now that benefits the industry from a supply perspective. Then there is Altria (MO). Personally, it is our least favourite tobacco exposure because of legal troubles over the IQOS rollout, and winner-take-all dynamics in heat not burn. Nonetheless, it has good non-combustibles in its portfolio, decent discount exposures in the case of downtrading, and the strongest tobacco brand (Marlboro) in the world with license in the US market. IBM (IBM) has Red Hat, which benefits from network economics and is making waves, especially as the company became more lean after its infrastructure spinoff. ONEOK (OKE) is a solid commodity logistics play and Gilead (GILD) has the strongest HIV franchise which is finally growing. Philip Morris (PM) is the most premier tobacco exposure on offer.

Conclusions

The PE lies just below the 13x level. That’s rather good, and represents a pretty solid earnings yield of 7.7%. With stocks that generally are either resilient to interest rate hikes and a recession, which could come as a reckoning of already evident declines in consumer confidence, and can flex pricing power with inflation, that earnings yield is rather safe, and potentially able to grow from today’s entry point. The yield is 3%, which is respectable, but not overwhelming like with a REIT. Importantly, the portfolio is non-consensus. While not exactly mid-cap, things don’t get too big here, and you aren’t swimming with whale allocators by owning (even if by ETF proxy) the stocks inside DVY. Non-consensus and value oriented stocks are a good pick when markets are in a state of flux, because the more known they are and the bigger they are, the harder they can fall when expectations change. This is a SWAN investment and there is both value and yield here. DVY looks solid.

While we don’t often do macroeconomic opinions, we do occasionally on our marketplace service here on Seeking Alpha, The Value Lab. We focus on long-only value ideas, where we try to find international mispriced equities and target a portfolio yield of about 4%. We’ve done really well for ourselves over the last 5 years, but it took getting our hands dirty in international markets. If you are a value-investor, serious about protecting your wealth, us at the Value Lab might be of inspiration. Give our no-strings-attached free trial a try to see if it’s for you.

Be the first to comment