Artur

Duolingo (NASDAQ:DUOL) is one of the world’s most popular language learning app with 56.5m monthly active users (MAUs) and 3.7m paid subscribers. Under their freemium model, language learners can either use Duolingo for free with ads (ad-supported plan) or pay a small subscription fee ($6.99/month for their most popular plan) to escape ads and gain access to other features (Super Duolingo).

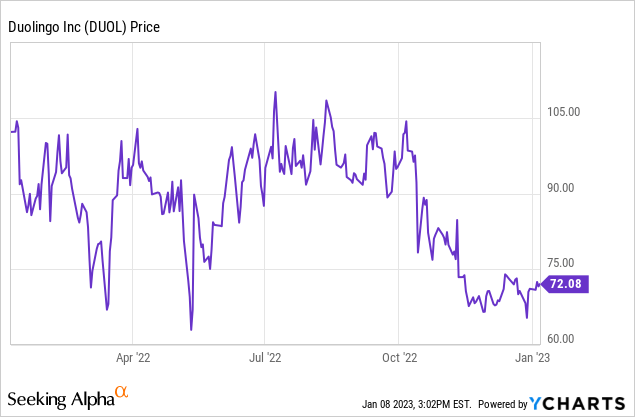

Despite comfortably beating their internal revenue and adjusted EBITDA guidance through the first three quarters of 2022, Duolingo’s share price has fallen 30% over the past 12 months. For some context, the Nasdaq Composite Index is down 29% over this same 12-month period.

| Quarter | Revenue Guidance (Midpoint) | Revenue (Actual) | Beat vs. Guidance (%) | Adjusted EBITDA Guidance (Midpoint) | Adjusted EBITDA (Actual) | Beat vs. Guidance (%) |

| Q3 2022 | $94.5m | $96.1m | 2% | ($3.0m) | $2.1m | n/a |

| Q2 2022 | $85.5m | $88.4m | 5% | ($2.5m) | $4.2m | n/a |

| Q1 2022 | $77.0m | $81.2m | 5% | ($4.0m) | $3.9m | n/a |

Although Duolingo’s operational performance has been strong so far throughout 2022 (see my breakdown of their latest Q3 results here), there is a material risk that upcoming quarters will be below expectations following a recent update which has been met with substantial backlash from users. As a Duolingo shareholder, I am concerned about this increasing user dissatisfaction and believe it warrants caution ahead of their upcoming Q4 results.

A Radical Change to the Home Screen

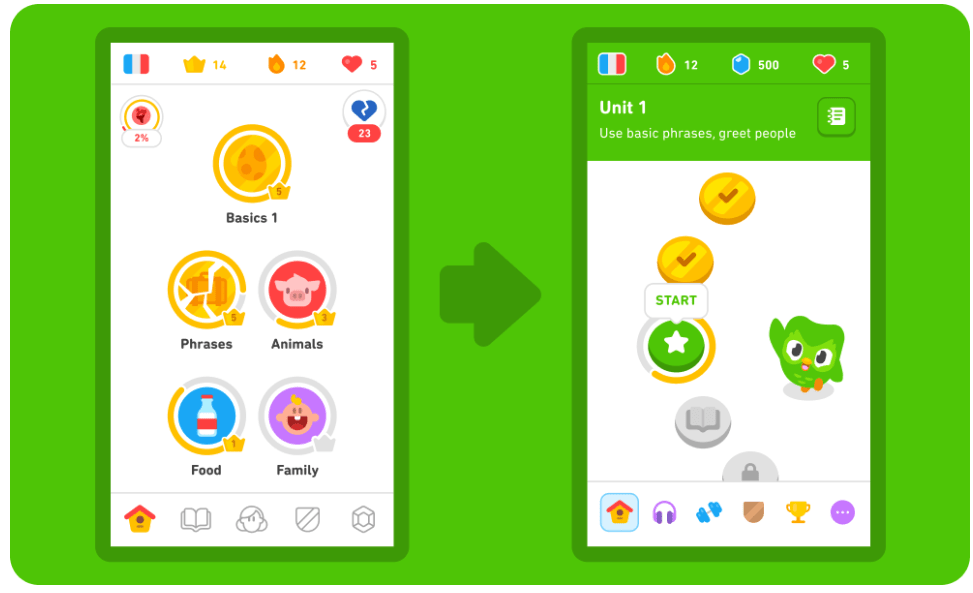

Over the course of 2022, Duolingo gradually rolled out a complete redesign of their home screen, the main interface through which users select their upcoming language lessons. Duolingo formerly used a “tree” design where learners had lots of flexibility to choose which lesson they wanted to study on a given day. Don’t feel like studying family today? You can study animals instead! Lessons that had been mastered but not revised for an extended period (e.g., phrases in the below figure) appeared as “cracked” to prompt learners to consolidate that content.

In the new update, Duolingo switched to a “path” design which is more constrained and forces learners to complete lessons in a pre-determined order. Lessons have been grouped into smaller units and stories are now built into the learning path, rather than an optional extra. There is no longer a need to revise “cracked” lessons as personalised practice lessons are built into the path. According to Duolingo, all progress from the old “tree” model was transferred in full to the newer “path” model (including that precious daily streak!).

Duolingo Home Screen Update (Duolingo Website)

Controversy and User Backlash

Duolingo is known for their data-driven approach to updating their core language learning app. As such, this home page redesign would have undergone substantial A-B testing and initial feedback was clearly positive enough to warrant rolling it out to their entire base of ad-supported/premium users.

In their Q1 shareholder letter, Duolingo management foreshadowed several benefits of their app redesign:

- Grow Users. We believe the new path will drive more engagement and give lapsed learners a reason to return to their language learning. We will also feature our cast of characters and animations along the path to add delight to the experience.

- Grow Subscribers. Ultimately, if we continue to improve how well we teach, and our learners are more engaged, this will translate into more paid subscriptions.

Moreover, in Duolingo’s latest Q3 results, user growth accelerated for the fifth consecutive quarter:

We’re not seeing any signs of consumer softness in our subscription metrics and as a result, we’re raising our full year guidance again … Daily and monthly active users continue to accelerate for the fifth quarter in a row, reaching all-time highs in this third quarter.

– Duolingo CEO Luis von Ahn, Q3 2022 Earnings Call

At this stage, evidence from Duolingo’s latest quarterly results suggests a successful rollout of their new app redesign.

However, this data point lies in stark contrast to public user feedback on Reddit, other online forums, and app stores. After spending hours reading through these recent reviews, I would estimate that 80%+ are strongly negative, with many of these disgruntled users threatening to cancel their Super Duolingo subscription and switch to a competing language learning app, such as Babbel or Rosetta Stone.

The negative reviews have largely been centered around five core concerns:

| Concern | Description |

| 1) Too linear/restrictive |

The new learning path feels too linear and restrictive. People want more flexibility in what lessons they are able to complete on a given day. People feel as though they are being treated like “child learners” rather than “adult learners”. |

| 2) Progress not accurately transferred |

Some past progress has not accurately transferred to the newer “path” model. Learners have not been given credit for old mastered lessons or are now being tested on content they have never learned. |

| 3) Less motivated to use the app |

Users feel less motivated to complete lessons and use the app following the home page update. Many online reviewers lost their 1,000+ day streaks due to this decreased motivation. |

| 4) Abrupt rollout | The rollout of the home page redesign was unnecessarily abrupt and the rationale could have been better communicated by management. |

| 5) Management does not care about their users | Management have persisted with rollout of the new home page despite strong negative feedback from users. Moreover, there have been no concessions/adjustments based on user feedback. This shows that Duolingo management are more concerned about short-term profits than their users. |

This avalanche of negative feedback culminated in a petition for Duolingo to revert back to their classic “tree” learning model (or at least provide users with the option to choose their preferred path). To date, this petition has been signed by almost 14,000 users. While this number represents a drop in the bucket of Duolingo’s 56.5m MAUs, the trend is concerning, particularly as it has been picked up by several media outlets and could materially damage Duolingo’s brand.

With this situation, I acknowledge the risk of bias when using a collection of individual user feedback to infer the opinion of the masses, as those with stronger opinions (which tend to be negative) are more likely to leave public reviews than those with neutral/slightly positive reviews. Nonetheless, I would highly encourage interested readers to check out recent Duolingo app reviews on both the App Store and Google Play stores for some perspective.

My Personal Experience

I must admit that my first experience with the app redesign was strongly negative. For a fortnight, I felt very demotivated to use Duolingo and only completed one lesson per day to maintain my streak. This lies in contrast to the 4-5 lessons I used to complete, on average, each day before the app update. I disliked being forced to complete lessons in a pre-determined order (sometimes I want a break from learning obscure animal names!) and progress felt much slower under this newer “path” model.

However, since that initial reaction, I’ve grown to enjoy and appreciate the updated home page. The learning path is simpler, the guidebook is more tailored towards the specific lesson being completed, and having personalised practice and stories inbuilt into the learning path makes for a more varied learning experience. Overall, it just took a few weeks to adjust to the new design.

What Impact Could This User Backlash Have on Duolingo’s Business?

The above anecdotal evidence suggests that Duolingo’s upcoming Q4 results (and beyond) could be worse than expected. If users are indeed this dissatisfied with the recent update, it could lead to the following outcomes:

- Higher-than-average churn in paid subscribers.

- Slower acquisition of new users due to poorer perception of Duolingo’s brand.

- Slower conversion of ad-supported users to paid subscribers.

- Decreasing user engagement, which could lead to reduced purchases of in-app tokens.

Any combination of the above factors would materialise in slower revenue/bookings and user growth for Duolingo. It might also increase their customer acquisition cost and subsequent sales and marketing spend, which could impact adjusted EBITDA margins.

While all of the above outcomes are possible, I am unsure at this stage whether this public backlash represents a very serious and permanent impairment in Duolingo’s brand, or a temporary setback as users (like myself) adjust to the newer “path” learning model.

Drawing Comfort from Meta Platforms and Spotify

In looking for parallels to Duolingo’s current situation, I’m comforted by two recent PR scandals involving Meta Platforms (NASDAQ:META) and Spotify (NYSE:SPOT) which had minimal impacts on their core business.

I vividly remember the “boycott Facebook” movement in 2017-18 following the Cambridge Analytica scandal where many users threatened to leave Facebook’s platform. Despite the appearance of a powerful movement, Facebook continued to report strong user growth for the next 2-3 years and seemingly showed no signs of slowing down before their comical pivot into the metaverse.

Spotify also recently underwent a similar scandal following the suspected release of COVID-19 misinformation on their flagship podcast, The Joe Rogan Experience. In the following three quarters, however, Spotify continued to chalk up consistent year-over-year MAU growth of 19-20% with no meaningful increase in churn.

These examples show that public backlash from a highly vocal minority is often not enough to derail a good business with a strong brand and a dominant market position. The key concern here for Duolingo is whether these reviews represent the perspective of the minority or majority of users.

An Increasingly Attractive Valuation

While I like Duolingo’s business model, brand recognition, high gross margins, strong historical revenue/user growth, and founder-led management team, the high EV/sales multiple (combined with a lack of GAAP profitability) has always represented a cause for concern. After all, a good business can become a poor investment if the entry valuation is too high.

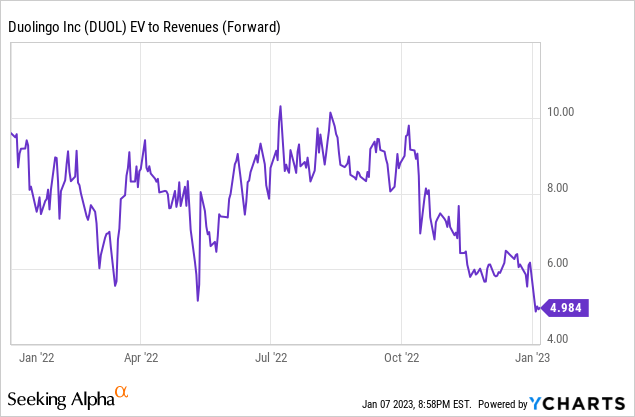

With the recent sell-off, Duolingo now trades at <5x forward revenues (based on analyst estimates) for the first time since their IPO in July 2021. EV/EBITDA multiples are not particularly meaningful at this stage of their profitability journey.

Despite the lack of GAAP profitability, Duolingo has consistently been free cash flow positive (arguably a more important metric than net income) each quarter since Q2 2020.

As research and development costs scale down as their major app redesign is complete and their stock-based compensation schedule normalises post-IPO, I expect Duolingo to generate positive net income sometime in the next 12-18 months. After this point, P/E and EV/EBITDA multiples will become more informative valuation metrics for investors.

The Take-Home Message

While there is a lot to like about Duolingo, the recent home page redesign and subsequent public backlash has substantially decreased the level of predictability relating to their user/revenue/bookings growth over the next few quarters.

While Duolingo’s app reviews still remain strong on an absolute basis (4.7/5 on App Store and 4.5/5 on Play Store), the overwhelming amount of recent scathing reviews and threats to “cancel Duolingo” has left me concerned about their upcoming Q4 results. As such, the path to increase MAUs by a 15% CAGR over the next five years (as outlined in my first article on Duolingo) is less certain and I think it is prudent to move my rating on Duolingo from “buy” to “hold”.

Duolingo has a strong balance sheet with a $554m net cash position (on a market cap of $2.90b), so there’s no balance sheet risk for the business if the next quarter or two are worse-than-expected. Nonetheless, I’ll need evidence that the core language learning business remains on track before purchasing more shares.

Be the first to comment