J Studios/DigitalVision via Getty Images

Introduction

Investing in the stock market can be a challenging task, with a plethora of options available to choose from. As an investor, it’s essential to weigh the potential risks and rewards of each stock, making informed decisions that align with your investment goals. While I often write about stocks that I find attractive, in this article, I want to take a different approach. I will be sharing my thoughts on two dividend stocks that I personally would not invest in, despite their attractive yield.

These stocks are not necessarily bad companies, but they present an unfavorable risk/reward ratio in my opinion. On the one hand, we have a stock with high volatility and economic risks, and on the other, a company with slow growth rates. In light of these concerns, I will also be providing alternative stocks for investors seeking high-yield opportunities with similar characteristics.

It’s important to note that this is solely my opinion, and it is not intended to be a negative reflection on the companies or their investors. This article serves as a cautionary tale, offering a glimpse into the stocks I personally would avoid and why.

So, let’s get to it!

Best Buy (BBY) – 4.1% Yield

I own one consumer discretionary stock. That company is Home Depot (HD), which I own because of its excellent execution in a highly competitive industry. The reason I don’t own more consumer stocks is that consumer cyclicals are often without a big moat. Especially in electronics retail, there are a few key things to keep in mind before diving in, as risks go well beyond the simple cyclical consumer risk.

-

Economic sensitivity: Cyclical consumer industries tend to be sensitive to changes in the economy. For example, during an economic recession, consumer spending on non-essential items such as electronics may decrease, leading to lower sales and profitability for companies in the industry.

-

Competitive landscape: The electronics retail industry is highly competitive, with several large players competing for market share. This can make it challenging for companies to maintain profitability and growth, especially in a down market.

-

Short product lifecycle: The electronics industry is characterized by rapid technological advancements and short product lifecycles, which can make it difficult for companies to keep up with the latest trends and maintain their market position. This can also lead to lower margins and profitability, as older products may become obsolete and harder to sell.

-

Price pressure: Companies in the electronics retail industry face significant price pressure from both online and brick-and-mortar competitors. This can lead to lower profit margins and make it challenging for companies to remain competitive.

-

Inventory risk: Companies in the electronics retail industry must manage the risk of having excess inventory if consumer demand for certain products decreases. This can result in markdowns, which can have a significant impact on the company’s financial performance.

With a market cap of $19.2 billion, Best Buy is the sixth-largest company operating in the specialty retail industry. The company operates more than 1,100 stores and focuses on six revenue categories: computing and mobile phones, consumer electronics, appliances, entertainment, services, and others.

What’s interesting is that the company’s 20 biggest suppliers accounted for 79% of its merchandise in fiscal 2022. The top five accounted for 56% of merchandise. These suppliers are Apple, Samsung, HP, LG, and Sony.

That said, I’m not worried about the power these suppliers have. If anything, Best Buy is in a good spot to benefit from its scale, which leads to attractive discounts when buying merchandise.

I’m also not worried about Best Buy’s ability to survive. They won’t go out of business. They are doing a tremendous job competing in a very tough market. While it may not lead to high growth, the added services when helping consumers pick products that are right for them are what keep physical stores alive.

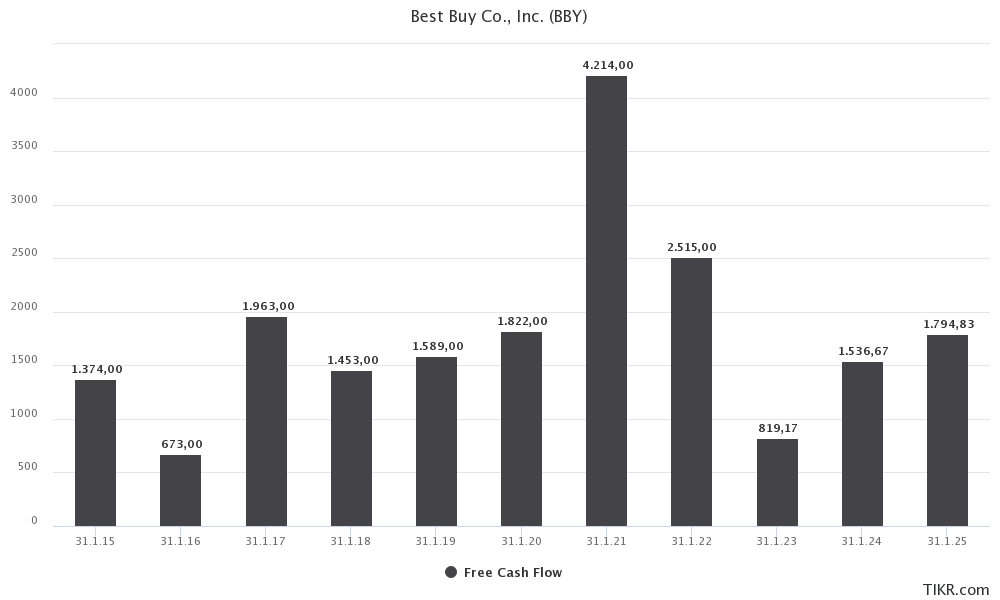

The company is consistently generating positive free cash flow, even in the year when the pandemic hit. In the current fiscal year, the company is set to make $1.5 billion in free cash flow. This translates to a 7.8% free cash flow yield. On top of that, it has a leverage ratio of less than 0.5x EBITDA and an A3 credit rating.

TIKR.com

These numbers not only mean that default risk is low but also mean that the company can prioritize its investors when it comes to cash distributions.

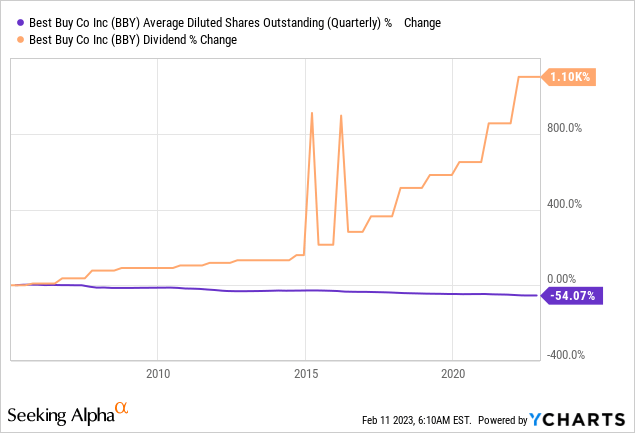

Since 2005, the company has repurchased 54% of its shares and hiked its dividend by 1,100%. The company did not cut its dividend during this period, including the Great Financial Crisis. The two spikes are special dividends.

Dividend growth has remained very strong.

- 10Y CAGR: 15.7%

- 5Y CAGR: 21.0%

- 3Y CAGR: 20.7%

The most recent hike was announced on March 3, 2022, when the company hiked by 25.7% to $0.88 per share per quarter. This implies a 4.1% dividend yield. Back then, the board also approved a $5 billion buyback program.

To reiterate, we’re dealing with a stock with strong double-digit dividend growth, a sustainable dividend thanks to high FCF, and a yield of more than 4.0%. And I’m calling it a bad stock?

Did I hit my head?

The reason I dislike BBY is because of the risks I described and the fact that free cash flow is not growing. Yes, it’s high and it ends up in investors’ pockets thanks to a healthy balance sheet, but it’s also volatile.

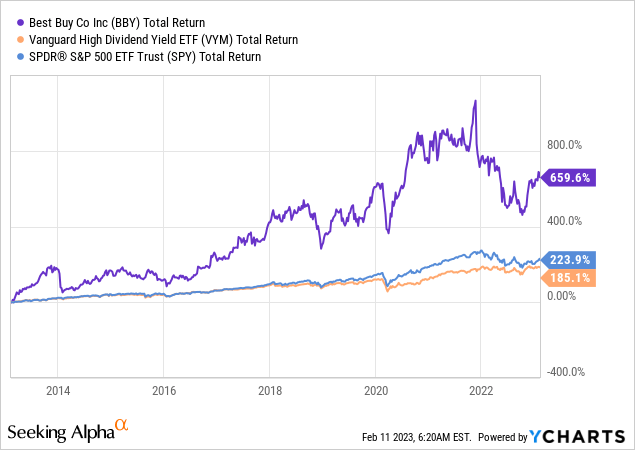

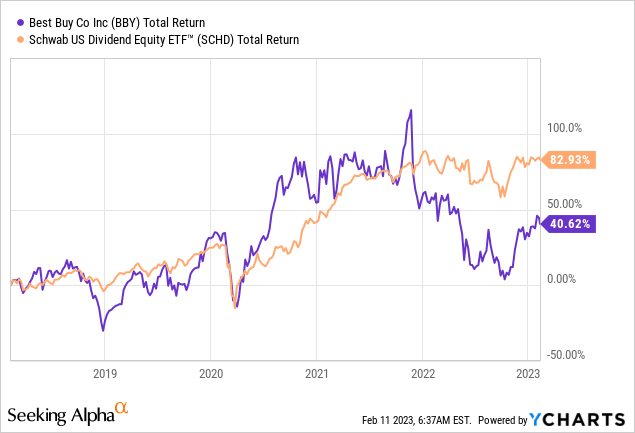

Over the past ten years, BBY shares have returned 660%, crushing everything in its path. The 3.0% yielding Vanguard High Dividend Yield ETF (VYM). returned just 185%. The S&P 500 returned 224%.

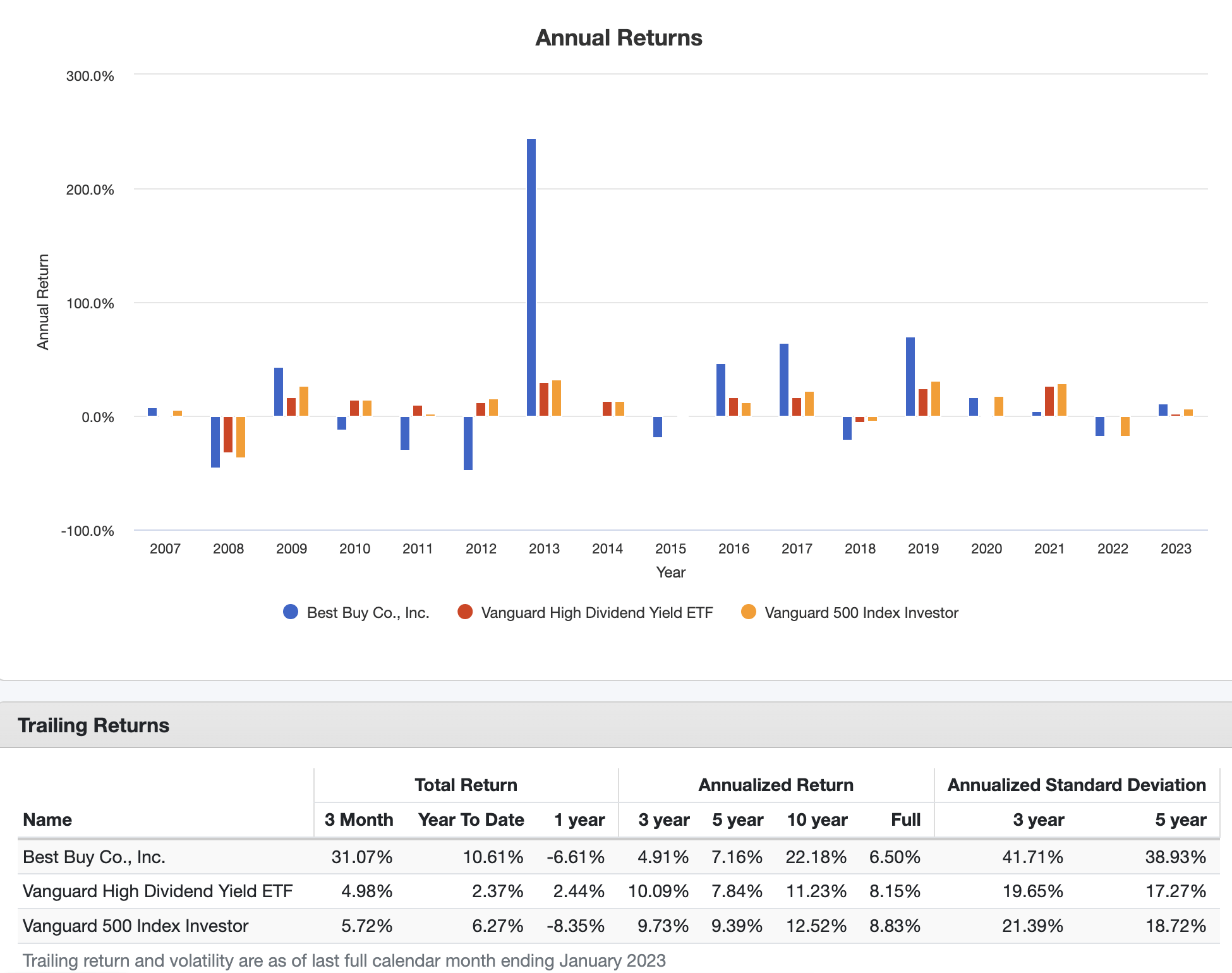

However, you would have only gotten that return if you bought the consumer bottom in 2012.

Looking at the data below, BBY exploded shortly after the Great Financial Crisis. Other than that, its returns have been subdued.

Portfolio Visualizer

For example, over the past five years, BBY returned 7.2% per year (including its dividend). That’s decent as it keeps up with the VYM ETF. However, it had a standard deviation (volatility) of almost 40%. That’s huge and comparable to some oil stocks.

Over the past three years, it has only gotten worse.

Going back to 2006, BBY has returned 6.5% per year with a 40% standard deviation. This has resulted in a Sharpe Ratio of just 0.3.

Now, the company is once again struggling with poor consumer health. While we have seen some improvement, these numbers remain poor.

Wells Fargo

In 3Q of the fiscal year 2023, comparable sales were down 10.4%.

Moreover, in the earnings transcript, it was noted that the promotional environment remains highly competitive compared to the previous year. In the third quarter, the level of promotions was similar to pre-pandemic levels and in some areas, even more aggressive, as the industry works to clear excess inventory and respond to softer demand from customers. Sales declines were seen across most product categories, with the largest impacts on enterprise comparable sales coming from the computing and home theater categories.

With all of this said, I’m not looking to get people to sell BBY. I’m sure a lot of readers bought BBY at cheap prices many years ago. My point is that I wouldn’t buy it today. Instead, I would go for a stock like Home Depot when trying to capitalize on a strong consumer industry in the US (in the future.

When looking for income, I would buy an ETF like the Schwab U.S. Dividend Equity ETF (SCHD), which comes with a 3.3% yield and very low volatility. I would prefer this over buying high-yield consumer stocks, as there’s no >4.0%-yielding stock on my list in that sector that I like a lot.

Going back to SCHD, the ETF has performed much better than BBY in the past five years – especially because of downside protection (a much lower volatility).

In summary, for income-seeking investments, I would consider conservative options such as an ETF or a REIT/utility that offer a steady dividend income. On the other hand, for investments with cyclical consumer exposure, I would opt for stocks with higher growth potential, even if it means a lower yield. I believe that the expected market weakness this year will present a favorable opportunity for investments like Home Depot which have higher growth prospects. I will continue to keep an eye on these investment opportunities and bring you more insights in the future.

Stock number two is different.

Campbell Soup (CPB) – 2.9% Yield

In recent months, Campbell Soup has garnered interest among investors seeking conservative dividend growth. The company, represented by the ticker symbol CPB, is often seen as a potential addition to investment portfolios for this reason.

Headquartered in Camden, New Jersey, Campbell’s history goes back to 1869. Since then, the company has grown into a packaged foods giant with a market cap of $15.3 billion.

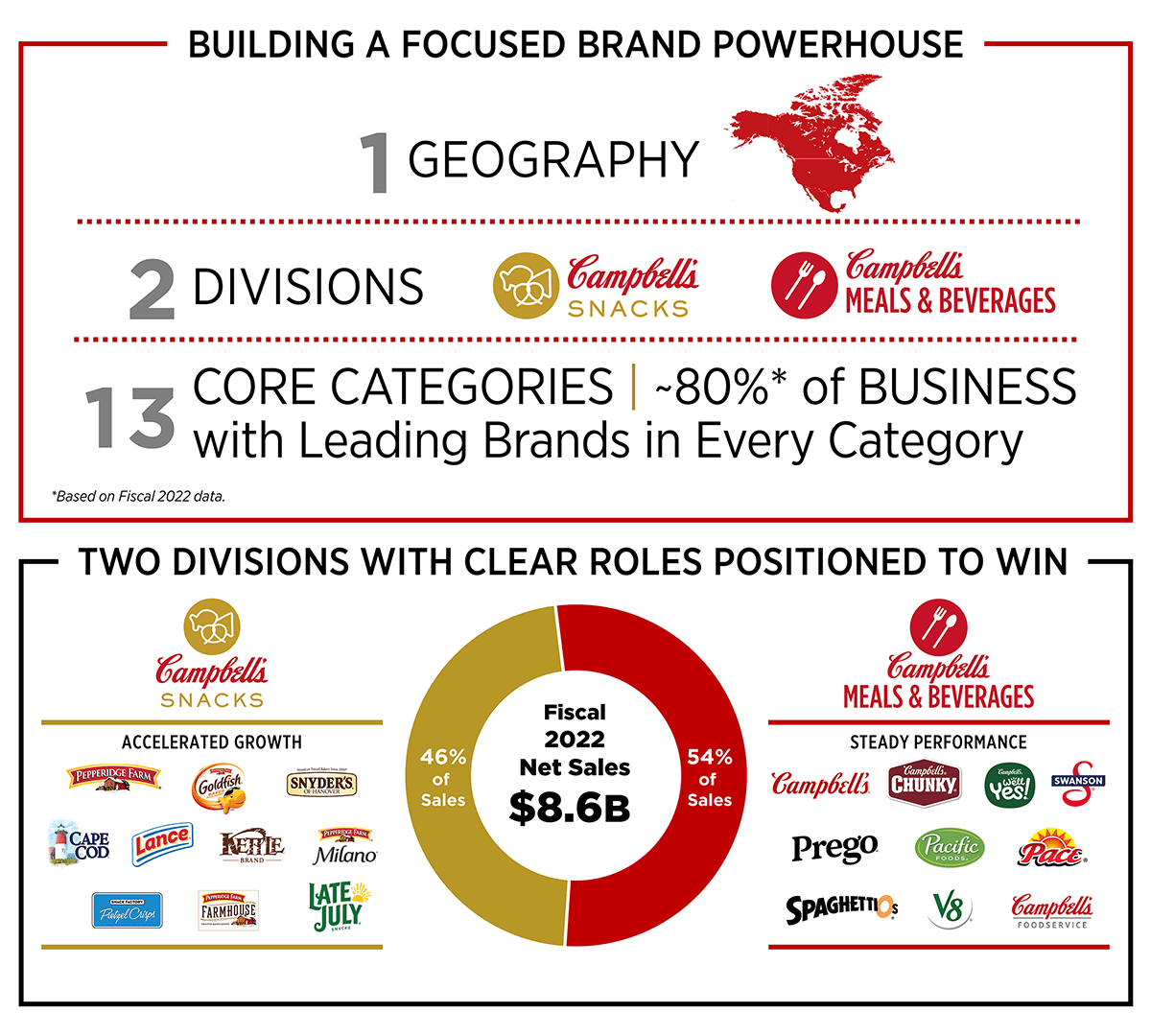

The company operates two divisions, which include snacks with brands like Cape Cod and Kettle Chips, which I quite like. The meals and beverages segment includes the iconic Campbell’s soup brand and various other brands like Swanson and Prego.

Campbell’s Soup Company

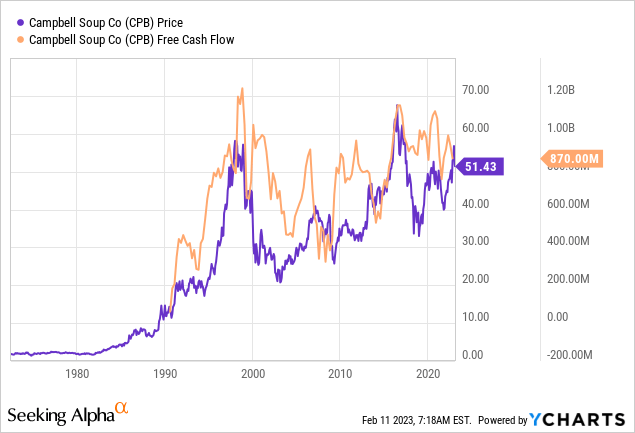

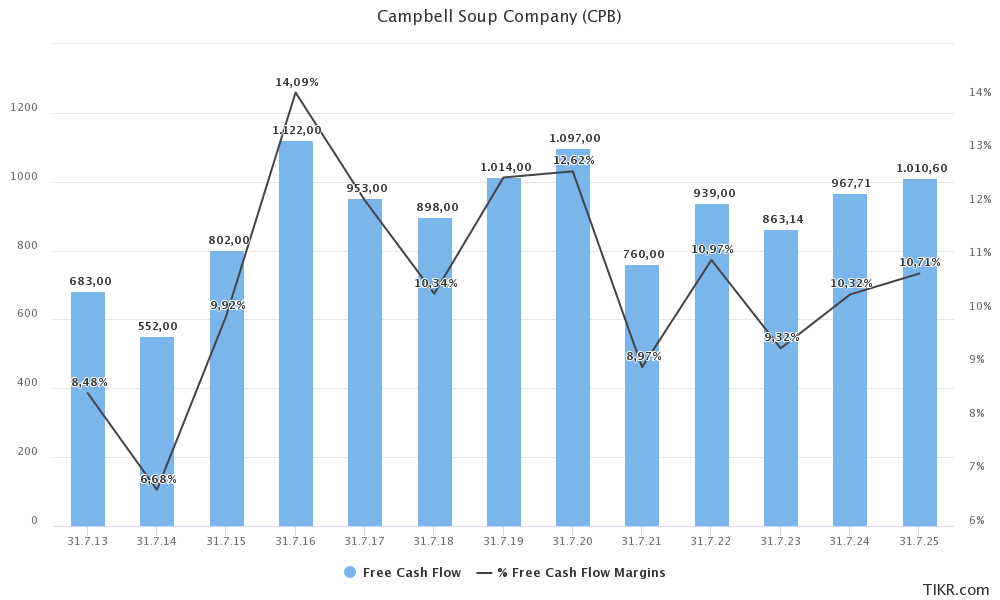

One of the biggest problems in the consumer staples industry is that a lot of companies are very mature. Campbell’s fast growth ended in the early 2000s when free cash flow growth peaked. Since then, free cash flow has hovered in a volatile sideways range between $400 and $1.2 billion.

Since the early 2000s, CPB has increasingly been pressured by what I believe are the key risks to mature food companies.

-

Slowing revenue growth: Mature companies in the consumer staples industry are often facing slowing revenue growth, which can make it challenging for them to maintain or grow their dividend payouts.

-

Increased competition: As the consumer staples industry is highly competitive, companies in this space may face increased competition, which can negatively impact their market share and financial performance.

-

Commoditized products: Consumer staple products, such as food and beverages, are often commoditized, which can result in lower profit margins and make it challenging for companies to differentiate themselves from their competitors.

-

Price sensitivity: Consumer staples products are often seen as necessities, but price-sensitive consumers may switch to cheaper alternatives if prices increase. This can result in declining sales and profitability for the company.

These are the company’s annual average compounding growth rates between FY2013 and FY2025E:

- Revenue: 1.3%

- EBITDA: 0.8% (slowing pricing advantages)

- Free cash flow: 3.3% (more cash efficient)

That said, since 2016, the company hasn’t grown its free cash flow either.

TIKR.com

If we assume that CPB has a clear path to $1.0 billion in free cash flow, we’re dealing with a free cash flow yield of almost 7%. The current dividend yield is 2.9%. The net debt ratio is less than 3.0x. The credit rating is BBB. In 2017, the company agreed to buy Snyder’s-Lance for $4.9 billion in cash. Since then, the company has focused on repaying that debt.

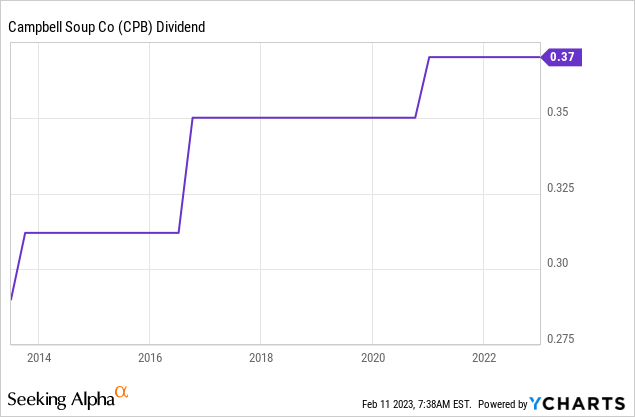

Based on this context, the company has the following dividend growth rates:

- 10Y CAGR: 0.2%

- 5Y CAGR: 1.1%

- 3Y CAGR: 1.9%

The most recent hike was announced on December 9, 2020, when management hiked by 5.7%. Over the past ten years, investors have seen three dividend hikes.

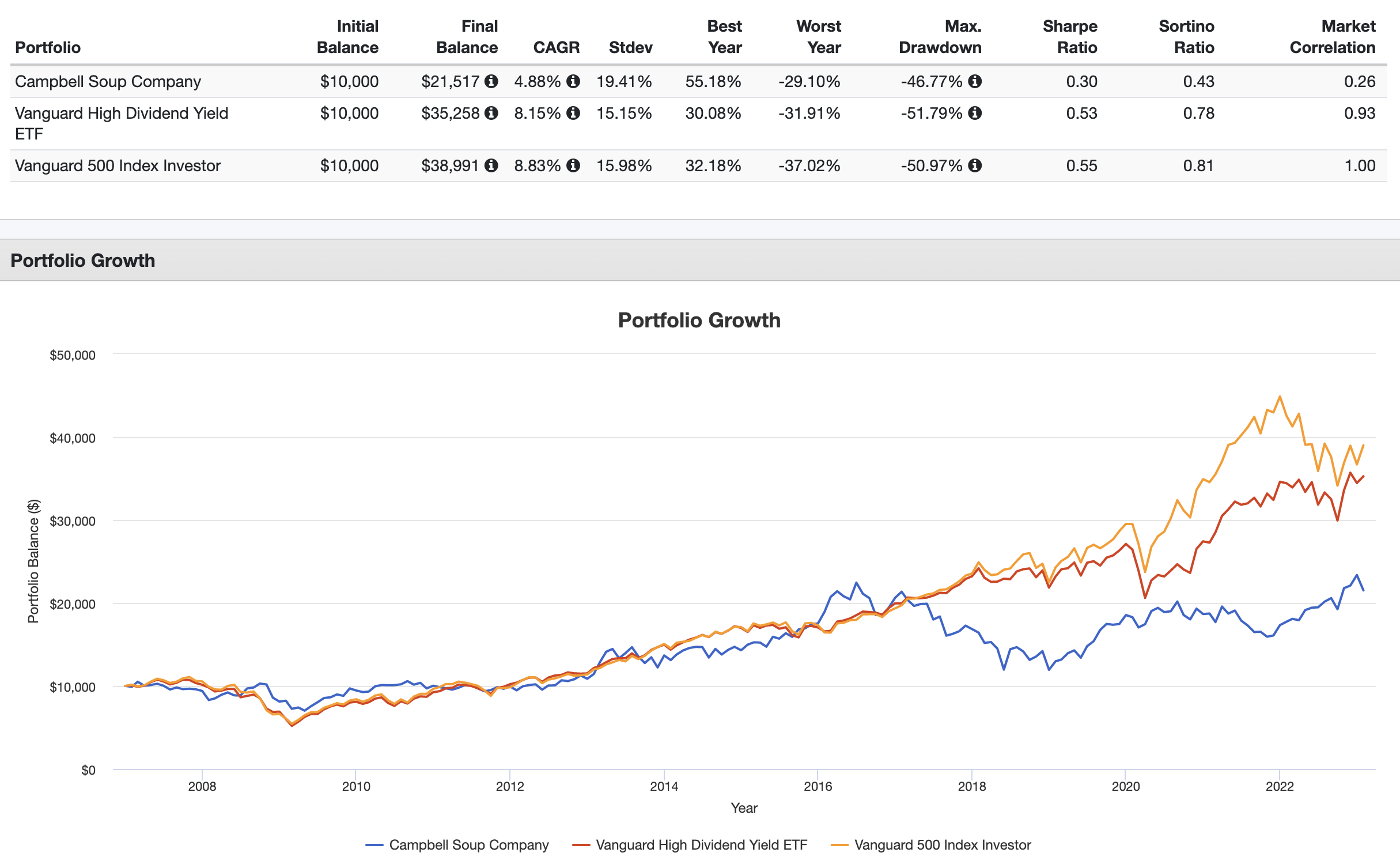

When it comes to long-term performance, we see the opposite of Best Buy. While Best Buy’s performance wasn’t that bad, it was way too volatile. Campbell’s volatility is a big benefit. Its performance is not.

Since 2007, CPB shares have returned 4.9% per year, including dividends. This underperforms the Vanguard High-Yield ETF by 330 basis points per year. The standard deviation is very subdued, but that doesn’t add value if the dividend yield is equal to the Vanguard High-Yield ETF – it’s lower than the Schwab Dividend ETF I mentioned earlier in this article.

Portfolio Visualizer

If I were an investor looking for conservative exposure and a decent yield, I would go for PepsiCo (PEP). The company just confirmed again that it can withstand pressure like inflation, as it enjoys high pricing power, a similar dividend yield to CPB, and a profile that allows for much higher growth.

When looking for a higher yield, I would suggest again going with the SCHD ETF.

Takeaway

In this article, I analyzed the risk/reward of two dividend stocks and concluded that they are not suitable investment options due to their unfavorable risk/reward ratio and limited potential for significant growth in the future. Instead, I provided alternative investment opportunities that align with the expectations of various investors.

It is important to note that the purpose of this article was not to encourage existing investors to sell their holdings. Making a switch may not be feasible for some due to potential capital gains taxes. However, for new investors, it is recommended to avoid these two stocks.

In the next few weeks, we will delve deeper into high-yield investment options and present articles for investors seeking both growth and income. So, stay tuned for that!

Thank you for reading, and feel free to share your thoughts and opinions in the comments section.

Be the first to comment